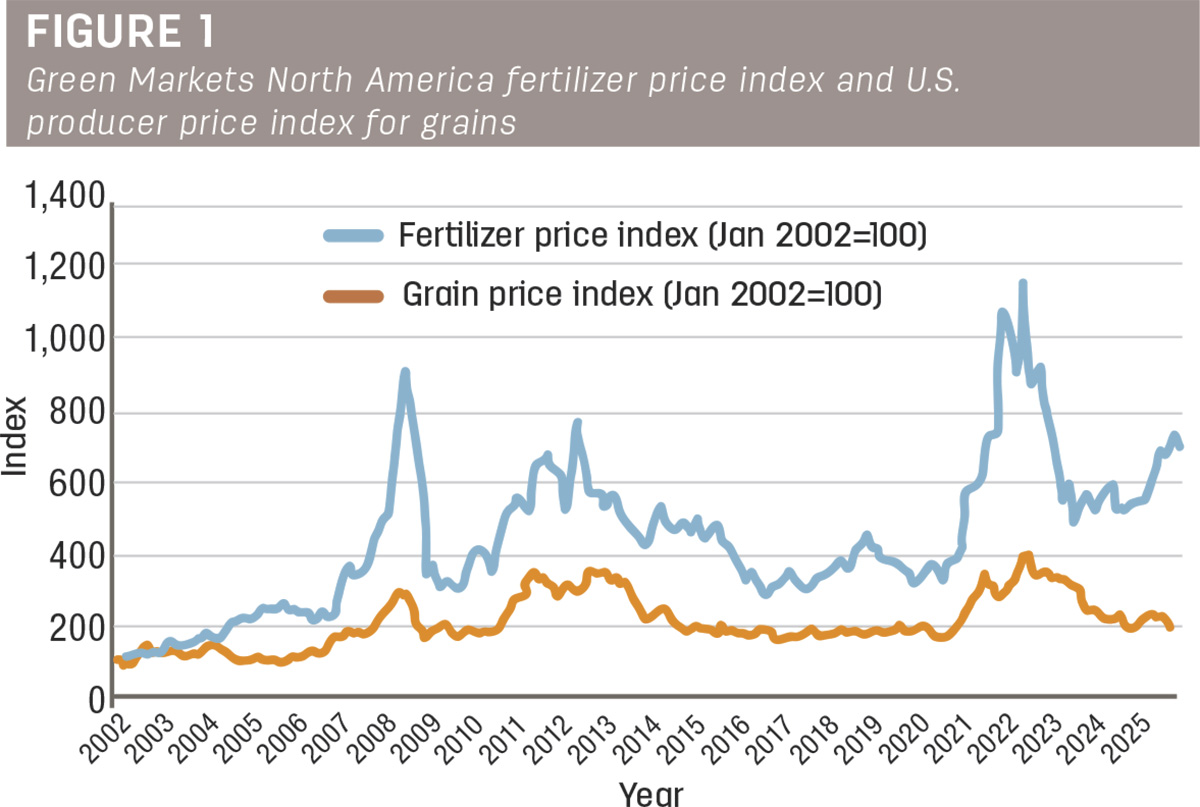

Fertilizer prices have eased since the 2022 spike, but for most farmers, they still feel painfully high. Figure 1 compares the North America fertilizer price index with the U.S. producer price index for grains, both standardized to 100 in January 2002. Fertilizer prices have shown far greater volatility than grain prices, with sharp spikes in 2008 and again in 2022 following the Russia-Ukraine war. Although prices have dropped from their 2022 peak, they remain about twice as high as prepandemic levels, while grain prices have fallen back to near pre-2020 levels. This widening gap in 2025 reflects a growing concern for producers: High fertilizer costs and weaker crop prices continue to squeeze farm margins.

Many factors are keeping fertilizer prices elevated. Fertilizer is a global commodity, and its prices are shaped by international supply and demand rather than domestic factors alone. Meanwhile, production and trade are concentrated in just a few countries. Morocco, China, Saudi Arabia, Russia and the U.S. account for most of phosphate exports, while Canada, Russia and Belarus dominate potash. Nitrogen is produced more widely, but the U.S. still relies heavily on imports. In fact, about one- quarter of all fertilizers used in the U.S. come from abroad.

