After a three-year run when annual U.S. per-capita dairy product consumption rose from the year before, 2017 yielded a small decline in overall consumption. The decrease was mostly attributed to a continuing drop in fluid milk consumption.

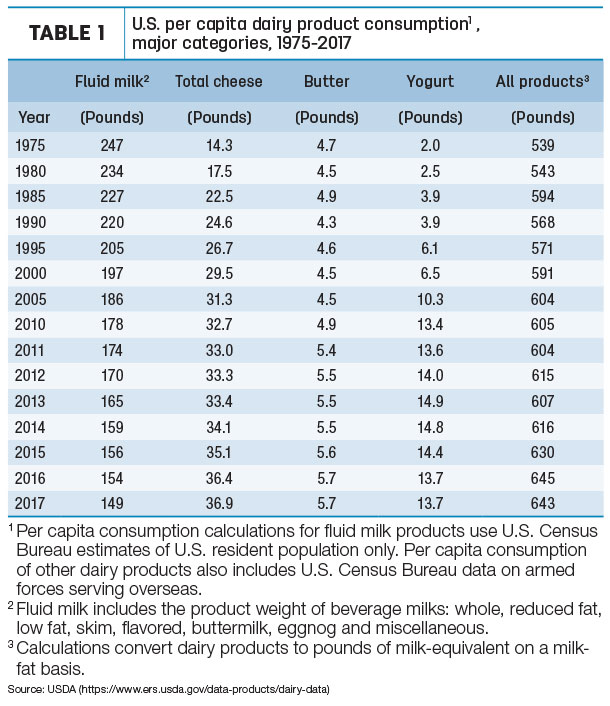

Annual USDA data shows 2017 U.S. per-capita consumption of dairy products (on a milk-equivalent, milkfat basis) slipped 2 pounds to 643 pounds (Table 1).

The disappointing 2017 numbers followed three years in which per-capita consumption had jumped 38 pounds, from 607 pounds in 2013 to 645 pounds in 2016. This was the first year-over-year decrease in total consumption since 2013.

Fluid milk continues slide

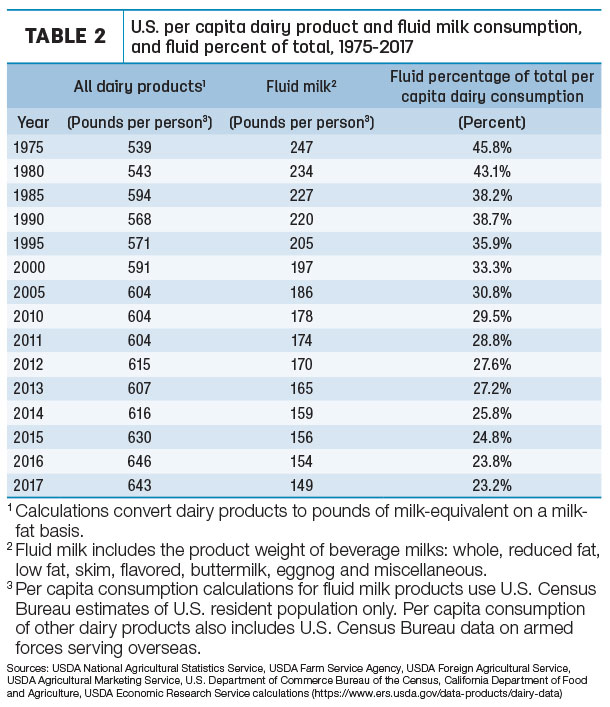

While overall per-capita dairy product consumption has generally trended upward, consumption of fluid products has declined both in terms of volume and as a percentage of total dairy product consumption.

U.S. per-capita consumption of fluid milk was estimated at 149 pounds in 2017, down 5 pounds from 2016 and down about 50 pounds in the past two decades. U.S. per-capita fluid milk consumption is now down nearly 100 pounds since 1975. Year-to-year per-capita sales have increased only three times over the 43-year period, with the last increase occurring in 1989.

As a percentage of total dairy product consumption, fluid products have slipped from nearly 46 percent in 1975 to just over 23 percent in 2017 (Table 2).

Unlike recent years, the 2017 decline in fluid milk consumption was not offset by robust gains in a combination of other dairy products (Table 1).

Unlike recent years, the 2017 decline in fluid milk consumption was not offset by robust gains in a combination of other dairy products (Table 1).

The milk equivalent of cheese consumption has been greater than fluid milk since the mid-1980s, and indications are 2017 U.S. cheese consumption (excluding cottage cheese) did rise slightly from last year’s record to almost 37 pounds.

American cheese consumption rose to about 15.1 pounds per person, up 0.8 pound. However, consumption of other cheeses slipped about 0.1 pound to 21.9 pounds per person. Per-capita consumption increased in 28 of the last 29 years and has declined only twice since 1975.

