A rail strike was averted, fuel prices declined slightly and a couple of drought areas received moisture. Here’s a look at those and other hay market conditions in early December.

Drought conditions improve in spots

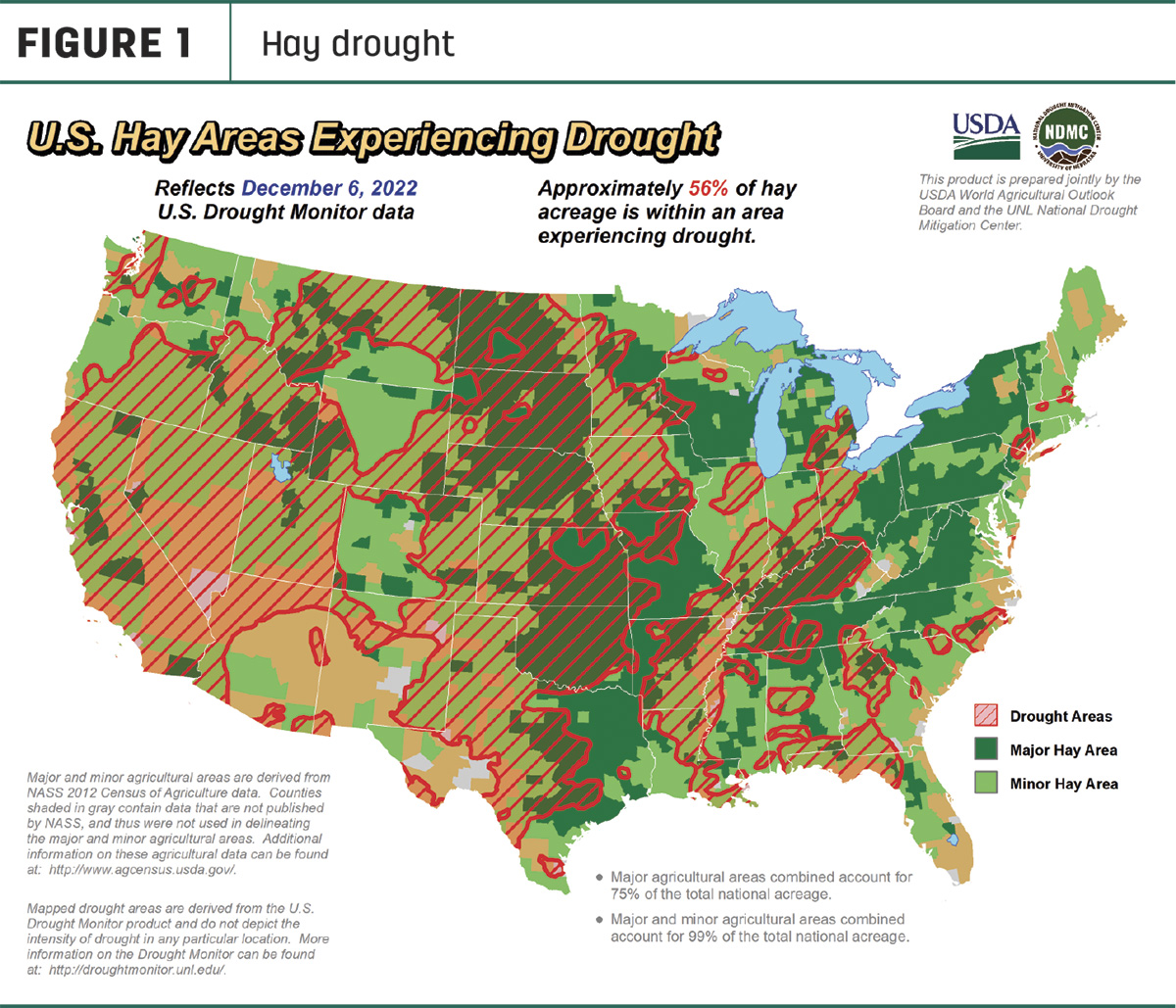

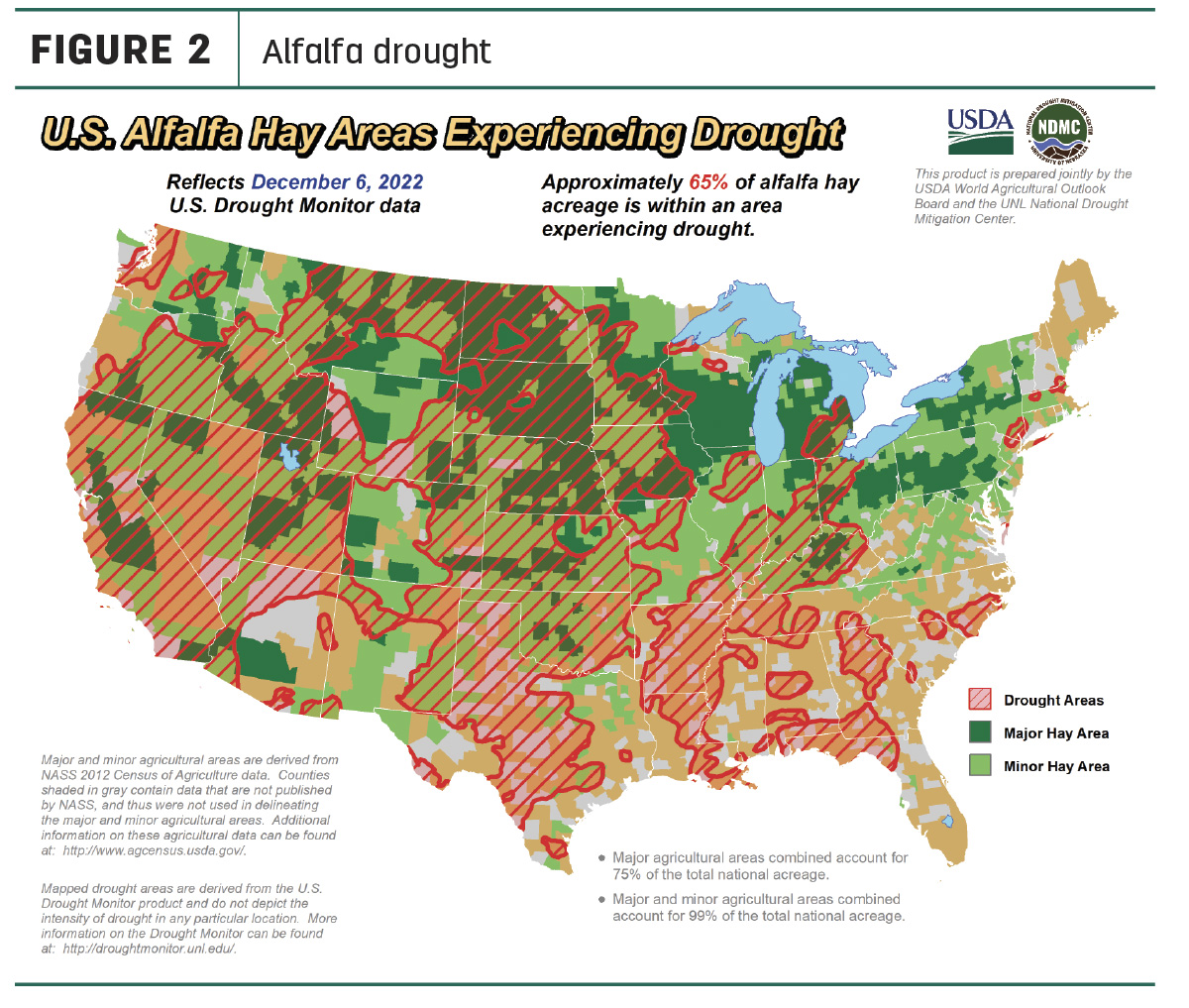

U.S. Drought Monitor maps indicate overall moisture conditions improved somewhat over the past month, primarily in parts of Texas and the Pacific Northwest. As of Dec. 6, about 56% of U.S. hay-producing acreage (Figure 1) was considered under drought conditions, 12% less than a month earlier. The area of drought-impacted alfalfa acreage (Figure 2) was down 4%, to 65%.

The early season snowpack in the West was normal to above normal for most of the region. The highest snowpacks of above 150% of median were in the Great Basin, Sierra Nevada and the southern Cascade Range, the Milk River of Montana, and the upper Yukon River in Alaska. The Southwest had below- to much-below-normal snowpack for early winter.

