The federally inspected slaughter for June was strong, exceeding the three previous years. More heifers and cows were in the slaughter mix in June, causing the average carcass weight to drop below the previous month’s expectations.

Based on USDA Agricultural Marketing Service (AMS) data on actual and estimated daily cattle slaughter, the percentage of heifer slaughter compared to that of steers for June 2021 was estimated at 2.5 percentage points higher than a year ago. The estimated percentage of federally inspected cow slaughter to total slaughter for June 2021 was 0.5% higher than June 2020.

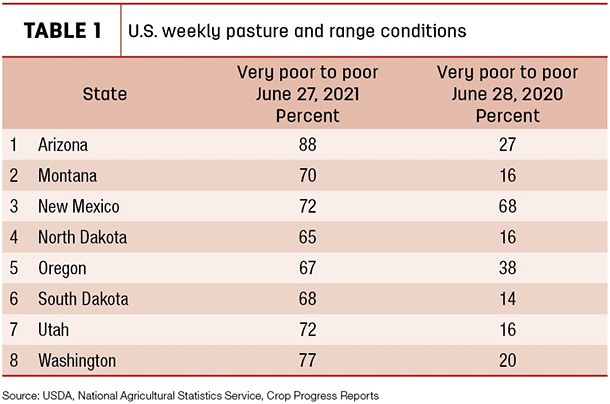

The forecast for 2021 beef production was unchanged from the previous month, as higher expected cow slaughter will likely be offset by lower average carcass weights. According to the U.S. Drought Monitor data, approximately 34% of cattle are in regions experiencing some level of drought. Pasture and range in much of the western and northern U.S. continue to be in very poor to poor conditions (see Table 1), which is likely affecting cow slaughter in regions where forage availability has become critical.

However, to the extent that the increase in aggregate slaughter numbers is driven by higher expected cow numbers and that heifers have recently been a higher proportion of steer and heifer slaughter, average carcass weights are expected to be lower.

With higher expected cow slaughter in the coming months, slaughter in later months is expected to decline as cows that might have been slaughtered in the fall move into the slaughter chain sooner. The 2022 forecast was reduced 10 million pounds from the previous month to 27.325 billion pounds, reflecting slightly lower cow slaughter after higher-than-expected cow slaughter in 2021. The USDA will be releasing its Cattle report on July 23, which will provide an estimate of the midyear cattle inventory and producer intentions for retaining heifers for breeding.

