Far away from the Strait of Hormuz, the new oil crunch prices are hitting closer to home.

While it’s gone from $2.99 to $3.69 in Jerome, Idaho, the price of regular unleaded gas jumped from $2.55 per gallon to $3.10 in Sauk Centre, Minnesota, and from $3.15 to $3.59 in Watertown, New York.

The heartland of Eudora, Kansas, where gas is typically cheaper than the national average, saw prices go from $2.94 to $3.20 per gallon in a week. Even in the hearty oil country of west Texas, the price of gas in Lubbock spiked from $2.34 in mid-February to $3.23 per gallon on March 12, according to AAA’s fuel price map.

But the prices are expected to keep climbing according to economists in the energy and commodity sectors, as the U.S. and Israel continue strike operations against Iran, and Iran responds with missiles and threats against oil tankers in the Middle East.

The largest increase in prices came this week as Iran made a blockade threatening oil barges trying to travel through the Strait of Hormuz, the main sea route in the south Persian Gulf used for oil shipments. With no way to move tankers over the strait, daily oil production in Iraq, Saudi Arabia, Kuwait and the United Arab Emirates has collectively been cut one-third in total capacity since the war’s start, and it could be cut more.

“We need the Strait of Hormuz to reopen, and we need it to reopen now,” said Matt McClain, a petroleum market analyst for GasBuddy. “Bottom line, that's what we need – that fixes everything.

“The conflict can continue for all intents and purposes. Whether that's a popular or unpopular decision in this country, as far as oil prices goes, that would be irrelevant. But the Strait of Hormuz being secured and oil flowing freely again to sort of separate it from the conflict, that solves our oil problem.”

Many have questioned how the blockade has led to drastic gasoline price increases in the U.S., when 80% of the oil coming through the Strait of Hormuz goes to Asia. But McLain says that total portion is actually 20% of the total world supply; it puts a dent in the global supply and demand.

“The crude oil market is a global market exchange based in U.S. dollars, and even if it wasn't, we have still removed 20 percent of the world's oil supply. It doesn't matter if it's steaks, bananas, it doesn't matter what the commodity is; if you remove 20 percent from the supply, the remaining 80 percent is going to cost more. When you decrease production, all of a sudden you've got an uptick on what remains.”

Many consumers also ask how the U.S. can be short in supply when domestic production of oil, gas and natural gas has been higher and remained higher since the Obama administration. But McLain said much of the energy produced in the U.S. continues to be sold elsewhere, and we continue to import oil as well.

“We have more oil than we know what to do with, it's not a supply issue,” he said of U.S. markets. “We're not having a supply issue. We have a price issue. It's a very big difference between the two.

“The market is globally interlinked together. Because not every country has oil to produce. That's how we operate, and that's why something that happens on the other side of the globe can impact prices here. But as far as supplies, we export oil, so does Canada. Canada exports oil to the middle part of this country. Any person who's talking with you in the Midwest, their refinery, their gasoline, probably came from Canada more so than even our own domestic supply, but it's all North American-based.”

How long will fighting last?

In a March 6 webinar from Rabobank’s Knowledge Team, Jan Lambregts, head of RaboResearch global economics and markets, said the length of the conflicts, as well as its overall disruptions and attacks, are the two most relevant factors.

“The longer the Strait of Hormuz is closed, the more these facilities get damaged, the bigger the impact becomes in the energy markets and other markets,” he said. “If it is closed for an extended period, you will see higher energy prices – and from that, higher inflation impact and more negative impact on growth. And if that is combined or separately, also associated with destruction of critical energy infrastructure that takes significant time to rebuild, the impact could be even bigger.”

Lambregts added that a longer conflict creates more volatility for energy markets. But an even bigger risk could come with regime change in Iran followed by “jihadi chaos.”

“That would be market chaos,” Lambregts said. “It would be bad for Trump and his agenda, but it wouldn't be good for the rest of the world. If he loses because the regime simply survives this, that may be a calmer scenario, but it would also be quite the loss for the West, and severely make people doubt what the U.S. is still capable of.”