Hay prices tracked

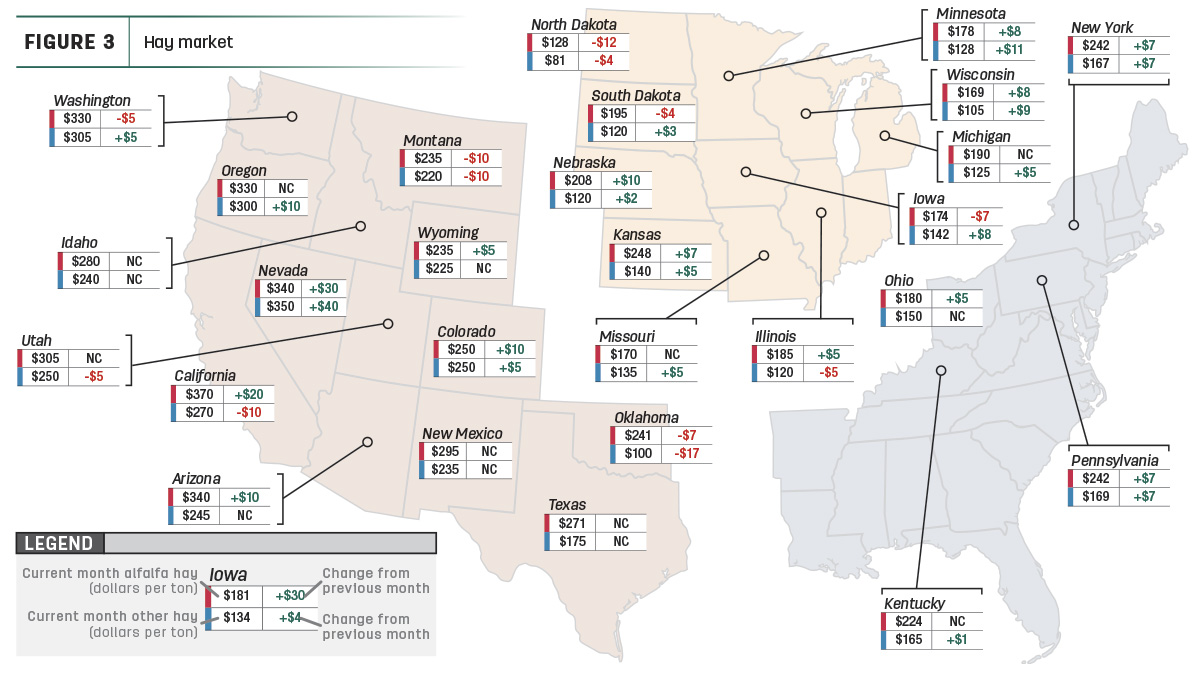

Price data for 27 major hay-producing states is mapped in Figure 3, illustrating the most recent monthly average price and one-month change. The lag in USDA price reports and price averaging across several quality grades of hay may not always capture current markets, so check individual market reports elsewhere in Progressive Forage.