Cattle prices are forecast higher in the second half of 2021 and in 2022

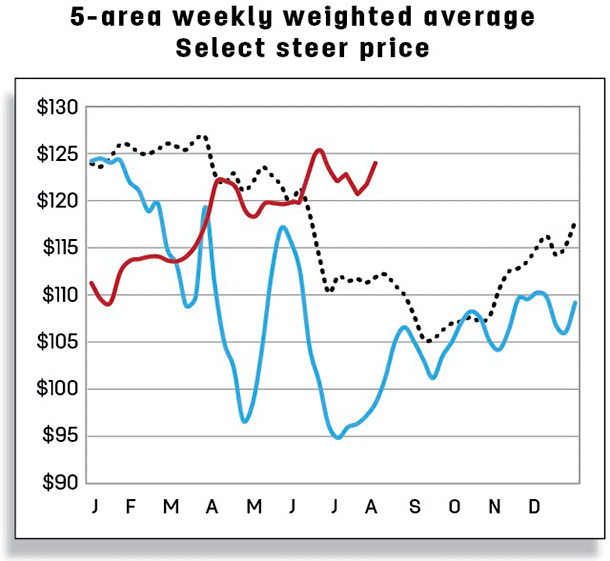

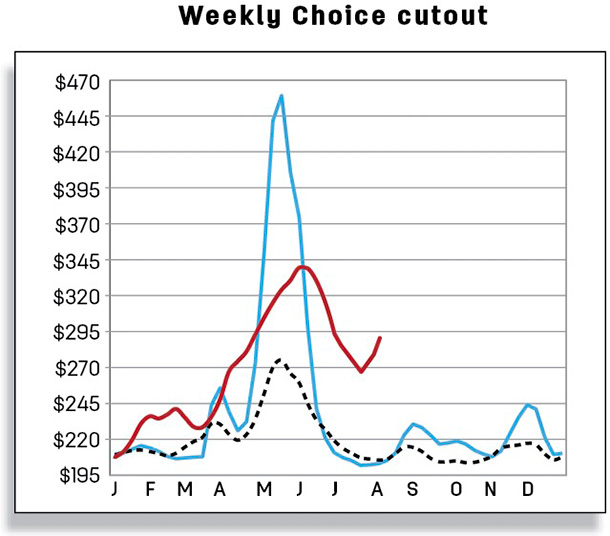

The June 5-area price for fed steers was $122.02 per hundredweight (cwt), up more than $18 year-over-year and almost $10 higher than the June 2019 average price. For the week ending July 4, the price for fed steers in the 5-area marketing region was $123.89. Although the Choice cutout has been declining since early June, it is still well above typical levels for this time of year. Fed steer prices are trending upward, implying that packers are willing to pay higher prices to bid cattle out of the feedlots. The forecast for third- and fourth-quarter fed steer prices was raised $5 to $120 per cwt and $3 to $123, respectively. The 2021 annual price forecast for fed steers was increased $2.20 to $119.20 per cwt from the previous month. Fed steer prices are forecast to continue trending upward in first-quarter 2022, reaching $127 per cwt, up $2 from the previous month. The 2022 annual price forecast for fed steers is unchanged from the previous month at a rounded $122 per cwt.

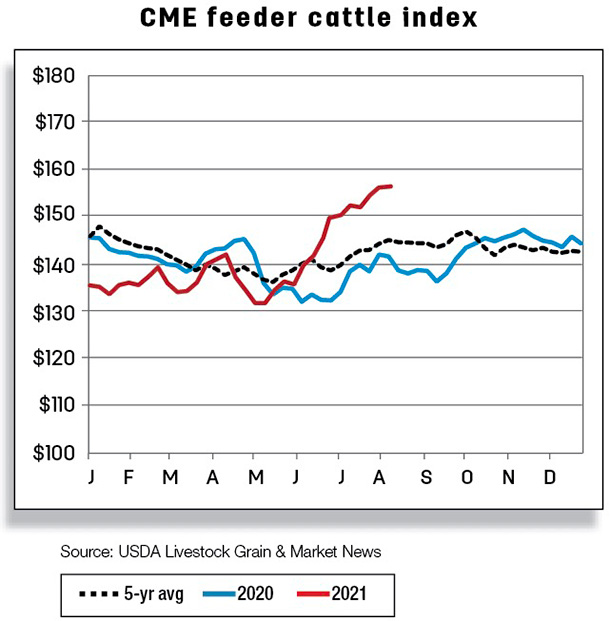

For June 2021, at the Oklahoma City National Stockyards feeder steers weighing 750 to 800 pounds averaged $144.09 per cwt, 10% above a year ago and 6% higher than the June 2019 price. The outlying quarters were raised on current price strength by $5 in the third and fourth quarters to $146 and $148 per cwt, respectively. The annual price forecast was raised to $142.10 per cwt. The current price strength is expected to carry over into 2022, with the first quarter increased $5 to $144 per cwt and the annual forecast raised to $147 per cwt.

Beef imports relatively flat in May; 2021 import forecast unchanged

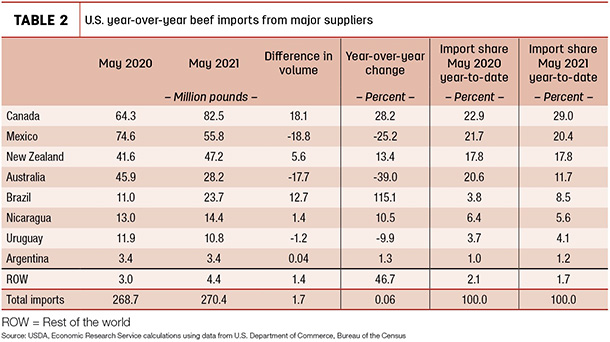

Beef imports in May totaled 270 million pounds, up almost 1% or 1.7 million pounds, from a year earlier (Table 2).

