Administrators of the 11 Federal Milk Marketing Orders (FMMOs – see Figure 1) reported February 2022 uniform milk prices, producer price differentials (PPDs) and milk pooling data, March 9-12. Here’s Progressive Dairy’s monthly review of the numbers and their potential impact on your milk check.

Class prices continue to rise

FMMO statistically uniform milk prices were up in February, while the spread between Class III-IV milk prices again impacted handler pooling.

Supporting higher uniform prices, prices for all individual classes of milk were up from January:

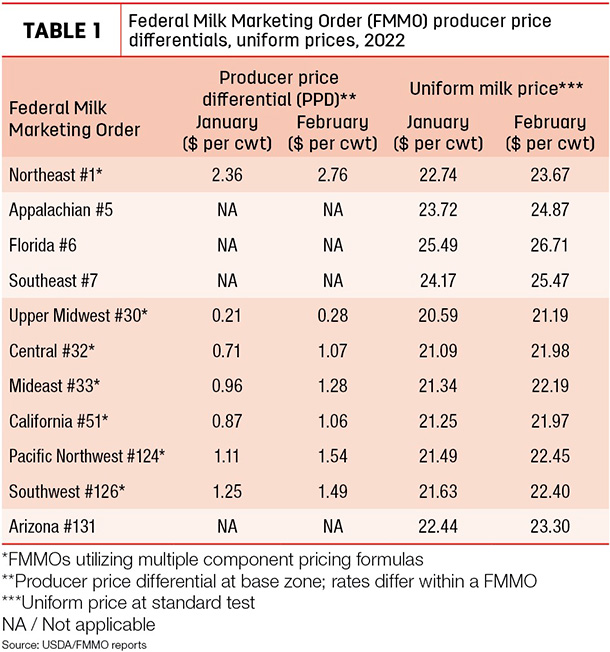

- At $21.64 per hundredweight (cwt), the advanced February Class I base price moved to an 86-month high, up $1.93 from January 2022 and $6.10 more than February 2021. Adding Class I differentials, the February Class I price averaged $24.46 per cwt, with a high of $27.04 per cwt in the Florida FMMO and a low of $23.44 per cwt in the Upper Midwest FMMO.

After a seven-month reprieve, the debate over the “higher-of” versus “average-of plus 74 cents” formula resurfaced in February. The difference between the advanced Class III skim milk pricing factor ($10.43 per cwt) and the advanced Class IV skim milk pricing factor ($12.97 per cwt) was $2.54 per cwt. When adding the advanced butterfat pricing factor, producers received 51 cents less under the average-of plus 74 cents Class I mover compared to the old higher-of formula. That difference was diminished in producer milk checks, however, depending on Class I utilization in each FMMO and its impact on “blend” or uniform milk prices.

- February’s Class II milk price was $23.79 per cwt, up 96 cents from January and up $9.79 from February 2021.

- The February 2022 Class III milk price rose 53 cents from January to $20.91 per cwt, the highest since November 2020, when government purchases of cheese for food boxes pushed prices up. The Class III price was up $5.16 from February 2021.

- The Class IV milk price soared to a record high $24 per cwt in February. It’s up 91 cents from January and $10.81 higher than February 2021.

Component values, tests

February Class III-IV milk prices again moved higher due to increases in values of butterfat and milk solids used in monthly milk price calculations, but the value of protein was down slightly.

The value of butterfat rose about 6.5 cents from January to $3.02 per pound. The value of milk protein slipped about 4 cents from January to about $2.32 per pound. The value of nonfat solids rose about 4 cents to $1.55 per pound, while the value of other solids increased about 7 cents to 59.8 cents per pound.

In FMMOs reporting component tests for pooled milk, average butterfat and protein tests were down slightly from January.

Uniform prices higher

With higher individual milk class prices, February blend or uniform prices at standardized test rose in all FMMOs (Table 1) and were the highest since the final months of 2014. When multiplied by milk class utilization in each FMMO, February uniform prices increased in a range of 60 cents to $1.30 per cwt across all 11 FMMOs compared to January. The high uniform price for February was $26.71 per cwt in Florida FMMO #6; the low was $21.19 per cwt in the Upper Midwest FMMO.

February baseline PPDs were positive and slightly higher than January, ranging between 7-43 cents more than January (Table 1).

As we remind you each month, PPDs have zone differentials within each FMMO. Also, whether positive or negative, individual milk handlers apply PPDs and other deductions to milk checks differently.

Impact on pooling

You can get a general picture of FMMO pooling-depooling in a couple of ways: on a volume basis, comparing monthly pooling totals to previous months, and on a percentage basis, comparing the percent utilization of a specific class of milk relative to all milk pooled that month.

Looking at February data, about 11.69 billion pounds of milk were pooled on federal orders, down about 960 million pounds from January. Factoring into that decline, of course, is the shorter month.