Nitrogen (N)

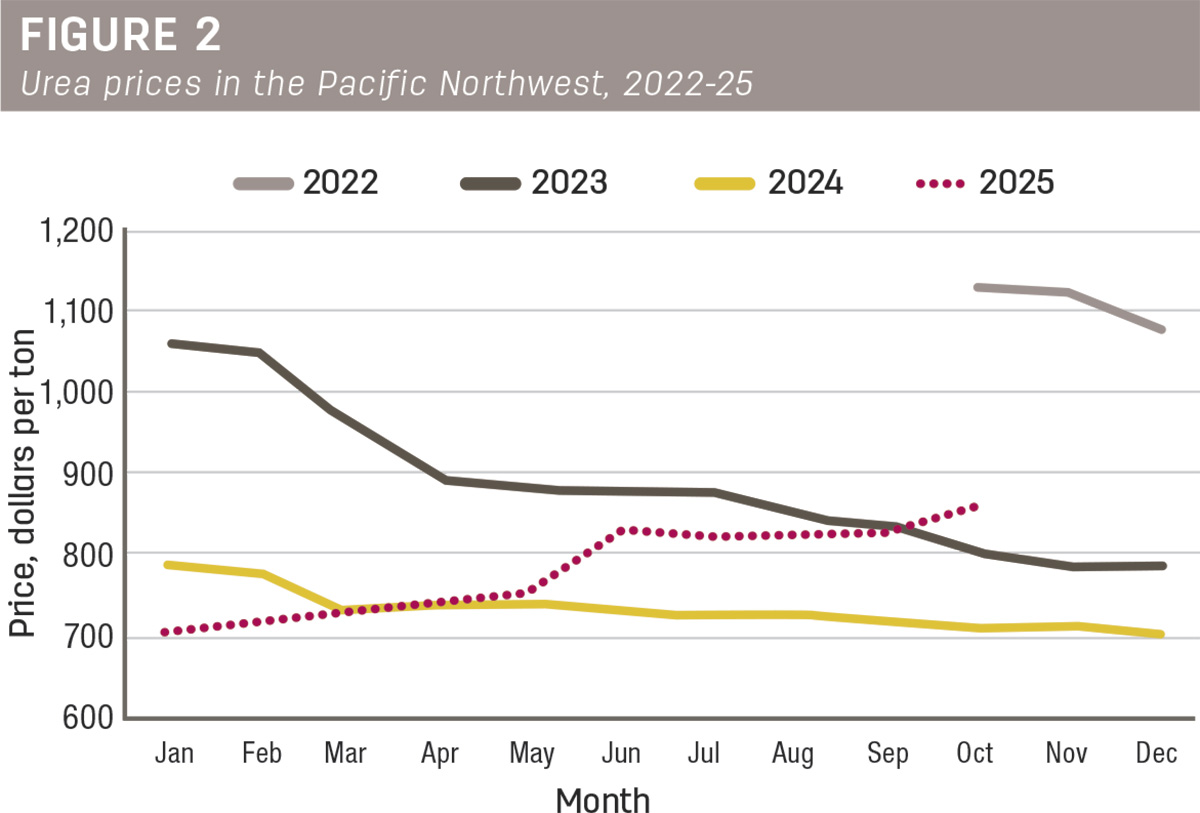

Nitrogen fertilizer prices have climbed sharply this year. Figure 2 shows monthly urea prices in the Pacific Northwest (PNW), which the USDA began tracking in late 2022. Urea is the most widely used nitrogen fertilizer in the world and serves as a benchmark for other nitrogen products. In October 2025, urea prices in the region were more than 20% higher than a year earlier.

Much of this increase comes from a continued squeeze on global supply. China, the world’s largest urea producer, has restricted exports to stabilize domestic prices. In 2024, it shipped just 0.26 million metric tons (mmt), down from 5.45 mmt in 2020. Although China began easing export restrictions in mid-2025, the added supply has not lowered prices meaningfully. Temporary shutdowns in Iran and Egypt (two major exporters) during the Israel-Iran conflict in mid-2025 further tightened availability. Further, Europe’s fertilizer industry is still recovering from the energy crisis that followed the Russia-Ukraine war. The high natural gas prices in 2022 forced many plants to shut down. Today, Europe’s output remains about 25% (roughly 3 million tons of urea) below prewar levels.

Prices for other nitrogen fertilizers have followed a similar pattern. With limited global capacity, any supply disruption or geopolitical tension can push prices higher. Building new plants requires years of planning and major investment, so additional production will take time to come online. In the meantime, the U.S. remains dependent on nitrogen imports from Russia, leaving domestic prices exposed to future tariffs or trade restrictions.