Strong beef shipments from Canada and Brazil were noteworthy for May. Shipments from Canada, the U.S.’s top beef supplier on a monthly basis since February 2020 and on an annual basis since 2017, were the largest in volume since June 2010. Year-over-year, imports from Canada were more than 18 million pounds higher in May. Imports from Brazil were also up in May compared to a year ago. In May, imports from Brazil were the second highest, largely to help fill U.S. demand for 90% lean beef trimmings not imported from Australia. Other beef suppliers, including New Zealand, Nicaragua and Argentina, also contributed toward May’s year-over-year increase.

In volume, Mexico shipped almost 19 million pounds less in May than a year ago. Australia’s cattle story continues: Signs of herd rebuilding remain a focal point of the Australian beef industry as cows and heifers are retained for breeding. U.S. imports from Australia were down 39% year-over-year.

However, among the major sources of imports, gains from Brazil, Canada and New Zealand more than offset substantial declines in imports from Australia and Mexico.

The annual forecasts for 2021 and 2022 beef imports remain unchanged from the previous month at 3.021 billion and 2.990 billion pounds.

Beef exports up in May on robust shipments to Japan, South Korea and China; 2021 and 2022 forecasts raised

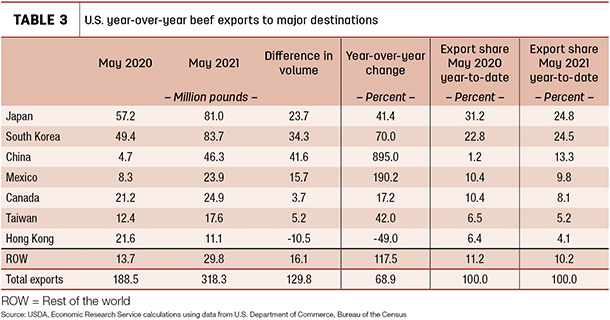

In May, U.S. beef exports soared to a record volume totaling 318 million pounds, an increase of 69% or 130 million pounds from a year earlier (Table 3).

While U.S. beef exports were up in six of the seven major destinations, May’s year-over-year increase was driven primarily by abnormally low exports due to the impact of COVID-19. However, the third consecutive month of record volumes is, to a large extent, the result of large shipments to South Korea, Japan and China.

South Korea received its largest volume of beef yet from the U.S., exceeding the record 75.1 million pounds posted in August 2020 by 8.6 million pounds. Since January, U.S. beef exports to South Korea have been up due to strong demand and a lower tariff rate than a year earlier. The second-largest shipment in May went to Japan. The increase in U.S. beef exports to Japan has also been partially driven by a lower tariff rate than a year ago.

For exports to China, the story of year-over-year increases continues. China is the U.S.’s third-largest beef destination and imports have been up substantially, partly due to the change in U.S. access to China’s market that was established in March 2020 along with the strength of import demand for animal proteins to help offset China’s low domestic supplies of pork. U.S. producers have increased production of cattle geared toward meeting China’s import requirements, which has supported higher beef shipments.

There were other noteworthy key trading partners contributing to the increase in beef exports in May. Beef shipments to Canada and Taiwan rose in May from a year earlier; U.S. beef exports to Canada were up 3.7 million pounds from a year ago, and exports to Taiwan were up 5.2 million pounds. However, although shipments to Mexico have been up year-over-year, the volume of beef exported in 2021 to Mexico has been lower than in 2019. Lower volumes of beef exports to Mexico in 2020 were partially due to economic weakness and trade disruptions due to COVID-19.

The second-quarter forecast for beef exports was raised by 30 million pounds from the previous month to 890 million pounds, partly due to the stronger demand from China, South Korea and Japan in May. U.S. beef export forecasts for the third and fourth quarters were also elevated, by 40 million to 900 million pounds and 10 million to 835 million pounds, respectively, on continued robust demand in Asia. The annual forecast for 2021 was raised to 3.422 billion pounds. This demand strength is expected to carry over into 2022, increasing the annual forecast to 3.320 billion pounds.