Many business owners and farmers often do not prepare their own federal tax forms due to the complexity of the tax laws. At the beginning of each year, farmers must review their recordkeeping, generate income and expense reports, capital asset purchases and sales lists, and meet with their tax professionals.

Farmers should have a basic understanding of the concepts and applications of federal income tax law that may impact their business and future decision-making. Consulting with an accountant, bookkeeper or other tax return preparer will help farmers understand and appropriately assess the impacts of a decision on their income tax liability.

Farm recordkeeping

Recordkeeping begins with collecting and organizing the farm business' production (physical) and financial (income/expense) information. Financial recordkeeping is often cited to fulfill income tax reporting requirements. Thorough records may need to be provided to government agencies, lenders, insurance companies, safe handling practices, organic production, etc.

The Internal Revenue Service (IRS) allows a farm business to use either cash or accrual accounting methods while imposing special treatment to certain income and expense items. Under the cash method of accounting, income is reported in the tax year it is received. Expenses under the cash method are deducted in the tax year the expense is paid. Many farmers use the cash method because they find it easier, and they are able to better match farm cash flows with the taxes that are due. However, the accrual method more accurately measures the true performance of the farm business.

Farm tax management strategies

Key goals that farmers might have for tax management include:

- Preserve the benefits associated with deductions and exemptions

- Minimize income tax paid over time, not just in the current year

For example, a farmer might encourage his or her tax preparer to reduce net farm profit on Schedule F (Form 1040) to zero or near zero. This may result in "losing" the benefit of offsetting taxable income with deductions and exemptions, especially if little non-farm or interest income is reported on Form 1040.

A more appropriate approach should be to minimize tax liability over several years to manage tax liabilities, as compared to only focusing on the current year's obligation. Various techniques may be utilized to either reduce or increase net farm profit reported to the IRS each year. However, some choices must be made before the end of the tax year.

An initial step in managing income tax liability should be to estimate farm income, expenses and net profit in November before the farm’s year-end is finalized. For example, during an anticipated high-net-farm-profit year, income may be reduced before year-end by either postponing sales or prepaying expenses. Delaying delivery of farm products until January or later would shift income to the following year. One important note: A check received from a customer, vendor or cooperative must be reported in the year it was received. The check was available to the farm business on receipt, so recognition of this income can't be postponed.