Dairy hay

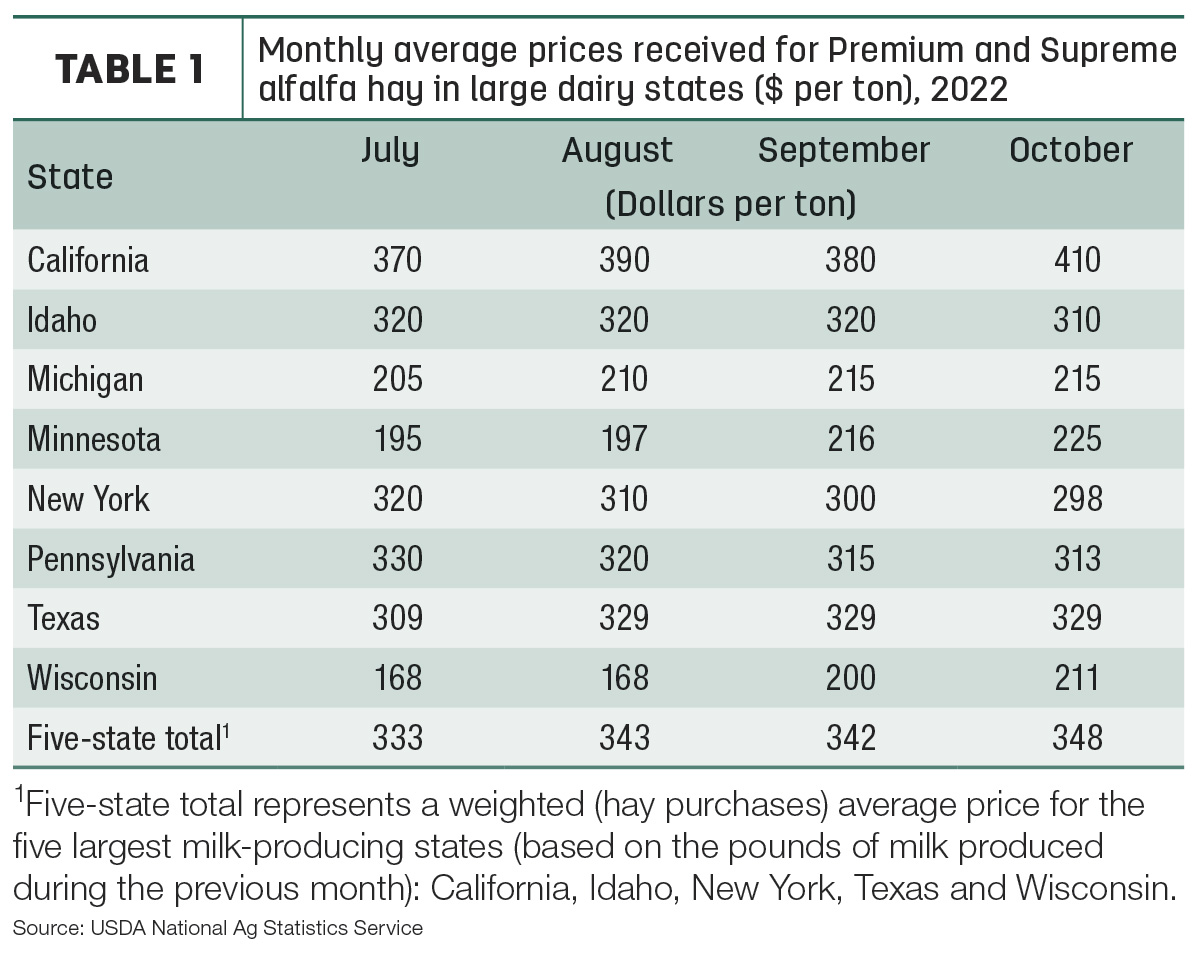

October’s average price for Premium and Supreme alfalfa hay in the top milk-producing states increased $6 from September, setting another record high at $348 per ton (Table 1). The average is $101 more than a year ago. Higher prices in California, Minnesota and Wisconsin offset small declines in Idaho, New York and Pennsylvania, with prices steady in Michigan and Texas.

Alfalfa

With higher prices for dairy-quality alfalfa hay, the U.S. average price for all alfalfa hay rose $4 in October to $281 per ton. Prices increased in 13 of 27 major forage states, led by a $30 increase in Nevada and $20 in California. Prices were lower in just six states, with Montana and North Dakota down $10 and $12, respectively. Year-over-year prices were up $100 or more in Arizona, California, Washington and Nevada.

The spread between U.S. average alfalfa and other hay prices was steady at about $101 per ton in October.

Other hay

At $180 per ton, the October 2022 U.S. average price for other hay was up $6 per ton from September. Prices increased in 15 of 27 major hay-producing states, with largest month-to-month increases in Nevada (+$40), Minnesota (+$11) and Oregon (+$10). Average prices for other hay were $135 more than a year ago in Nevada, and up $80 in California.

Hay exports slower

At 220,246 metric tons (MT), October alfalfa hay exports slipped to a four-month low. Monthly exports were down nearly 28,000 MT from the month before and down 117,000 MT from August.

Much of the decline can be attributed to lower sales to China, which also hit a four-month low at 147,978 MT. Despite the volume decline, sales to China represented 67% of all alfalfa hay exports in October.

At 24,764 MT, sales to Japan were up slightly from September but still near a seven-year low and represented 11% of the month’s total.

Demand for other U.S. alfalfa products also slowed. At 3,130 MT, October exports of dehydrated alfalfa cubes were the lowest since November 2008. Monthly shipments of sun-dried alfalfa meal dried up completely, with no export volumes reported. Exports of dehydrated alfalfa meal fell to a 37-month low.

Export volume for other hay hit a four-month high but remained weak in October. Foreign sales totaled 86,643 MT, up about 10,000 MT from the month before. At 51,692 MT, October sales to Japan were the highest since June and represented about 60% of the monthly total. October sales of other hay to South Korea were the fourth lowest of the year.

Regional markets

Here’s a snapshot of regional markets to start December:

- Southwest: In Texas, some areas received beneficial rains to end November but drought continued; however, hay demand was strong with prices firm in all regions. Hay was still moving into the state from bordering states, but trucking and freight rates continued to have a large impact on delivered prices. The productivity of winter wheat crop will be very important.

In California, trade activity and demand were slow to moderate. Retail hay demand was moderate with steady prices. Export and dairy hay demand were slow to moderate.

