Given recent history, factors setting the stage for hay markets and forage production are in a bit of a role reversal. Moisture conditions are improving regionally, but hay exports are weakening. Milk prices are headed toward five-quarter lows. We’ll get some clarity in how major crops are competing for available acreage in 2023 when the USDA releases its Prospective Plantings report on March 31.

With spring on our mind, here’s Progressive Forage’s monthly look at hay markets and conditions approaching the middle of March.

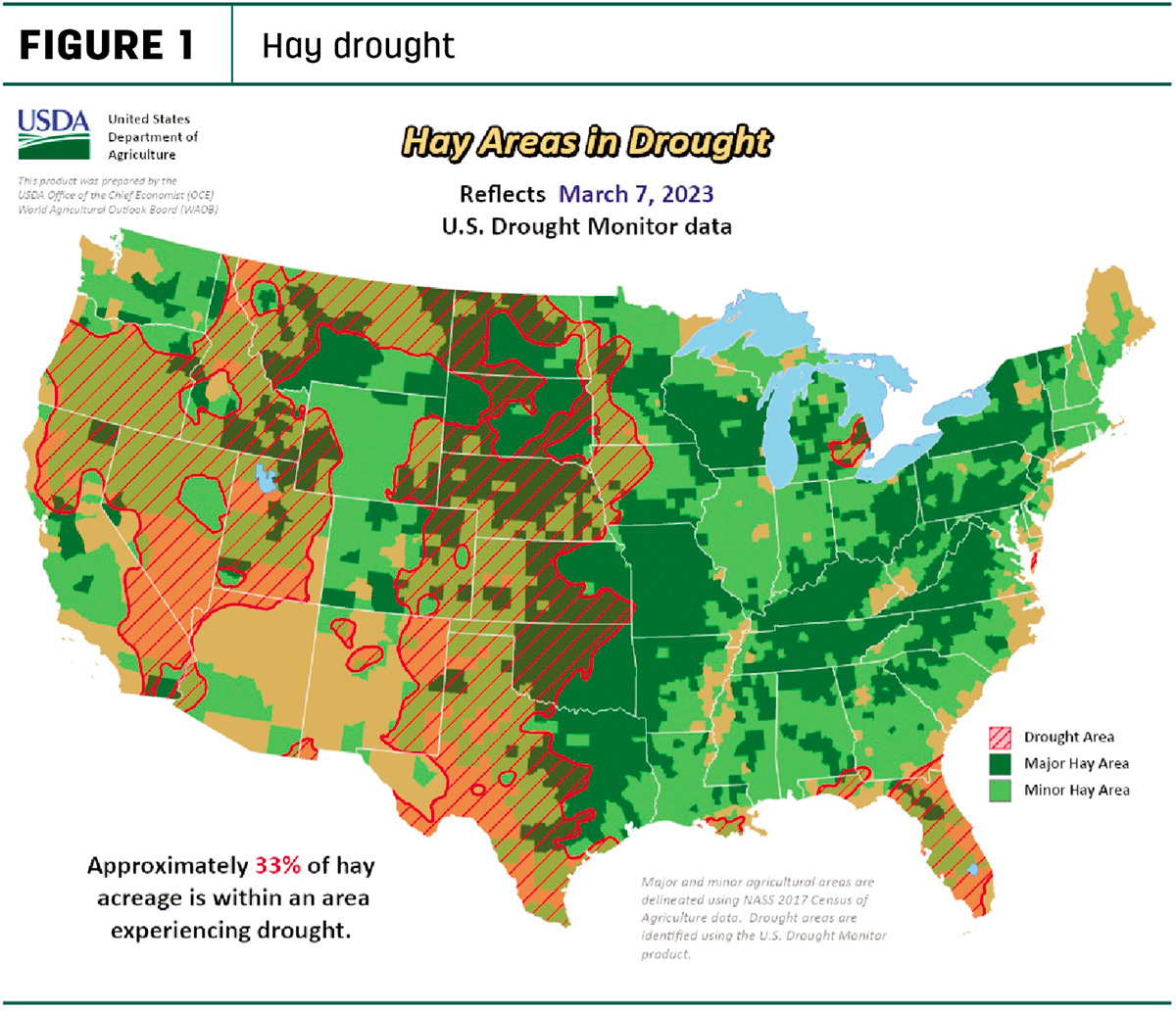

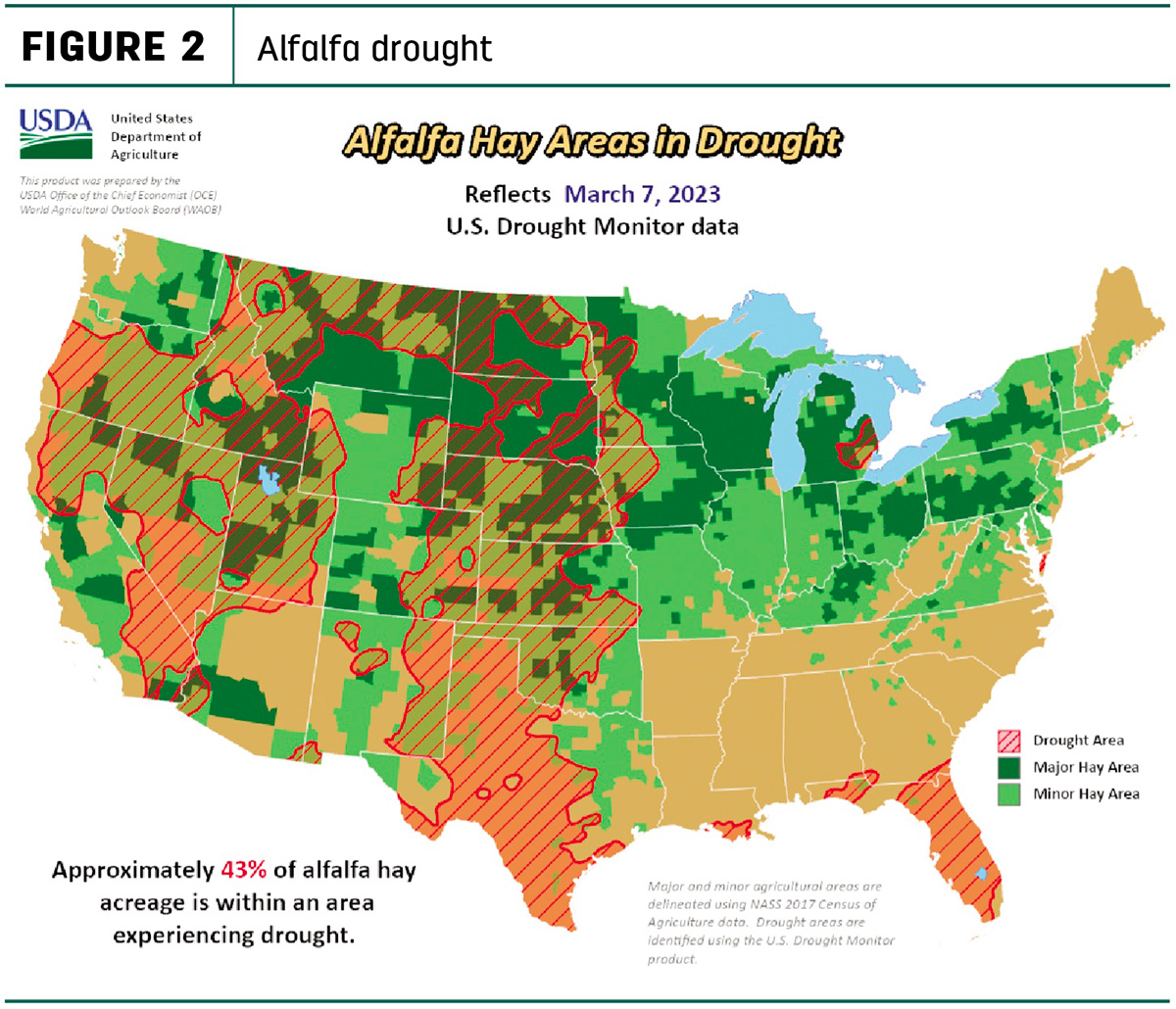

Moisture conditions improving

U.S. Drought Monitor maps are exhibiting better moisture conditions. As of March 7, about 33% of U.S. hay-producing acreage (Figure 1) was considered under drought conditions, 7% less than a month earlier and the lowest percentage since last June. The area of drought-impacted alfalfa acreage (Figure 2) was down 9% from early February to 43% and represented the lowest percentage since last September. The lower percentages of acreage considered under drought are nearing multiyear lows.

Much of the improvement can be attributed to California. Elsewhere, drought areas in Michigan, Minnesota and Iowa shrunk, although frozen soils limited soil moisture penetration, and it’s still too early to determine the extent of winterkill.