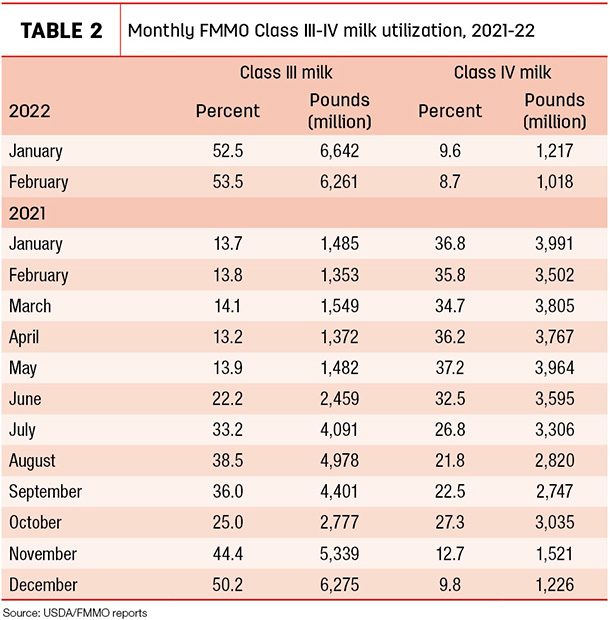

February’s Class III-IV price relationship created a wide $3.09-per-cwt spread, providing incentives for Class IV depooling. Class IV milk pooled across all FMMOs fell to about 1.018 billion pounds (Table 2), the lowest volume since pre-2018. February Class IV milk utilization represented about 8.7% of total FMMO milk marketings, also a pre-2018 low.

February’s Class III-IV milk relationship again had an opposite impact on Class III pooling. With the Class III milk price below than Class IV price, Class III handlers brought more milk back to the pool. On a volume basis, Class III milk pooled in February was estimated at about 6.261 billion pounds, more than four times the average monthly volume pooled during the first five months of 2021. As a percentage of utilization, Class III milk represented about 53.5% of the total FMMO pool, also the highest since the first quarter of 2019.

Looking ahead

Class and uniform prices will move higher for March milk marketings, but incentives for Class IV milk depooling will remain.

The March 2022 advanced Class I base price moves to eight-year high. At $22.88 per cwt, it’s up $1.24 from February 2022 and $7.68 more than March 2021. It’s also the highest since November 2014. Adding Class I differentials to each order's principal pricing point, the March 2022 Class I price averages $25.70 per cwt, with a high of $28.28 per cwt in the Florida FMMO and a low of $24.68 per cwt in the Upper Midwest FMMO.

The Class I mover formula again comes into play. At $3.12 per cwt, the difference between the advanced Class III skim milk pricing factor ($10.59 per cwt) and the advanced Class IV skim milk pricing factor ($13.71 per cwt) grew substantially. Based on Progressive Dairy calculations, the Class I mover calculated under the higher-of formula would have resulted in a Class I base price of $23.67 per cwt, 79 cents more than the price determined using the average-of plus 74 cents formula.

March Class II, III and IV milk prices will be announced on March 31. At the close of Chicago Mercantile Exchange (CME) trading on March 11, the March Class III futures price was $22.35 per cwt, up $1.44 from February. The March Class IV futures prices settled at $24.80 per cwt, up another 80 cents per cwt from February. If those prices hold, the Class III-IV price spread would be about $2.45 per cwt.

Longer term, as of March 11, Class III futures prices averaged $22.90 per cwt for all of 2022, with Class IV futures averaging $24.40 per cwt. The spread between the Class III-IV futures prices averages about $1.50 for the year, maintaining Class IV depooling incentives.

Individual FMMO pooling, depooling and repooling rules play a role in how much. And milk markets change.

Another look back

Updating previous months, two monthly average milk prices announced by the USDA both improved for November 2021 milk marketings. And with FMMOs reporting PPDs that month, the spread between the average “all-milk” and “mailbox” prices shrunk.

Based on Progressive Dairy calculations, November 2021 mailbox prices were 81 cents per cwt less than the all-milk prices for comparable states and regions. That was the smallest difference since May 2020, when the COVID-19 pandemic disrupted milk markets and FMMO class pricing.

The all-milk price is the estimated gross milk price received by dairy producers and includes quality, quantity and other premiums but does not include marketing costs and other deductions.

The mailbox price is the estimated net price received by producers for milk, including all payments received for milk sold and deducting costs associated with marketing.

The price announcements reflect similar – but not exactly the same – geographic areas. The USDA National Ag Statistics Service (NASS) reports monthly average all-milk prices for the 24 major dairy states. The mailbox prices are reported by the USDA’s Agricultural Marketing Service (AMS) and covers selected FMMO marketing areas. The AMS announcement of mailbox prices generally lag all-milk prices by a couple of months.

The November 2021 Class III-IV spread, with Class IV milk price moving above the Class III price, provided incentives for Class IV depooling in November.

Through the first 11 months of 2021, the USDA’s mailbox prices averaged about $1.05 per cwt less than average all-milk prices for the same months. During that period, all-milk prices averaged $18.41 per cwt, while mailbox prices averaged $17.36 per cwt.

The difference in the two announced prices can affect dairy risk management, since indemnity payments under the Dairy Margin Coverage (DMC), Dairy Revenue Protection (Dairy-RP) and Livestock Gross Margin for Dairy (LGM-Dairy) programs are all based on the all-milk price, before any marketing cost deductions.