Per-capita consumption of yogurt (13.7 pounds) and butter (5.7 pounds) were unchanged from the year before, but consumption of regular ice cream, milk powders and dry whey declined.

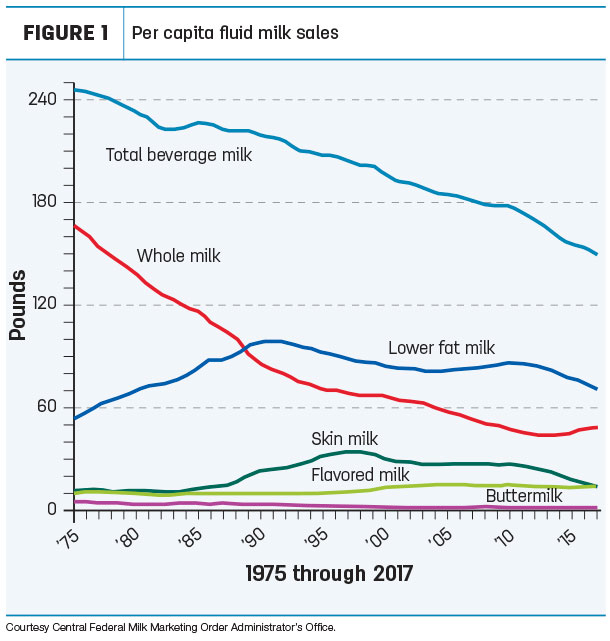

If there is a bright spot in the fluid milk data, it regards per-capita consumption of whole milk (Figure 1), which has reversed course and has now increased three consecutive years.

Sales of flavored milk increased fractionally in 2017, but that was offset by a combined 1.5-billion-pound decline in sales of reduced-fat (2 percent), low-fat (1 percent) and skim milk. Total fluid milk sales in 2017, at 48.63 billion pounds, were down 1.07 billion pounds from 2016.

Sales of flavored milk increased fractionally in 2017, but that was offset by a combined 1.5-billion-pound decline in sales of reduced-fat (2 percent), low-fat (1 percent) and skim milk. Total fluid milk sales in 2017, at 48.63 billion pounds, were down 1.07 billion pounds from 2016.

The number of plants processing fluid milk in 2017 increased by two to 448, but the average milk volume per plant declined about 3 million pounds to 108.5 million pounds per year. ![]()

AFBF analyzes plant-based beverages

Using Information Resources Incorporated (IRI) scanner data from 2015 to July 2018, American Farm Bureau

Federation economist Michael Nepveux has created an interactive dashboard to estimate market shares of dairy and plant- and nut-based beverages.

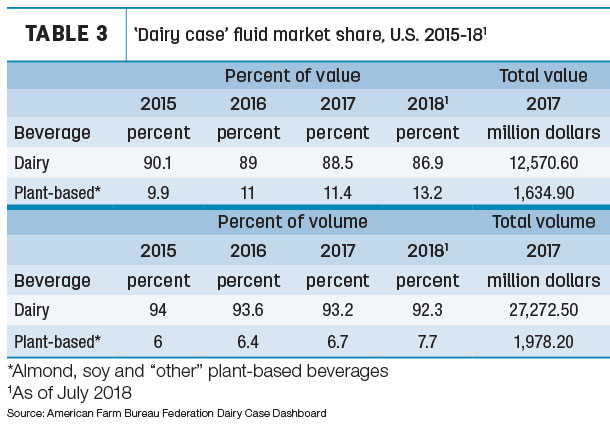

Although still dwarfed by fluid dairy consumption, plant-based product volume, value and share of the “dairy case” are on the rise (Table 3).

According to the analysis, more than $1.6 billion was spent on plant- and nut-based beverages sold in the dairy case in 2017. These sales were up $141 million, or 9 percent, from 2015 levels.

According to the analysis, more than $1.6 billion was spent on plant- and nut-based beverages sold in the dairy case in 2017. These sales were up $141 million, or 9 percent, from 2015 levels.

On a value basis, the market share of nut- and plant-based beverages has increased from under 10 percent in 2015 to over 13 percent through July 2018. During this same time, the market share of traditional milk beverages has dropped from over 90 percent in 2015 to under 87 percent in 2018.

These market shares include only nut- and plant-based beverages that are sold in the dairy case alongside, and directly competing with, refrigerated milk. There are also nut- and plant-based beverages that are shelf-stable and labeled “ready to drink.” When including those additional beverages, the market share grew from 13 percent in 2015 to 16 percent through July 2018, with over $2.1 billion in annual sales in 2017.

Within the category of plant- and nut-based beverages, almond beverages represented 67 percent of the market through July of 2018, up from a 61 percent market share in 2015. The growth in almond beverages has likely come at the expense of soy-based beverages and traditional milk.

The market share for soy-based beverages has declined from 19 percent in 2015 to approximately 11 percent through July of 2018.