Dairy markets are moving on from the dog days of summer. Time to review as we kick off the new season.

July milk prices steady

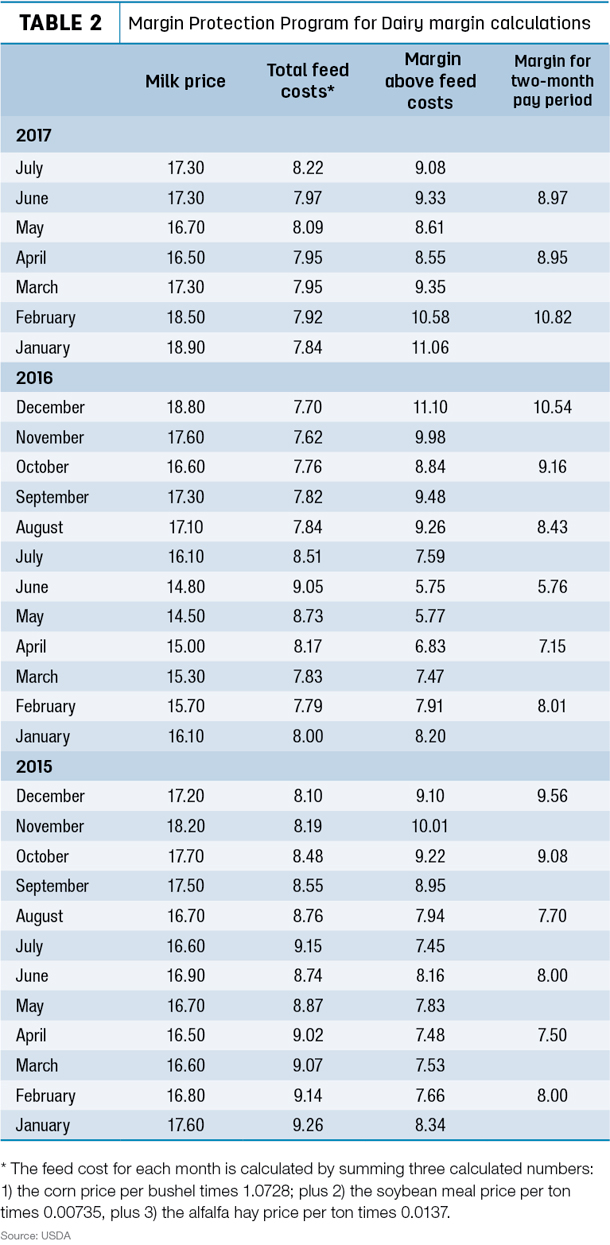

While July’s average milk price remained on a leash, feed costs increased prior to August crop production estimates, taking a small bite out of dairy income, based on the USDA’s monthly Margin Protection Program for Dairy (MPP-Dairy) calculations.

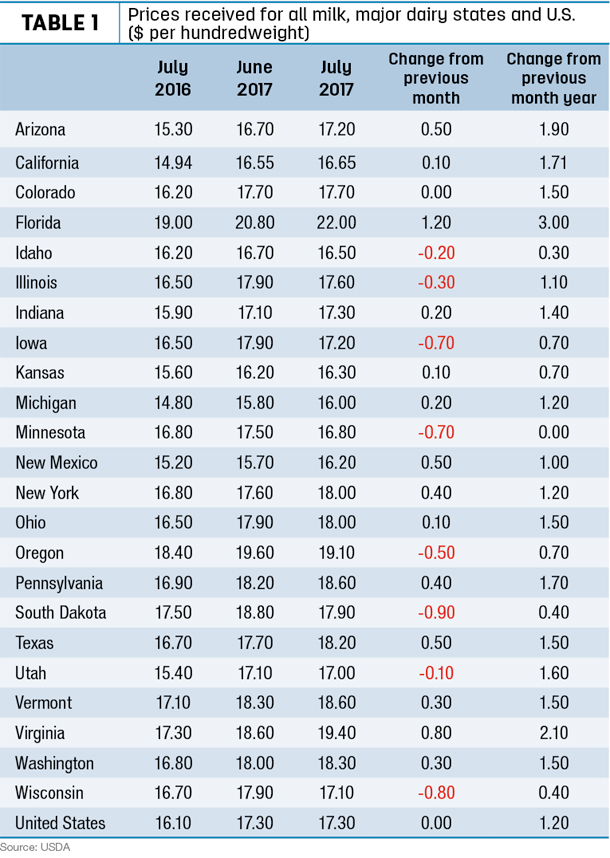

July 2017’s U.S. average milk price of $17.30 per hundredweight (cwt) was unchanged from June, but up $1.20 compared to July 2016, according to the USDA’s monthly Ag Prices report. The January-July 2017 average of $17.50 cwt is $2.13 per cwt more than the same period a year earlier.

Among individual major states (Table 1), Florida (up $1.20), Virginia (up 80 cents) and Arizona (up 50 cents) saw the largest increases compared to June. Eight states saw price declines, led by South Dakota (-90 cents), Wisconsin (-80 cents) and Iowa and Minnesota (both -70 cents).

Compared to a year earlier, July 2017 milk prices were up $3 per cwt in Florida, and $1.70 or more per cwt in Arizona, California, Pennsylvania and Virginia.

MPP-Dairy margin shrinks

The steady U.S. average milk price failed to keep pace with higher feed costs used in MPP-Dairy margin calculations.

