Let me begin by reviewing the definition of the mailbox milk price announced by the Agricultural Marketing Service (AMS). It is the net price between what a dairy farmer is paid for the milk they market, less the deductions to market that milk. In other words, the mailbox price is the money dairy farmers receive for the milk they market after all marketing deductions such as hauling, cooperative dues, promotion assessments, etc.

Monthly, AMS publishes average mailbox prices for 19 states and regions of the country which are part of the federal order system. Mailbox prices are announced on a per-hundredweight (cwt) basis at average milk component tests for each reporting area. Generally, AMS releases mailbox prices about three months after the month being reported. (Due to California joining the federal order system in 2018, California’s mailbox price information is incomplete at this time and is not included in this article.)

Two tables are presented to help see what mailbox milk prices are telling us. Table 1 shows 2017 and 2018 mailbox milk prices.

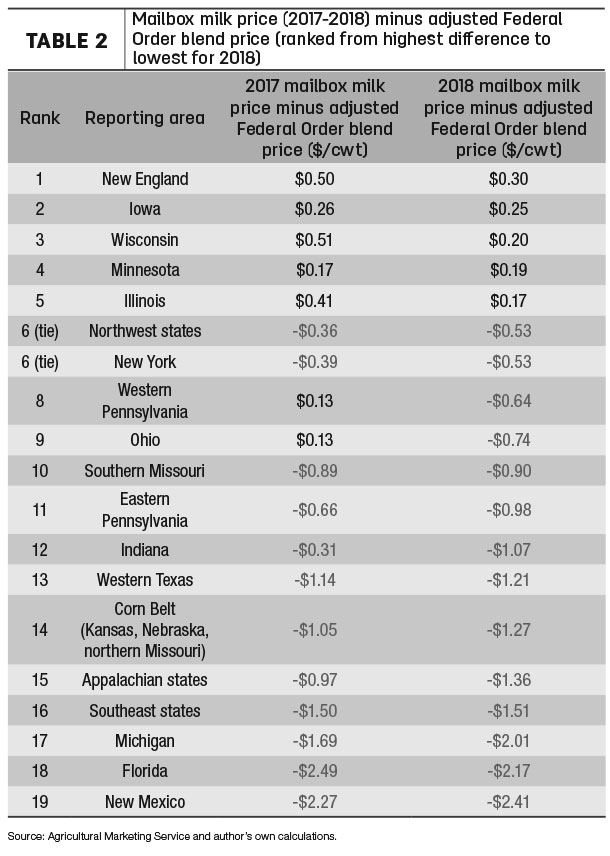

Table 2, also for 2017 and 2018, shows the difference between the mailbox price and an “adjusted federal order blend price” for each reporting area.

Let me explain the second table further. As stated above, mailbox prices are announced at average component tests for the reporting area. Federal order blend prices per cwt are announced at a standardized test. Within federal orders, there are price adjustments for different locations. Order blend prices are announced at one specific or base location. Mailbox prices are an average of all payment locations.

To make an “apples to apples” comparison between mailbox prices and order blend prices, I calculate an adjusted federal order blend price for each mailbox reporting area. My adjustment calculates the order blend prices at the order’s average components and at an estimated average location.

The weighted average of all mailbox prices in 2018 was $15.72 per cwt. This was $1.59 per cwt lower than 2017 and the lowest since 2009’s average of $12.82 per cwt. The states or areas at the top and bottom of the mailbox rankings have changed little over time. For nine of the past 10 years, Florida reported the highest mailbox price. The one exception was in 2015 when New England gained the number one spot. On the other end, New Mexico has had the lowest mailbox price for 10 consecutive years.

A closer look at Table 1 shows some areas declined more in price than others in 2018. For example, Ohio’s mailbox price dropped $1.97 per cwt while it only went down $1.22 per cwt in Florida. Changes in over-order premiums, balancing costs, milk utilization and cooperative operations can account for the differences.

As a watcher of mailbox prices for many years, I see a trend occurring. Average mailbox prices are converging. A few years back, the difference between the highest and lowest annual mailbox price ranged from $4.75 to $5 per cwt. For the past three years, the range was below $4 per cwt. If we drop the highest and lowest mailbox prices, the range was only $2.80 per cwt in 2018. Dairy industry consolidation and increased movement of both bulk milk and finished dairy products, along with declining fluid milk sales, are reasons for this trend. In my lifetime, dairy has moved from a local to a regional to a national and international industry, all of which bring mailbox prices closer together.

Now let’s move to Table 2 and look at the relationship between mailbox prices and the adjusted order blend price. I see another trend here as well. Mailbox prices are continuing to fall further below order-adjusted prices. Only five of the 19 areas had a mailbox price higher than the adjusted federal order blend price in 2018. Eight of the reporting areas’ mailbox prices were over $1 per cwt lower than the order blend. Going back to my 2013 article, nine areas had higher mail prices than the order blend. And only three had mailbox prices at $1 per cwt below order prices. Unfortunately, in recent years, mailbox prices are declining more than federal order blend prices.

The best explanation for this trend is milk supply exceeding demand. More milk has led to lower over-order premiums. Milk has been sold at steep discounts below federal order class prices in order to find a market. And too often, milk was dumped due to no viable market. In addition, the expense to transport milk has increased. All of these factors have lowered mailbox milk prices relative to the federal order blend price.

I am optimistic dairy farmers and their cooperatives will see the growing negative difference between mailbox prices and order blend prices as a call for action. For areas with mailbox prices below order prices, the money between the mailbox and order price is potential revenue for dairy farmers. As a former dairy cooperative CEO, I know the challenges in recouping this money.

It requires cooperatives finding ways to increase efficiencies in their milk marketing, and better balance between milk supply and demand. It requires cooperatives working more closely together to lower and be equitably compensated by milk buyers for balancing costs, and to not underprice another cooperative just to gain a milk market.

Finally, I encourage all dairy farmers, when they receive their milk check, to benchmark their mailbox price to their respective order blend price, adjusted for location and components. Such benchmarking helps you measure how well your milk is being marketed. If your mailbox price is declining relative to your order blend price, find out why. Ask questions, and seek solutions. The more knowledge you have about your milk price, the better opportunity you have to improve it. ![]()

Calvin Covington is a retired dairy cooperative CEO and now does some farming, consulting, writing, and public speaking.

-

Calvin Covington

- Retired Dairy Co-op Executive

- Email Calvin Covington