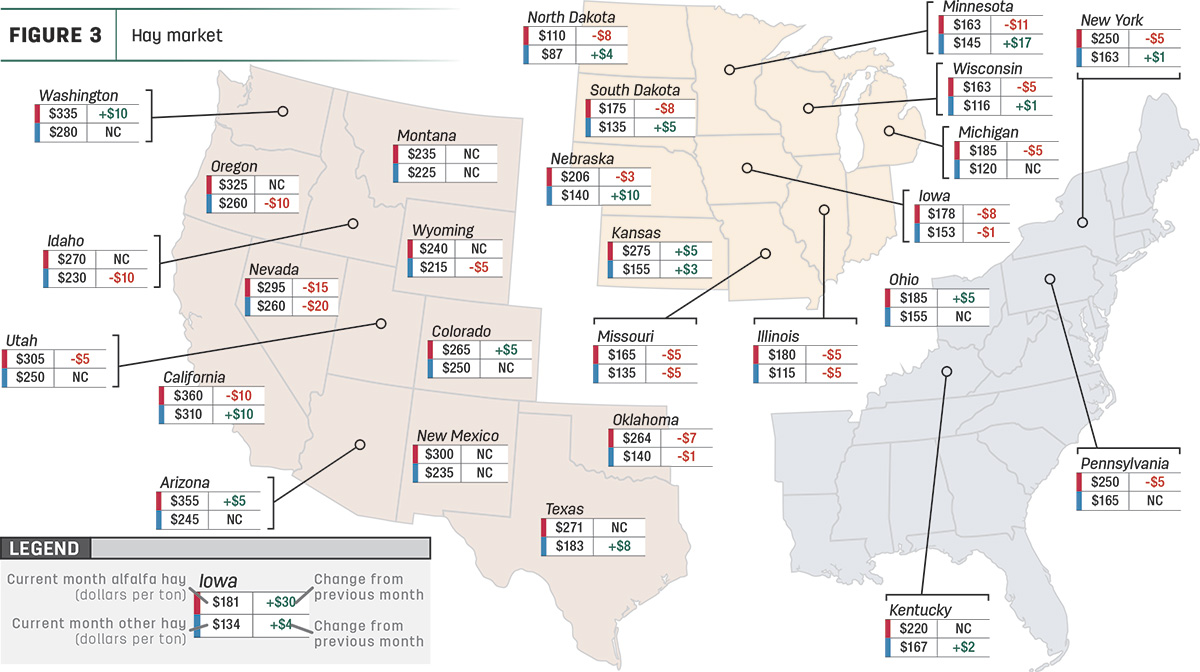

Hay prices tracked

Price data for 27 major hay-producing states is mapped in Figure 3, illustrating the most recent monthly average price and one-month change. The lag in USDA price reports and price averaging across several quality grades of hay may not always capture current markets, so check individual market reports elsewhere in Progressive Forage.