The U.S. average price for corn received by growers was up 6 cents from June, to $3.49 per bushel. At $326.04, soybean meal was up more than $25 per ton. Alfalfa hay averaged $152 per ton, unchanged from June. The overall feed cost was $8.22 per cwt of milk sold, up 25 cents from June (Table 2).

Subtracted from the average milk price, the July MPP-Dairy income margin was $9.08 per cwt, also down 25 cents from June.

The July MPP-Dairy calculations are the first half of two-month factors used to determine potential payments for the July-August pay period. The August margin will be announced Sept. 28.

Milk prices exhibited volatility in the first half of August, but feed prices declined following USDA’s August crop production forecast. The lower feed costs more than offset some milk price weakness, lending strength to dairy margins, according to Commodity & Ingredient Hedging LLC.

Thanks to a jump in the value of protein, August federal and California milk marketing order minimum prices are somewhat higher than July, which should boost the U.S. average milk price for the month. But dairy commodity markets remain turbulent, said John Geuss, dairy consultant. The dominant force for milk prices is the wholesale cheese price. The August federal order milk protein price was $1.55 per pound in August, up from $1.22 per pound in July. The change in August was welcomed, but may be short lived.

September Class III/IV futures prices tumbled to close out August. As of Aug. 31, September Class III futures had fallen $1 per cwt from Aug. 18, to $16.20 per cwt. October 2017-January 2018 futures prices fell between 58-75 cents per cwt. Fourth-quarter 2017 Class IV prices were down 31-40 cents per cwt.

As of Sept. 1, the Program on Dairy Markets and Policy projected monthly MPP-Dairy margins to rise during the next several months, peaking at about $10 per cwt in October-December, before dipping closer to $9 per cwt in the first quarter of 2018. Although conditions may change, those margins remain above MPP-Dairy indemnity payment triggers.

Read also: USDA offers 2018 MPP-Dairy opt-out option

Dairy cow slaughter higher

The number of dairy cows culled in 2017 continues to run ahead of a year earlier, but the dairy herd is larger too.

For July 2017, federally inspected milk cow slaughter was estimated at 225,800 head, 12,500 more than July 2016, but 10,900 less than June 2017.

Through the first seven months of 2017, dairy cows slaughtered under federal inspection were estimated at 1.72 million head, about 58,600 more than January-July 2016.

However, as a percentage of the U.S. to dairy herd, the pace of culling has slowed since the first quarter of the year. USDA’s milk production report estimated the second quarter 2017 U.S. dairy herd averaged 9.399 million, about 76,000 head larger than the same quarter a year ago. Culling for that quarter was 702,000 head, about 7.4 percent of the herd, down about 1 percent from the first quarter of 2017.

Cull cow prices better

Cull cow prices showed improvement for a seventh consecutive month. Including beef and dairy cows, the July 2017 cutter cow price averaged $77.30 per hundredweight (cwt), about 80 cents more than June, and $16 per cwt higher than last December, but still $4.20 less than July 2016.

USDA’s latest projections estimate cutter cow prices will be in a range of $67-$71 per cwt in the third quarter of 2017, and end the year in a range of $67-$69. The 2016 average was $70 per cwt, after averaging $99.50 cwt in 2015 and $102 per cwt in 2014.

Heavy culling impacting organic cow prices

Heavy culling among organic dairy herds is apparently driving organic cull cow prices lower, according to the USDA’s Organic Dairy Market News.

At an auction in Oregon, Aug. 24, organic cows sold for slaughter at lower prices than conventional cows. The top 10 organic cows auctioned brought an average price of $66.76 per cwt, compared with a $78.05 per cwt average for the top 10 conventional cows. Observers suggested the weakness of organic cow prices was an indicator of increased organic herd culling in the face of lower organic milk pay prices, as cash-squeezed organic dairy producers seek to both reduce herds and raise additional cash.

Producer quotas on volumes of organic milk some processors will buy under contracts has also accelerated organic herd reductions, sending more cows to auction.

Dairy export outlook: Weaker dollar boosting expectations

A weaker U.S. dollar and an improving global economy are boosting the outlook for agricultural exports, including dairy.

The value of the U.S. dollar has declined about 7 percent since January, and is down about 10 percent relative to the euro since the beginning of the year, according to USDA’s quarterly Outlook for U.S. Agricultural Trade, released Aug. 29. Although it remains strong relative to earlier this decade, the dollar’s value is expected to generally trend lower for the remainder of 2017.

The outlook for dairy exports was raised based on improved demand and stronger prices for most products. FY’17 (Oct. 1, 2016 through Sept. 30, 2017) dairy exports are expected to increase to $5.5 billion, about equal to FY’15 after falling below $4.6 billion in FY’16. U.S. dairy exports hit a record high of $7.4 billion in FY’14.

Meanwhile, the FY ’17 U.S. dairy import forecast was estimated at $3.3 billion, down slightly from FY’16. FY’17 cheese imports are projected at $1.2 billion, compared to $1.3 billion in FY’16.

The initial dairy export outlook for FY’18 (Oct. 1, 2017-Sept. 30, 2018) was forecast at $5.7 billion. Imports of dairy products are expected to drop to $3.2 billion, although cheese imports will increase slightly.

Total FY’17 U.S. agricultural exports are forecast at $139.8 billion, about $10.2 billion more than FY’16 exports. U.S. agricultural imports are forecast at $116.2 billion, up $3.2 billion. The U.S. agricultural trade surplus is forecast at $23.6 billion, up from $16.6 billion in FY’16. ![]()

-

Dave Natzke

- Editor

- Progressive Dairyman

- Email Dave Natzke