A panel of dairy economists shared the outlook they perceive for the global dairy market at the American Dairy Products Institute (ADPI) Annual Conference held last month in Chicago, Illinois.

European Union

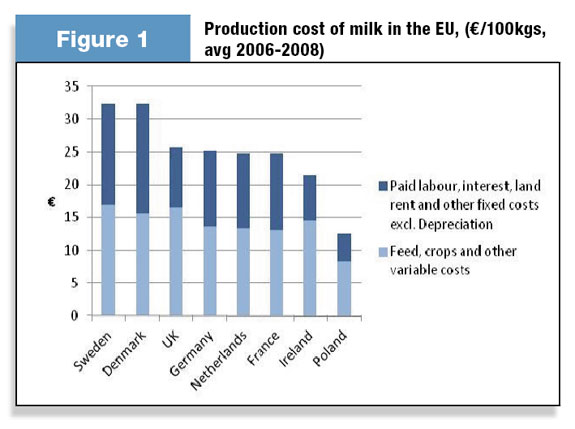

Calling in from New York, Mark Voorbergen with Rabobank International – Europe, recounted the year European Union farmers faced in 2009. Milk supply growth finished the year down 0.6 percent.

Farmers tried to squeeze every little bit out of their cows, he said. Fixed costs are relatively high, so in order to cover them when prices fell even farther below breakeven last March, they could only focus on what they do best – milking cows.

Milk production in Europe is largely insensitive to price changes because of the high fixed costs.

“I think that’s going to be a big challenge for milk prices going forward. As a bank we’re going to have to play a role in dealing with the ups and down of milk prices,” Voorbergen said.

In his short-term outlook, this market analyst reported that local demand is still slow to recover, but he’s starting to see some reactions on the buyer side. Export demand is picking up, especially to the Russian market. Another positive is that buyer stocks are still below the historic average.

However, there remains a significant stock of skim milk powder that needs to be cleared. Political pressure is building to move those stocks and Voorbergen said the EU’s 2010 production profile would likely favor cheese and whey, rather than the heightened butter and skim milk powder it produced last year.

Oceania

Historically, Australia and New Zealand were not subject to volatility in the dairy marketplace, states David McGowan from Fonterra. That changed in 2007 and they’ve experienced the highs and lows similar to the rest of the globe.

Uncertainly looms over the region’s ability to supply the global marketplace. Australia milk production is declining and future growth in New Zealand is limited. Forty percent of New Zealand’s herd is currently in a drought zone. Nearing the end of the milk season, production for the year is predicted to be 1.5 to 2 percent below expectations.

Compared to the large increase in product surplus in 2009 due to the export decline and financial crisis, McGowan said it’s expected to decrease this year.

The domestic market continues to deliver strong growth, as Australia emerged from the global financial crisis unscathed.

They have also seen China demand increase substantially in a fairly rapid period and are not seeing any slowdown there at the moment. “Clearly they do have an industry and could stimulate milk production on their own; however, there has been a large reduction in animal numbers and its capability to increase production in the short term is fairly limited,” he said.

“In the absence of intervening policy, international, EU and U.S. dairy commodity prices will move close in parity,” McGowan said. “As support programs are reduced or removed, a true market price will be established, but supply and demand swings will create greater price volatility.”

To manage the volatility, Fonterra developed a commodity risk and trading group and is working to provide a range of tools to manage risk for both buyers and sellers. Some of the tools include long-term contracts with built-in risk premiums, swaps or contracts for difference, options and contracts that include optionality, and identifying opportunities where derivative markets can be used to structure fixed price sales.

McGowan said he is excited to see the range of developments occurring in dairy derivatives. Now, he added, “It’s important that we support the development of a transparent marketplace.”

U.S. supply

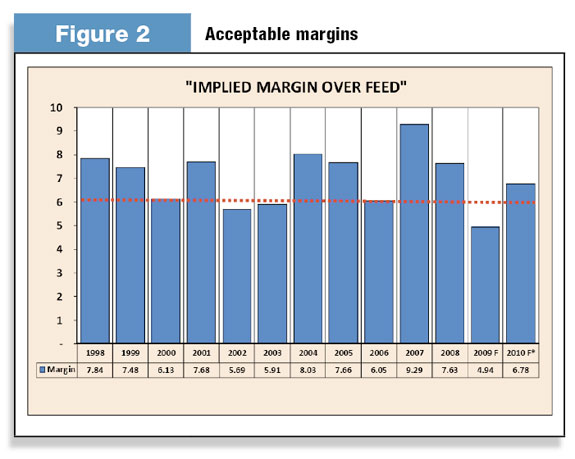

Phil Plourd and his colleagues at Blimling and Associates have done a fair amount of work trying to come up with a way to forecast milk production in the U.S. By flipping around the milk-feed ration, they’ve developed what they call the “implied margin over feed.”

They also identified that 6.2 is the line between expansion and contraction. When the margin is greater than 6.2, the industry expands; and when it is lower, the industry contracts.

Using futures prices for Class III milk and grain and an estimated hay price, Plourd forecasted a margin of 6.78 for 2010, signaling a mild expansion in milk production for the year.