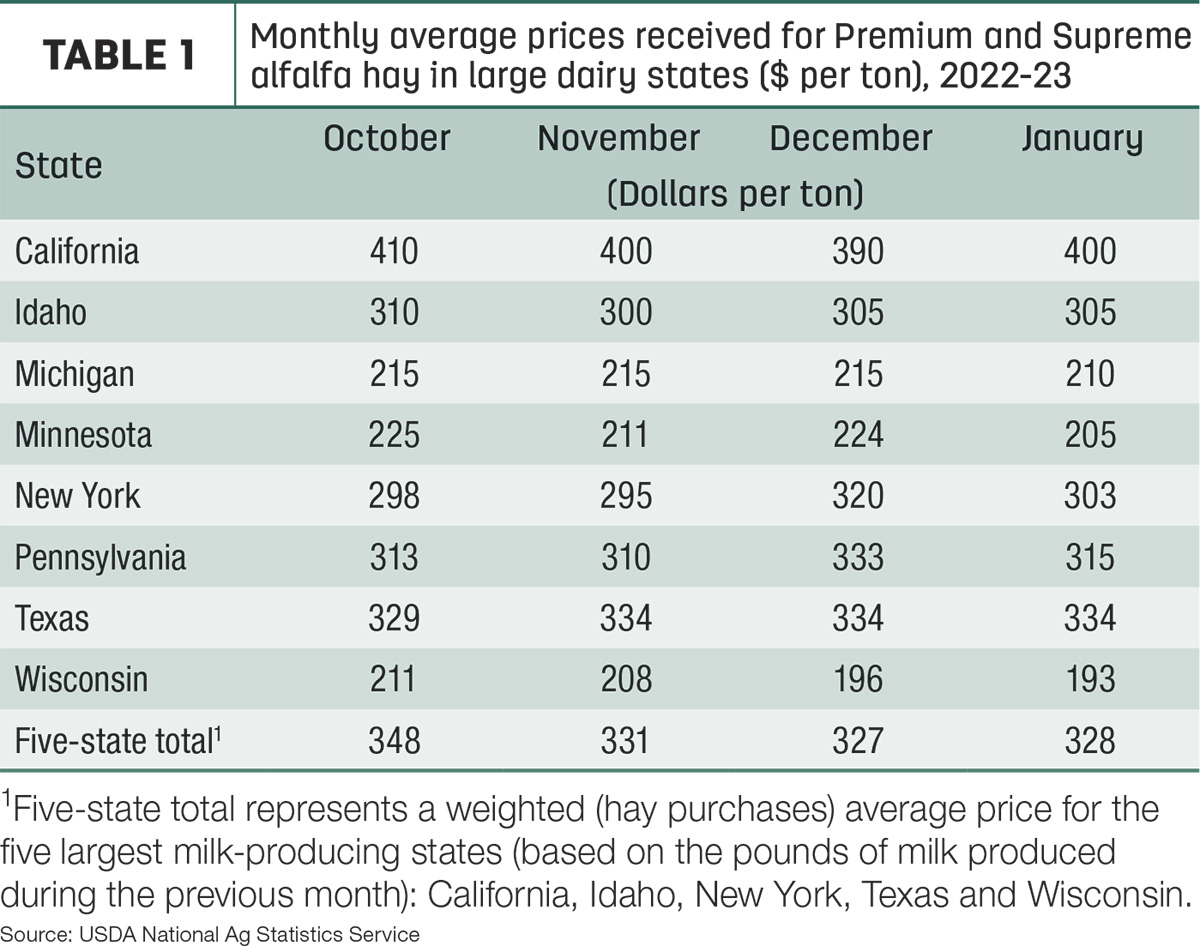

Dairy hay

At $328 per ton, January’s average price for Premium and Supreme alfalfa hay in the top milk-producing states increased $1 from December and was $66 higher than a year ago (Table 1). While prices were steady to slightly lower in most surveyed states, January average prices rose $10 per ton in California.

Alfalfa

Despite the average price increase for dairy-quality alfalfa hay, the U.S. average price for all alfalfa hay dipped $6 in January to $263 per ton. Prices increased in just five of 27 major forage states, led by a $10 increase in Washington. Prices were lower in 15 states, with Minnesota and Nevada down $11 and $15, respectively.

Year-over-year prices were up $100 or more in Arizona and Washington.

The spread between U.S. average alfalfa and other hay prices narrowed to about $88 per ton in January after averaging $92 in 2022.

Other hay

At $175 per ton, the January 2023 U.S. average price for other hay was down $2 per ton from December. Prices increased in 10 of 27 major hay-producing states, with largest month-to-month increases in Minnesota, California and Oklahoma. Largest declines were in Nevada, Idaho and Oregon.

January average prices for other hay were $50-$55 more than a year ago in California, Utah and Arizona, and up $22 nationally. Compared to a year ago, average prices slipped $20 per ton in Illinois, Michigan and North Dakota.

Hay exports start year weak

Regardless of type or category, January 2023 exports of most U.S. hay products were among the weakest in several years.

Exports of alfalfa hay were estimated at 142,959 metric tons (MT), the lowest monthly total since January-February 2015. At 77,688 MT, sales to China were the lowest since January 2021. China was the destination for about 54% of all U.S. alfalfa hay exports during the month. Sales to Japan totaled 22,691 MT, 16% of the month’s total.

Exports of dehydrated alfalfa cubes and dehydrated alfalfa meal both hit three-month lows at 3,855 MT and 1,314 MT, respectively; sales of sun-dried alfalfa cubes slipped to just 936 MT, the lowest volume since 2006.

Exports of other hay continued to fall, with January’s total at just 66,830 MT, the lowest monthly total since at least 2005. Sales to the major markets of Japan and South Korea continued downward trends started in the second half of 2022. Japan maintained its spot as the top market, taking about 58% of other hay shipments (38,880 MT) during the month, followed by South Korea at 18% (12,328 MT).

Regional markets

- Southwest: In Texas, hay prices remained steady to firm in all regions with very good demand. Supplemental livestock feeding continued.

In California, trade activity was moderate, and prices were firm on all hay markets. Dairy and export hay demand was light to moderate. Additional rounds of rain and snow added to the ample precipitation received across the West since December 2022.

In Oklahoma, hay trade and prices picked up as producers tried to make it to spring.