- Northwest: In Montana, hay sold unevenly steady on moderate demand and offerings. With the onset of winter, ranchers were out searching for hay, and supplies were starting to tighten. Several producers reported they are out of hay or they didn't want to sell any more until they ship the hay they already have sold. Hay prices remained the lowest in far-eastern Montana, where producers are competing with Dakota hay prices, and prices remained the highest along the Rocky Mountain Front and Central Hi-line, where the drought is the worst.

In Idaho, trade remained slow with good demand, especially for wheat straw. Alfalfa was steady in a light test. Supplies were light and in firm hands.

In Colorado, trade activity was moderate. Very good demand for horse hay held prices steady. Buyers for feedlot and dairy hay indicated they had enough hay purchased. With little supply available, those still seeking hay are finding a hefty price tag.

In the Columbia Basin, domestic and export alfalfa and forage mix hay trade remained steady, with inclement weather conditions limiting trading somewhat.

In Wyoming, all reported forages sold steadily. Demand was moderate. There was very light snow in the eastern areas of the state with dry conditions at lower elevations in the western areas. Most producers were done with hay production for the year. With the moisture in the east, cornstalk baling had come to a halt.

- Midwest: In Nebraska, all reported forages sold steadily. Demand for alfalfa backed off a tick. Cattle producers were blending cornstalk bales with distillers' byproducts; some were using the corn-steep liquid and cornstalks for winter feed.

In Kansas, demand remained strong and prices were mostly steady, with an undertone of strength. Lots of cornstalks were baled and were being ground with alfalfa to help offset higher costs and to extend alfalfa supplies.

In South Dakota, prices for all classes of hay remained steady to firm on good demand. The supply of hay is very tight. Calves were arriving in feedyards and needing high-quality grass hay to get them started, adding strength to the grass hay market. High-quality dairy hay remained tough to find. Demand for cornstalk bales is strong.

In Missouri, hay movement remained good, the supply of hay was light to moderate, demand was moderate and prices were mostly steady.

In Iowa, buyer demand and auction attendance was moderate, with prices higher for nearly all categories except wheat straw.

In Wisconsin, prices for dairy-quality hay were steady. Overall forage supplies were good, but lower-quality hay was discounted.

- East: In Pennsylvania, alfalfa sold strong, alfalfa-grass mixes sold steadily and prairie-meadow grass sold steadily with a weak undertone. Wheat straw sold steadily with a strong undertone. Corn fodder sold steadily, with buyer demand moderate on a moderate-to-heavy supply.

In Alabama, trade was moderate on moderate supply and good demand.

Other things we’re seeing

-

Dairy: October’s U.S. average milk price rose $1.50 while average feed costs fell slightly, supporting monthly dairy producer milk income margins. October 2022 U.S. milk production was up about 1.2% from a year ago, with continued slow growth in cow numbers and a small increase in milk output per cow contributing to higher overall production. The number of milk cows on U.S. farms in October 2022 was estimated at 9.42 million head, 31,000 head more than October 2021 and 1,000 head more than September 2022.

-

Cattle: The number of beef cows marketed for beef increased in October, up 39,400 head from September and 35,800 more than October 2021. Year-to-date beef cow slaughter is up more than 377,000 compared to the same period in 2021, topping 3.28 million head.

-

Wages: October 2022 U.S. gross farm wages were up 7% compared to a year earlier. Farm operators paid their hired workers an average of $17.72 per hour during the reference week (Oct. 9-15, 2022). Among individual worker categories:

- Field workers received an average of $17.04 per hour, an increase of 6%.

- Livestock workers earned $16.52 per hour, up 7%.

- The field and livestock worker combined wage rate, at $16.90 per hour, was up 6%.

- Fuel: The U.S. Energy Information Administration (EIA) forecasts global oil inventories to fall by 0.2 million barrels per day in the first half of 2023 before rising by almost 0.7 million barrels per day in the second half of the year. The inventory forecast would result in a Brent crude oil price forecast averaging $92 per barrel in 2023, $9 less than the average of $101.48 per barrel in 2022.

The U.S. average price for gasoline was $3.39 per gallon on Dec. 5, down 14 cents from the week before but a nickel higher than the corresponding date a year earlier, according to the EIA. U.S. average retail gasoline prices are forecast to average $3.51 per gallon in 2023, down from $3.99 per gallon in 2022.

The average U.S. on-highway price of diesel was $4.97 per gallon as of Dec. 5, 17-cents-per-gallon below the week before, but $1.29 more than early December 2021. The U.S. average on-highway prices of diesel are forecast to average $4.48 per gallon in 2023, down from $5.05 per gallon in 2022.