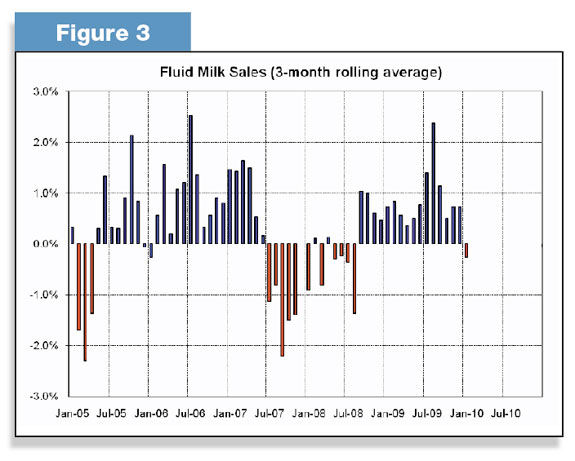

Based on numbers run by Blimling and Associates, Plourd reported that cow numbers are basically flat. When slaughter numbers are 55,000 or less, the industry starts expanding; and when they are 60,000 or more, shrinking occurs.

“We’ve been floating in between there since the beginning of the year. I don’t foresee a big change this year,” he said.

When looking at animal inventories, he related the worst-kept secret in the industry is the growing heifer inventory. The heifer-to-cow ratio is 49.7 percent, well above any historic levels. “The expectation for 2010 is that we’re going to have a lot of young animals in the pipeline. To get the number of cows back on a downward trend, we’re going to have to kill a lot more animals,” Plourd said.

Current economics support more rather than less production in the near future. Bankers have become somewhat of a mystery, he said. They’ve come too far to pull the plug now. Also, assets – in the form of heifers and empty freestalls – are plentiful and ready to be deployed if prices dictate. It will not take Greenfield development to grow the first 1 to 2 percent.

“Our forecast shows 0.9 percent growth for 2010,” he said, adding the country probably needs this additional production to meet demand that wasn’t there four to six months ago.

Speaking to how farm prices should be set moving forward, Plourd said there is tension in that debate. “Either you try to fix the system to take it industry-wide or you take the system out to allow producers and companies the ability to manage it on their own.”

U.S. demand

Mike McCully from Kraft Foods shared what will be done with all the milk produced in the U.S.

Retail cheese sales have posted huge numbers and gains since early in 2009 as people ate more from home. Those sales are down a bit now, but still good. He mentioned Kraft, as a branded company, is concerned with the strong, growing trend in private label sales and whether or not consumers will shift back to brand names as the economy improves.

Cheese is becoming less and less of a product developed to balance the milk supply. It’s now something that has its own demand. Into the future, he doesn’t see milk shifting from cheese plants just to make butter and powder. “We’re probably shorter on those products relative to cheese,” McCully said.

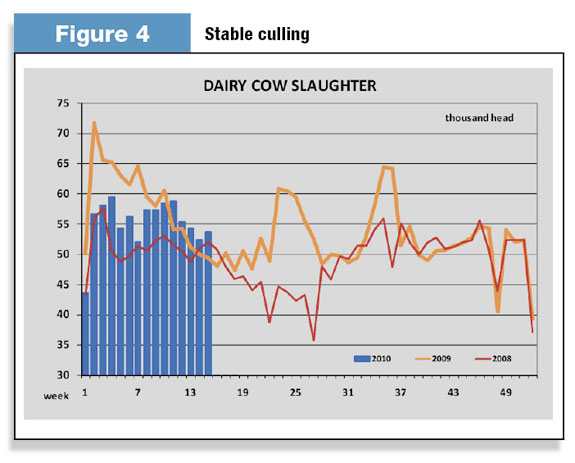

Fluid milk sales have maintained their sensitivity to price. The sales posted big negatives in 2007 and 2008 when prices were high, which was followed by a run in positive sales the last 18 months while prices were negative. Now, they are starting to slip back down again.

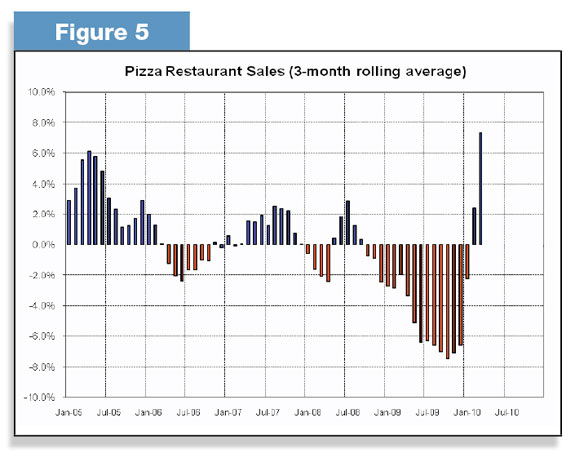

Restaurant sales dropped sharply due to the recession, but some improvement is being seen now except in the really high-end places. “If the economy continues to gradually improve, people will start to eat out more,” McCully said.

“The economy going forward is going to be different,” McCully said, “not just in the U.S., but globally.”

For other countries, volatility in the marketplace is just starting. The U.S. has dealt with it for some time and has already developed a lot of tools to manage the risk. Yet, now it may be important to take those tools to a larger market.

“Development of viable futures contracts will greatly enhance global price discovery and transparency, providing a method for the industry to manage price volatility,” McCully said. PD

-

Karen Lee

- Midwest Editor

- Progressive Dairyman

- Email Karen Lee