- Northwest: In Montana, hay sold generally steady on good to very good demand. Ranchers were buying hay on an as-needed basis. Loads of hay continued to be sent into the southern Plains as buyers in Texas, Oklahoma and Colorado remained active. Many of these loads were catching back hauls, which helped lower freight significantly.

In Idaho, old-crop sales were light. New-crop export contracts on the east part of the trade area were reported. Trade was slow with light to moderate demand. Inclement weather conditions affected the market. Most dairy sales were hand-to-mouth as buyers wait for new-crop trends.

In Colorado, trade was inactive on large squares of feedlot and dairy hay as growers raised asking prices.

In the Columbia Basin, activity was mostly light. Dairies were concerned about lower milk futures prices.

In Wyoming, all reported hay sold fully steady on good demand; sun-cured alfalfa pellets sold $20 higher. Most producers were almost out of hay. The bulk of the hay sold stayed in the local trade areas.

- Midwest: In Nebraska, all reported hay sales sold steady. Demand was good. Some snow melting helped take some pressure off the market as cows could graze winter feed resources. Quite a few loads of hay continue to be shipped in from North and South Dakota.

In Kansas, demand remained good, and prices remained mostly steady, but trade activity was slow. The western half of the state remained in drought, although areas surrounding western Kansas received some form of precipitation. As the drought lingers, so do concerns for this year's alfalfa crop.

In South Dakota, all types and classes of hay sold steady on very good demand. Supplies are very limited. There was a large snowpack to clear in the eastern half of the state, and more snow and colder temperatures were forecast. There was very good demand for cornstalks and straw as livestock producers tried to keep their stock comfortable during these rough conditions.

In Missouri, rain and warmer temperatures resulted in mud, limiting market activity. Some hay sales took place but business was slow. The supply of hay was light and prices were steady.

In Iowa, the market was steady to stronger on most categories of hay. Buyers were making preparations for another round of winter storms.

- East: In Pennsylvania, alfalfa and alfalfa-grass mix hay sold strong; orchardgrass, orchard-timothy and prairie-meadow grass sold with weaker undertones. Buyer demand was moderate on a moderate supply.

In Alabama, trade was moderate on light supply and moderate demand.

Other things we’re seeing

-

Dairy: January signaled the start of what is expected to be a year of tight dairy income margins, as high feed prices combine with weakening milk prices. With the milk income over feed cost margin calculated at $7.94 per hundredweight (cwt) in January, it triggered indemnity payments under the Dairy Margin Coverage (DMC) program. Based on current futures prices for milk and feed, that could be the largest margin into early autumn.

-

Cattle: Cattle feedlots are becoming fewer and larger, according to David Anderson, professor and economist with the Texas A&M AgriLife Extension Service. The USDA’s latest Cattle on Feed report indicated there were 26,093 feedlots in the U.S. in 2022, down 1,027 from the year before. The smallest category reported, less than 1,000 head, declined by 1,000 to 24,000 feedlots. Each feedlot size category with fewer than 7,999 head declined in number between 2021 and 2022. Each size category over 8,000 head either had the same number or grew in number. Two more feedlots with over 50,000 head were reported in 2022. Feedlots in that largest category marketed about 35.2% of fed cattle marketings, up from 34.6% in 2021.

-

Fuel: Weekly fuel prices are fluctuating but remain well below a year ago, according to the U.S. Energy Information Administration (EIA). The U.S. retail price for regular-grade gasoline averaged $3.39 per gallon on March 6, up a nickel from the previous week but down 71 cents from a year earlier. The average U.S. on-highway price of diesel was $4.28 per gallon, a penny per gallon below the prior week and 57 cents less than early March 2022.

-

Fertilizer: End-of-February analysis by ag economists at the University of Illinois and Ohio State University indicated fertilizer prices have been on a declining trend in recent months. Based on USDA Ag Marketing Service data for Illinois, average anhydrous ammonia prices fell 14% ($197 per ton) between Nov. 3, 2022, and Feb. 23, 2023. Diammonium phosphate (DAP) and potash prices declined about $124 and $221 per ton, respectively, between Dec. 15, 2022, and Feb. 23, 2023. While fertilizer prices have declined in recent weeks, current prices are still high by historical standards. Moreover, much of phosphate and potash applications occurred last fall. Those applications, along with fall-applied nitrogen, were made before price declines. In these cases, fertilizer price declines may provide reduced costs for 2024 but will not have an impact on 2023 fertilizer costs.

- Trucking: Spot flatbed prices were fairly steady entering the second month of the year, according to DAT Trendlines. Regionally, average spot prices per mile were: Southeast – $2.73, Midwest – $3.01, South – $2.65, Northeast – $2.73 and West – $2.29.