When it comes to risk management strategies, there are four basic actions a manager can take: (1) avoid the risk, (2) transfer the risk, (3) control the risk or (4) accept the risk.

Avoiding risk is simply choosing to not do something that exposes you to the risk. For example, if you are not comfortable with the risk of growing a particular crop, you can avoid it by simply not growing the crop. If you don’t grow it, you don’t have the expenses associated with growing it nor do you have resources tied up in growing it.

To evaluate this strategy, the manager would compare the benefits of not growing the crop to the lost potential income and the uncertainty around it.

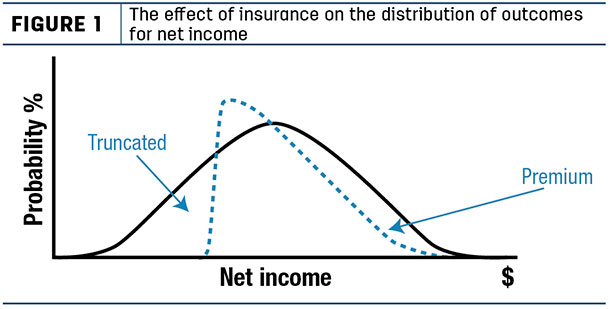

Transferring risk outside the farm or ranch is usually accomplished through insurance or marketing contracts. Insurance contracts provide protection from downside risk in exchange for a premium expense. By paying the premium, you essentially transfer some of the potentially bad outcomes to a large insurance company that can better withstand the negative consequences.

This has the effect of truncating your distribution of possible outcomes on the downside, in exchange for subtracting the insurance premium from every outcome (Figure 1). Marketing tools such as put options work in this same way.

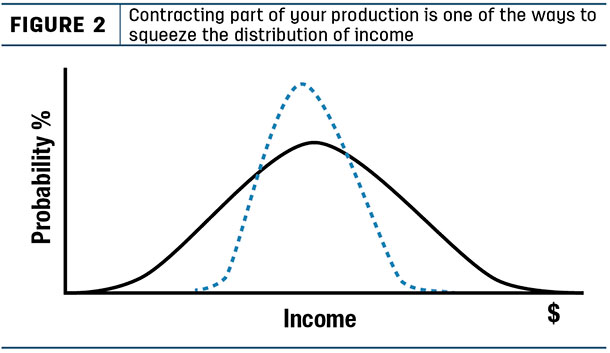

A marketing contract that locks in a price on some or all of your production would have the effect of squeezing your distribution of outcomes into a tighter range of possibilities (Figure 2).

In this case, the risk associated with the full range of outcomes is transferred to the person you are contracting with. In exchange, you pay a risk premium collected up front in the contract price that is slightly in the other parties’ favor, when compared to the price expected at the end of the contract period.

The more production you lock in, the tighter the price range. This makes sense when you consider that as you contract more and more production, you transfer more of the potential upside and more of the risk premium to the other party, in exchange for transferring more of the downside risk.

Evaluating insurance and marketing contracts can be frustrating, especially when considered looking back in time. Once the outcome has been determined, it is tempting to declare the decision good or bad based on whether the contract worked in your favor. That is a bad habit to get into.

Managers should always make a sincere effort to evaluate any decision at the time it is taken, in terms of what it will cost in premium and, in the case of marketing contracts, the benefit of the upside potential associated with transferring the risk to a third party.

Controlling risk is by far the most active form of risk management. There are two primary means for controlling risk: either by controlling the probability of various outcomes occurring or by controlling the impact of those outcomes if they do occur. Very seldom can a manager do both at the same time.

For example, a piece of machinery may break down at any moment. You can control the risk of a machinery breakdown by properly maintaining the machine and reducing the chance of failure, thus extending its useful life or saving money on a costly repair. To evaluate if this is a good strategy, you need to compare the extra expense of maintaining the machine versus the effect it has on reducing the probability of a breakdown.

Controlling the impact of a bad outcome (consequence) involves using strategic risk management tools like diversification, keeping extra resource reserves on hand or maintaining flexibility. The goal here is to reduce the impact of a bad outcome or increase the impact of a good outcome.

For example, having extra cash reserves could reduce the impact of poor revenue in a given year. To evaluate such a strategy, the manager would evaluate the cost in potential lost income from keeping the cash reserves on hand, versus the benefit the reserves offer for weathering the storm of a bad year and the associated peace of mind it brings.

Finally, accepting risk is also a risk management strategy. Risk or uncertainty about the future may include both positive and negative changes (benefits or costs). In some cases, there are simply no tools available to either control or transfer a particular risk. In other cases, the tools available are just too expensive to justify their use.

One of the bigger questions many managers do not stop to consider for long is, “How much risk is right for you?” If you had a choice, would you take on more risk if it meant more profit? Would you accept a lower profit for less risk? How much profit does it take to make it worth taking on extra risks?

These are the questions that can only be answered by the individual taking on the risks. Some individuals avoid risk, while others confront it head-on.

The challenge here is to figure out which kind of person you are. Since every investment involves risk, it is important to know how risk-tolerant we are. “Risk tolerance” is the amount of risk you are willing to take on for the possibility of earning a particular level of return.

RightRisk has developed several approaches over the past 15 years to help individuals sort this out for themselves. In addition, the team has developed over 30 individual tools to help managers evaluate the trade-offs between the potential returns and risks involved across many different types of management decisions.

These tools are freely available at the website Right Risk, many with accompanying guides and examples.

Agricultural managers routinely speculate on risk. That’s where a lot of the profit in farming and ranching resides. However, such decisions should be made only after careful evaluation of the potential impact and your willingness to accept the probability of their occurrence.

Risk management is an activity that can return big dividends. Thoughtfully evaluating available risk management strategies as a habit for conducting your business can lead to a more stable and prosperous business future. ![]()

Jay Parsons is an associate professor with the University of Nebraska – Lincoln. Email Jay Parsons. Jeff Tranel is a business management economist with Colorado State University Extension. Email Jeff Tranel.

-

John Hewlett

- Ranch/Farm Management Specialist

- University of Wyoming

- Email John Hewlett