The USDA National Agricultural Statistics Service (NASS) Agricultural Prices report, released May 29, established last month’s Dairy Margin Coverage (DMC) program calculations. The price for all key feedstuffs used to calculate the margin rose in April, revealing an income over feed cost of $10.54 per hundredweight (cwt), more than $1 above the highest coverage selection in Tier I and comfortably positioning those enrolled in the program in the clear of indemnity payments.

A peek at April DMC

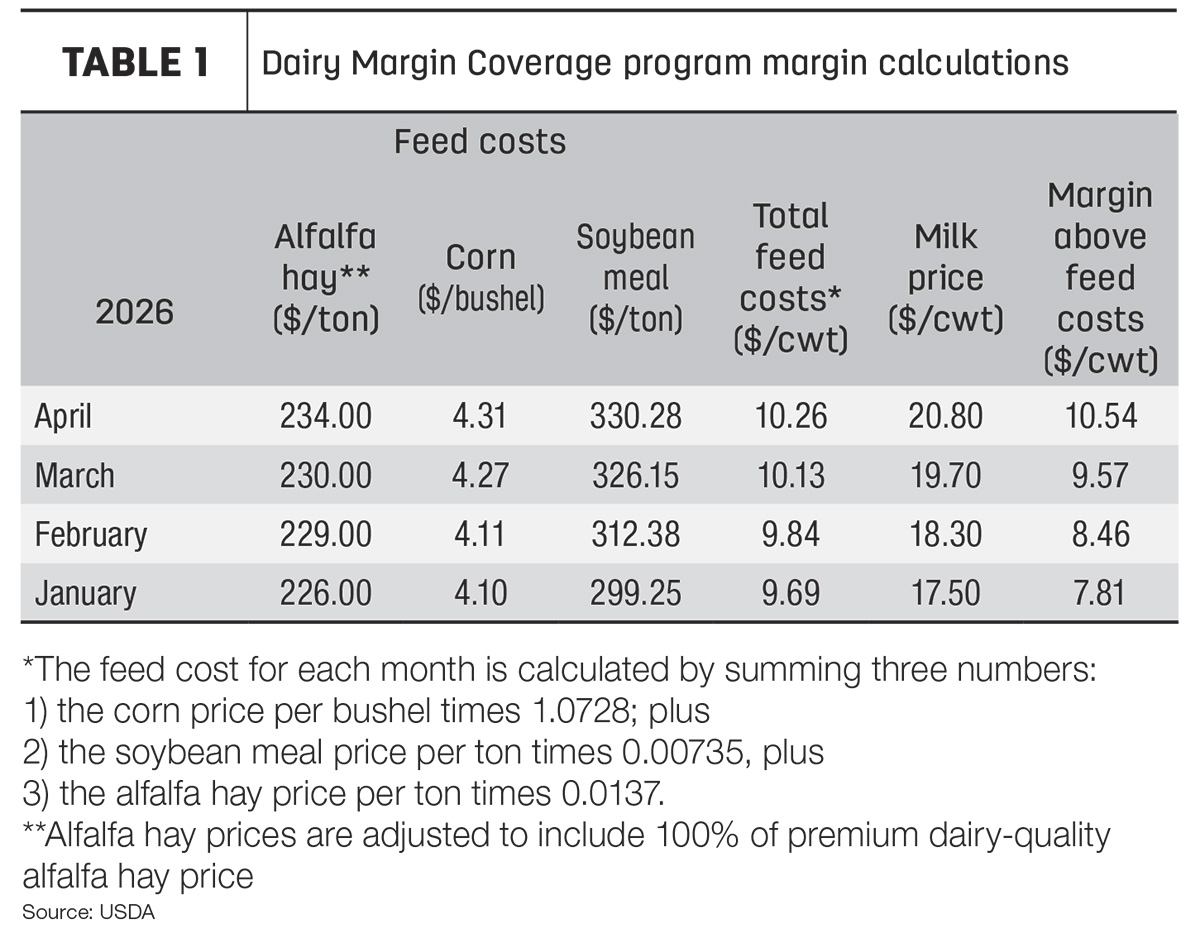

Prices for major dairy feedstuffs that influence the DMC program margin were reported in April’s USDA Agricultural Prices report (see Table 1).

DMC program margin factors for April compared to March were as follows:

- Dairy alfalfa hay: $234 per ton, up $4

- Corn: $4.31 per bushel, up 4 cents

- Soybean meal: $330.28 per ton, up $4.13

- Total feed costs: $10.26 per cwt, up 13 cents

- Milk price: $20.80 per cwt, up $1.10

- Margin above feed cost: $10.54 per cwt, up 97 cents

Milk prices continue spring rally

All-milk prices in the 24 major dairy states continued to rally in April. On average, the all-milk price was $20.80 per cwt, up $1.10 per cwt from the previous month and a shy 30 cents under April 2025 (Table 2).

Looking at the all-milk price on a state-by-state basis, every one of the 24 major dairy states saw an improvement, albeit varying from as little as 40 cents in Iowa to garner an all-milk price of $19.70 per cwt, to as large as $2.50 in Florida for an all-milk price of $24.90 per cwt. Two additional states recorded an all-milk price in April that was more than $2 above the previous month; those were Georgia, up $2.20 to $25.30 per cwt, and Virginia, up $2.20 also to $25 per cwt. Seven other states joined Iowa in all-milk price improvements below $1, whereas the rest fell somewhere in between.

As prices improved in April, they still lagged from the same month last year for many of the 24 major dairy states. Only six states recorded an all-milk price in April that was no different or better than April 2025. Colorado saw the steepest price decline of $1.70 per cwt comparing last month’s $19.60 per cwt to April 2025’s $21.30 per cwt, whereas Florida did not see a change in price.

Feed costs gain strength

April’s feed costs are reflective of a market that is regaining strength, particularly for corn and soybean meal. The price per bushel for corn was up 4 cents in April from March but remained 31 cents below April 2025. On the contrary, the price for soybean meal improved $4 and change from the previous month and was up $35.25 per ton from April last year.

The DMC feed cost for each month is calculated by summing three numbers: 1) the corn price per bushel times 1.0728; plus 2) the soybean meal price per ton times 0.00735; plus 3) the alfalfa hay price per ton times 0.0137.

Overall, a substantially improved all-milk price drove the DMC margin to $10.54 per cwt in April and the highest margin in 2026 to date. This was $1.04 above the Tier I $9.50 per cwt coverage level and will result in no indemnity payments for enrolled operations.

Looking ahead

The DMC margin forecast for May is predicted to be 51 cents higher than last month’s with both feed costs and milk prices moving in the right direction. As of May 28, the all-milk price forecast for May was up to $21.43 per cwt, and the feed cost forecast was also up to $10.38 per cwt, bringing the month’s DMC margin forecast to $11.05 per cwt. While it appears both soybean meal and alfalfa hay prices will rise, the price of corn is forecast to fall more than 10 cents, the contributing factor in reining in the feed cost. At the time of this writing, this is the largest expected margin to date for 2026 and likely the largest one until November, when the margin is predicted to move to $11.17 per cwt. However, the markets will change.