U.S. milk production momentum pushed through the final month of 2016, gaining strength from more cows and greater milk output per cow.

Momentum is built on mass and velocity, and December continued a four-month roll in which U.S. milk production increased at least 2 percent from the same month a year earlier. USDA’s monthly milk report estimated total December 2016 U.S. production at 17.86 billion pounds, up 2.2 percent from December 2015. Production in the 23 major dairy states was estimated at 16.78 billion pounds, up 2.4 percent.

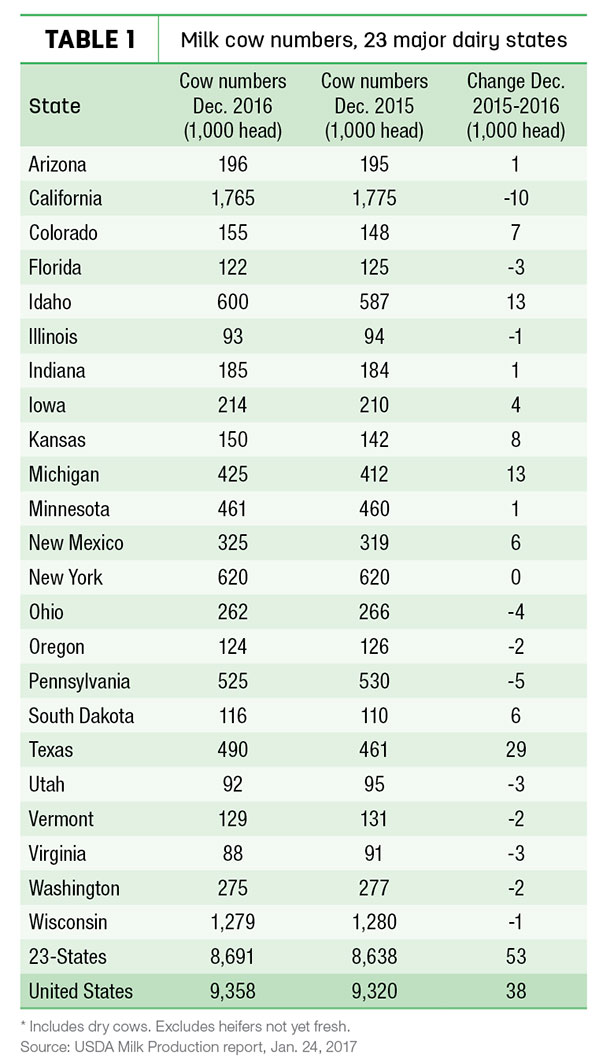

December 2016 U.S. cow numbers were up 38,000 head compared to a year earlier, and up 53,000 head in the major states (Table 1). Thanks to genetics as well as feed and management, milk production per cow in the 23 major states was the highest December total since USDA started tracking those numbers in 2003.

With December’s preliminary estimates, total 2016 U.S. milk production will hit 212.5 billion pounds, 1.9 percent more than 2015, according to Bob Cropp, professor emeritus at the University of Wisconsin-Madison. While annual average cow numbers were up 0.2 percent from 2015, to 9.33 million head, 2016 milk output per cow rose 1.7 percent, to 22,770 pounds.

Regional patterns

With slight alterations, recent regional patterns prevailed, Cropp said in his monthly dairy situation and outlook report. Strong-but-lower milk production growth continued across the Northeast and Midwest. While most of those states had steady cow numbers, Michigan’s herd grew by 13,000 from a year ago.

Texas posted a 11.7 percent milk production jump in December, and it appears fully recovered from the impact of Snowstorm Goliath. Cow numbers were up 29,000 head from a year ago. Elsewhere, cow numbers were 13,000 head higher in Idaho, 8,000 in Kansas, 7,000 higher in Colorado and 6,000 in both South Dakota and New Mexico.

California cow numbers were down 10,000 from last year, but total milk output was up fractionally in December, ending the fourth quarter up about 0.9 percent compared to the same period a year earlier.

Price recap, outlook

Good domestic butter and cheese sales and improved exports held milk prices up at the end of 2016, much improved over the first half of the year, Cropp said.

The Class III averaged just $13.48 per hundredweight (cwt) for the first half of the year, but improved to $16.25 per cwt for the second half. The Class IV price averaged $13.18 per cwt for the first half of 2016, rising to $14.36 per cwt for the second half. December 2016 Class III and Class IV prices were highs for the year.

Milk prices are forecast to improve in 2017, although there will be some backsliding early in the year. The January Class III price (about $16.50 per cwt) will fall from the December high, but the January Class IV price (about $16 per cwt) will be higher, Cropp said. However, unless cheese prices rebound, the Class III could fall below $16 per cwt for February.

Looking ahead, Cropp projects the Class III should stay in the $16s per cwt through May or June, and then move into the $17s for the remainder of the year, yielding an average more than $2 per cwt higher than 2016. The Class IV price could be in the $16s for the first quarter of 2017, then into the $17s for the remainder of the year.

How much milk prices improve will depend on whether domestic and global demand can keep pace with production. USDA’s latest forecast expects U.S. cow numbers to increase 0.4 percent in 2017, with milk per cow to increase 1.8 percent. That would result in another 2.2 percent milk production gain in 2017.

Any changes in expected milk production, sales or exports could result in quite different prices, Cropp warned. Dairy producers may want to use some price risk management tools to take advantage of the current futures prices. As of Jan. 24, 2017, Class III futures averaged $17.52 per cwt for the year; Class IV futures averaged $17.19 per cwt.

“Continued growth in the economy and improved consumer confidence (bodes) well for good sales,” Cropp said. “Milk production for four of the major exporters—the European Union, New Zealand, Australia and Argentina—are expected to be lower than a year ago and not expected to show increases any time before the second half of the year. The U.S. is the only major exporter experiencing higher milk production. World demand is also improving with more activity from China, Southeast Asia and others. The world supply and demand is slowly tightening and world dairy product prices are increasing. These are favorable factors for growth in U.S. dairy exports.” ![]()

-

Dave Natzke

- Editor

- Progressive Dairyman

- Email Dave Natzke