Fertilizer and fuel for ag

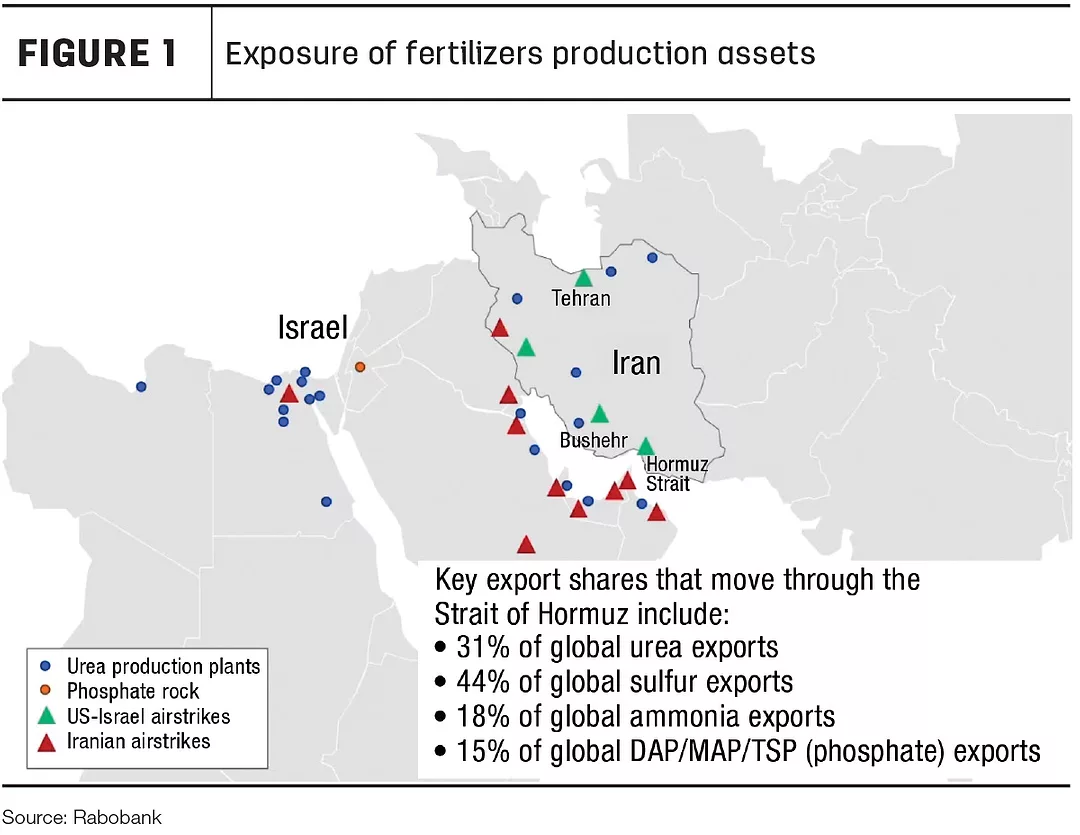

Later in the Rabobank webinar, Andrick Payen, an analyst in global agribusiness, said the Strait of Hormuz also sees a high volume of fertilizer production travel through it, with 31% of global urea exports, 44% of sulfur exports, 18% of ammonia and 15% of phosphate exports coming from the region (see Figure 1).

“We’ve seen more than anything urea and other prices increase due to the risk and low supply that is expected to come through the next coming weeks,” Payen said.

Many regions of the globe already made fertilizer purchases before the Iran conflict started, including much of the U.S., Payen said. But with urea used for nitrogen applications, and crops such as corn, wheat, cotton, potatoes, vegetables and sugarbeets being nitrogen-intensive, supply cost will be critical if producers haven’t made planting decisions.

“For farmers that haven’t locked in prices at the moment, they’re the ones that stand the risk right now seeing higher prices.”

“In the southern [U.S.] there has already been applications being made into fields … However, closer to the Corn Belt, that’s where we could see potentially some switch or changes on planting decisions.

“We won’t know the extent of the switch on corn, soybeans acres in the U.S. until everything is said and done. That’s probably going to come in June.”

"Transportation of shipping commodities will play a significant cost as harvest comes into the picture later in the year,” Payen added (see Table 1). “Given that energy prices continue to trend higher, and depending how long they stay, we're likely going to see all types of transportation impact.

“Farmers are likely going to see more pressure on the downside on prices, given that most likely higher transportation costs will result in adjusting prices, which ultimately will impact them in the long run.”