Phosphate (P)

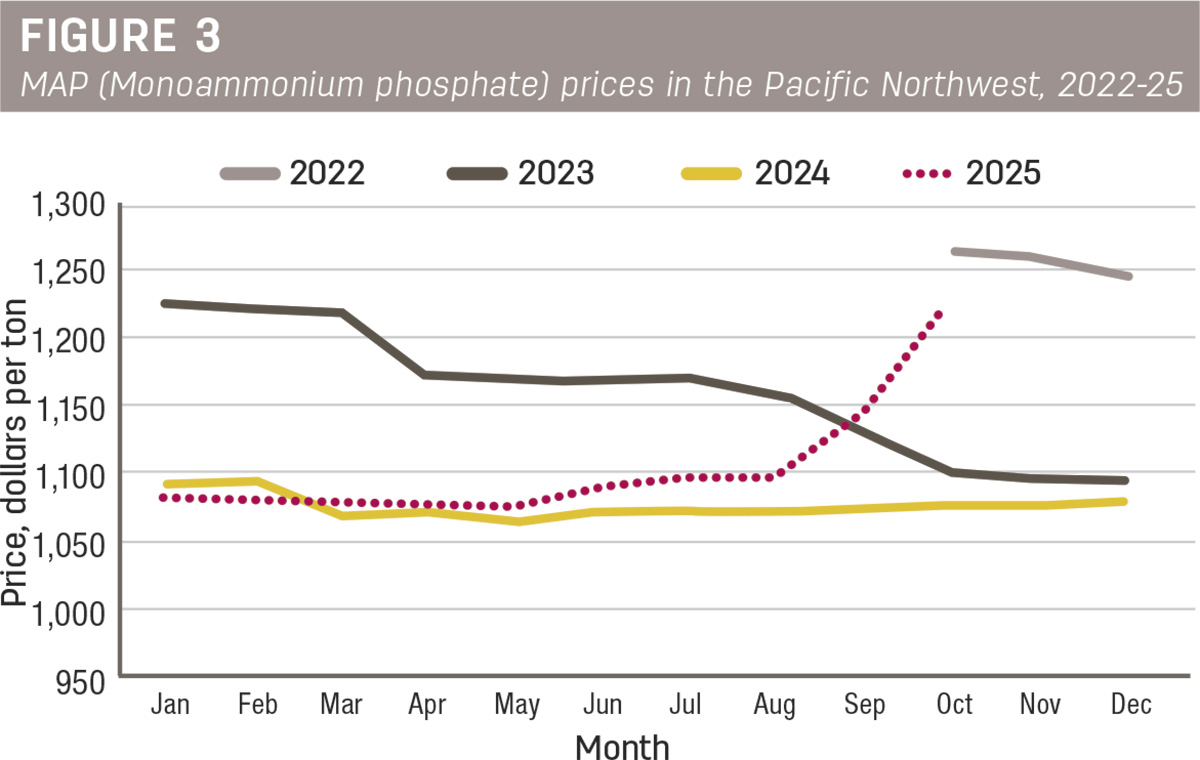

Phosphate prices have also risen sharply in 2025. Figure 3 shows that monoammonium phosphate (MAP) prices in the PNW were more than 10% higher in October 2025 than a year earlier. As with nitrogen fertilizers, tight global supply continues to support elevated prices.

Domestically, phosphate production has dropped by more than 60% over the past two decades. Much of this decline reflects structural changes in the industry, but recent natural disasters in Florida, the main source of U.S. phosphate production, have further disrupted supply.

Globally, China, once a major exporter, has cut its phosphate exports by nearly half. This decline is partly due to China’s efforts to stabilize domestic prices and to divert phosphate into its booming lithium iron phosphate battery industry. India, one of the largest fertilizer consumers, has also struggled to rebuild its phosphate stocks. Because Indian farmers pay a heavily subsidized price for fertilizer, importers have continued buying even as global prices have climbed, pushing prices even higher.

Trade policies have also created uncertainty in the market. Currently, most U.S. phosphate imports come from Peru. Imports from major exporters such as Morocco, Russia, China and Saudi Arabia are subject to either tariffs alone or a combination of countervailing duties and tariffs, adding to farmers’ costs.

Potential relief in the market depends on new production capacity. Several projects in Saudi Arabia, Egypt and Morocco could help ease the tight supply, but most of these developments are years away from full operation. The most immediate price relief would come from increasing Chinese exports and lowering tariffs, both of which depend on political decisions in the U.S. and China.