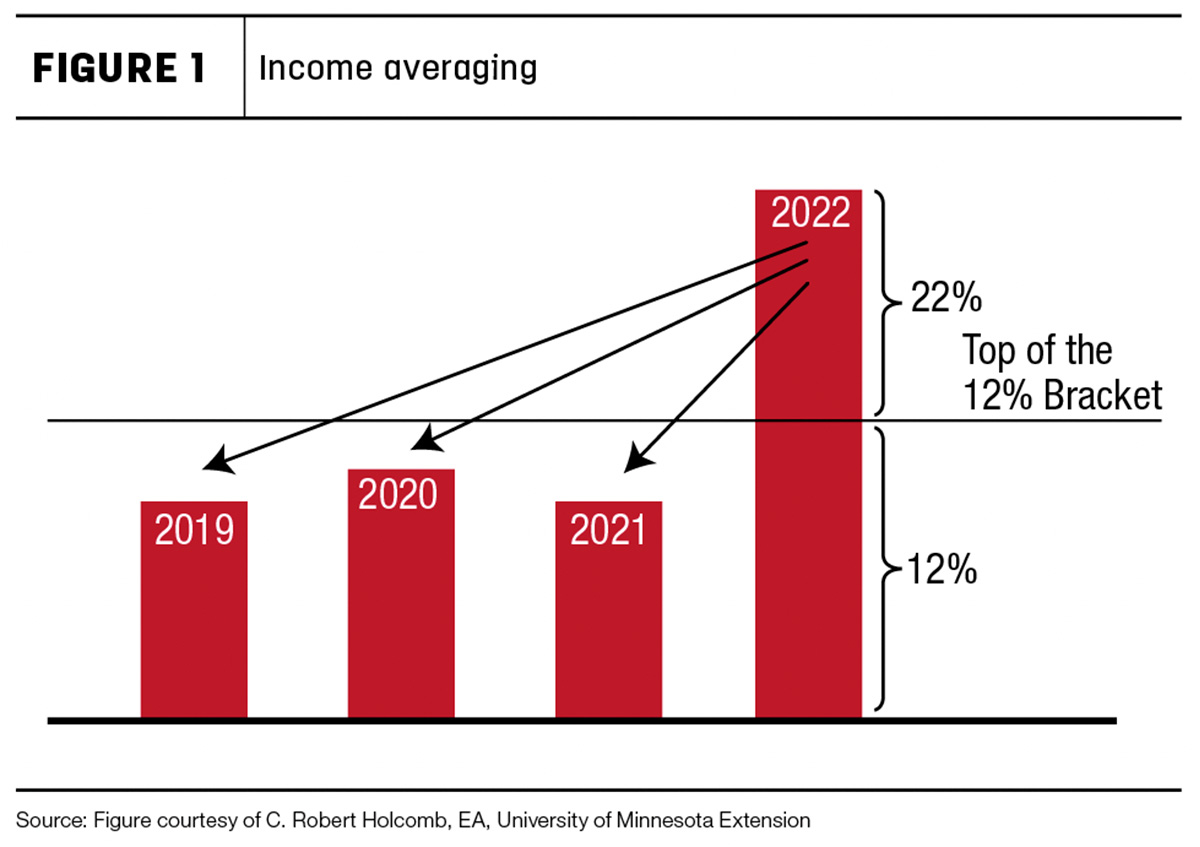

Farm income averaging

A tax planning strategy that may help farmers mitigate tax liability includes farm income averaging. This strategy is only applicable for farm income and is filed on Form 1040 Schedule J. Farm income averaging does not average farm income but allows the farmer to utilize unused tax brackets from the previous three years. Farm income averaging doesn’t affect self-employment tax or taxable income, as only the tax rates are affected.

Income averaging is performed when the tax return is filed. The farmer does not need to do anything prior to the end of the year for income averaging. Figure 1 illustrates how income averaging can be applied. In this example, the farmer has unused 12% brackets in the prior three years and high income in 2022. Income averaging allows the farmer to elect to put back an equal amount of money into each of the previous three years and use up the unused 12% tax brackets. If the farmer wanted to put back $30,000 from 2022, he or she would have to put $10,000 back into tax years 2021, 2020 and 2019.

Depreciation options

Section 179 depreciation is a method that may be utilized to accelerate depreciation on qualifying assets. Assets with a depreciable class life of three to 15 years qualify if they were acquired and put into service during the prior year. The most common use of Section 179 may be used with beef and dairy breeding stock (five-year property), new machinery (five-year property), used machinery (seven-year property), single-purpose agricultural structures (10-year property) and drainage tile (15-year property). There is a maximum Section 179 deduction for 2022 ($1.08 million) and qualifying purchase limit ($2.7 million). Once qualifying purchases exceed this maximum, there is a dollar-for-dollar reduction in the deduction.

Bonus depreciation is a second option to depreciate capital assets. In addition to assets that qualify for Section 179, bonus depreciation includes purchased 20-year property, such as new or used farm buildings, machine sheds and barns. For 2022, bonus depreciation is 100%, meaning that if a farmer elects bonus depreciation on a group of assets, those assets will be 100% expensed. By default, bonus depreciation is taken on all qualifying assets. If unwanted, farmers must elect out (indicate what they don’t want to use bonus depreciation on).

Bonus depreciation is taken by class life. A farmer may elect to take the bonus on all the five- and seven-year assets purchased that year but exclude everything in all other class life categories. As a result, bonus depreciation will be taken on all assets in the five- and seven-year class life categories.

Choosing a tax professional

Choosing the right accountant or tax return preparer can be a crucial decision for farmers. Find a professional who has the experience and knowledge that best match the farm business and enterprises. It is important to remember that whoever is chosen may be hired by the farmer, but the professional must follow the law, the Internal Revenue Code and other regulations. Each tax professional must follow specific ethical standards and guidelines. These professionals should be a part of the management team of the farm business, and their advice should be sought when needed.

Disclaimer: This information changes often. This is educational information, not tax or legal advice. Information is based on material from the Land Grant University Tax Education Foundation (LGUTEF) and the IRS. For a list of universities involved, other fact sheets and additional information related to agricultural income tax, click here.