Potash (K)

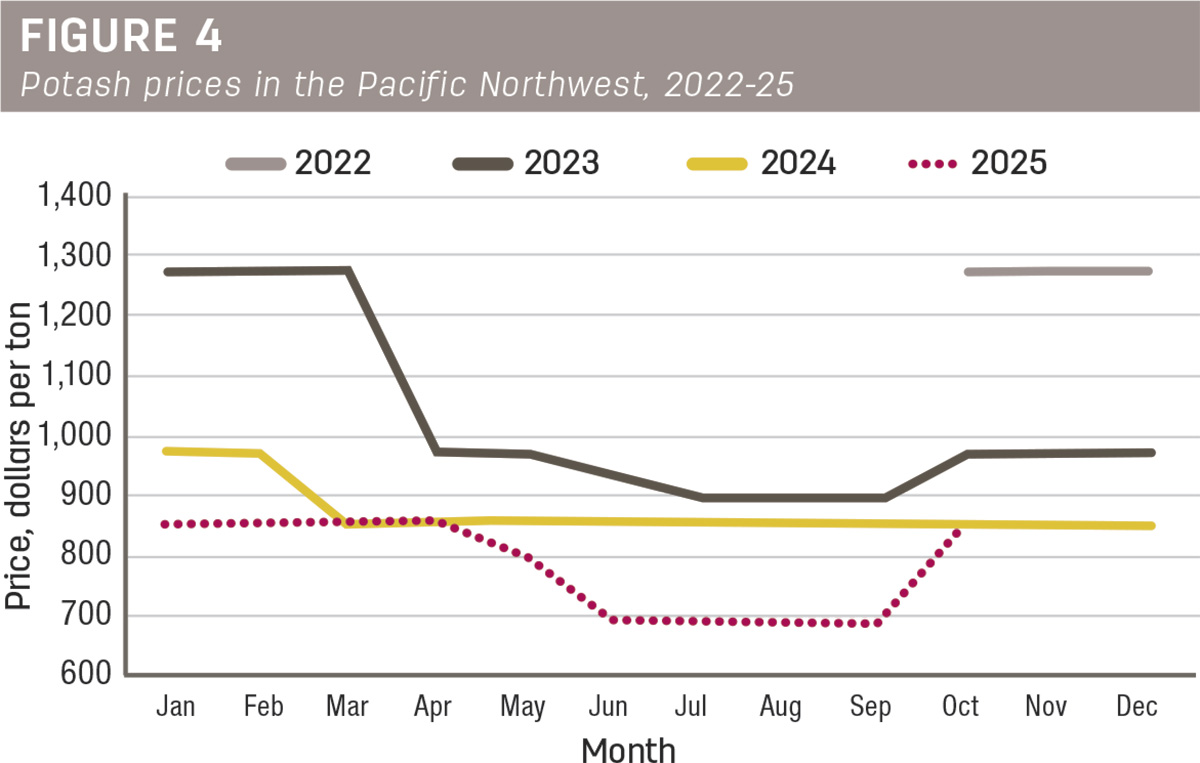

Potash is the only fertilizer market showing some stability in 2025. As shown in Figure 4, potash prices in the PNW have held steady or edged slightly lower compared with last year. As of October, average potash prices in the region were similar to last year’s.

The U.S. relies heavily on Canada for potash, which supplies more than 80% of total domestic consumption. Additionally, potash imports that meet the requirements of the Canada-United States-Mexico Agreement (CUSMA) are not subject to tariffs.

Globally, potash production and exports have largely recovered to prewar levels and should continue rising as new projects come online. One major development is the BHP Jansen project in Canada, set to become one of the world’s largest potash mines with an annual capacity of 8.5 million metric tons. Additional investments in Laos, which has significant potassium chloride reserves, will further expand global supply. Within the U.S., although production has declined in recent years, new projects in Michigan and Utah are expected to increase domestic output.

Looking ahead to 2026

While challenges remain, there are reasons for cautious optimism. Fertilizer prices are unlikely to return to prewar levels soon, but they could stabilize as global supply conditions improve. Several developments may help lower costs. Continued easing of China’s export restrictions could bring more nitrogen and phosphate fertilizers to world markets. A resolution to the Russia-Ukraine conflict would restore exports from Russia and Belarus, adding much-needed supply. Meanwhile, new and expanding plants in North America, the Middle East and Asia are expected to come online in the next few years, gradually increasing production capacity. Tariffs and trade policies still pose uncertainties, but if these supply-side improvements materialize, the fertilizer market could move toward a more balanced environment in 2026.

.webp?height=auto&t=1783636475&width=285 "63802-Thomas-GPS-equipment--Automated-Magnum-Tractor--Matt-Skinner-photo(1).jpg")