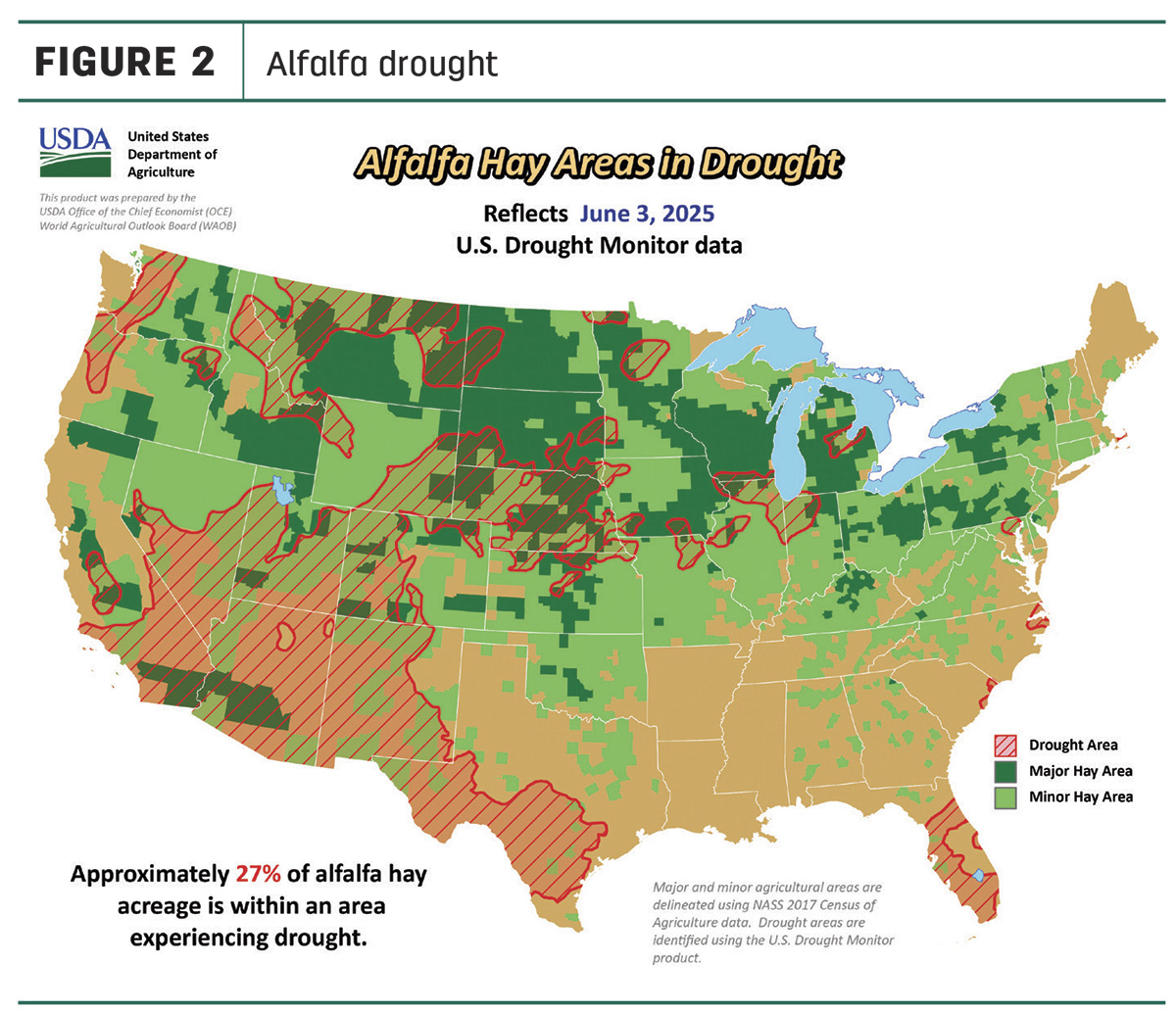

The forage market continues to be influenced by several key factors including drought conditions, fluctuating hay prices and continuing trade policies. During the first week of June, it was reported that about 19% of U.S. hay-producing acreage is under drought conditions, showing a notable improvement from April, which was 39%. For alfalfa hay, the percentage is slightly higher at 27%. The reduction in drought conditions is expected to improve forage availability and stabilize hay prices, but regional variations will still play a role.

Here’s a review of what we do know about hay and forage markets as you continue to look for answers.

U.S. Drought Monitor maps indicate shifting weather patterns across the country from late May through early June. Heavy precipitation occurred in the Desert Southwest, where a low-pressure system combined with moisture from Tropical Storm Alvin, the first named storm of the year in the Northern Hemisphere, to bring heavy rainfall to Arizona, improving drought conditions. The Northeast also saw significant relief with May precipitation exceeding 200% of normal precipitation, effectively ending drought in most areas.

Cooler-than-normal temperatures were observed across the Central Plains, eastern Corn Belt and Mid-Atlantic states and into the Carolinas and northern Georgia.

As of June 3, approximately 19% of U.S. hay-producing acreage (Figure 1) was considered under drought conditions, down 7% from a month earlier. The estimate of alfalfa hay-producing acreage (Figure 2) under drought conditions declined slightly to 27%, down 8% from a month earlier.

Drought conditions continued shifting across key agricultural regions. While the Great Plains saw expanding drought, southern Iowa, northern Illinois and northern Missouri also experienced an increase in drought conditions due to little to no precipitation.

A snapshot of hay prices

USDA price data for 27 major hay-producing states is mapped in Figure 3, illustrating the most recent monthly average price and one-month change. The lag in USDA price reports and price averaging across several quality grades of hay may not always capture current markets, so check individual market reports elsewhere in Progressive Forage.

Dairy hay

The top milk-producing states reported an average price of $252 per ton for Premium and Supreme alfalfa hay in April 2025, a $10 increase from March 2025 (Table 1). The average price was $12 lower than April 2024.

Alfalfa

The U.S. average price for all alfalfa hay increased $13 in April to $180 per ton. Compared to a month earlier, prices were lower in 17 of 27 major forage states, with the largest declines in Montana, Oregon, Wyoming, Oklahoma, Texas, Arizona, Ohio, Washington and Wisconsin. Prices were up in six states including Pennsylvania, New York, Idaho, Minnesota, Nevada and Kansas.

With few exceptions, year-over-year alfalfa hay prices were down substantially, with the U.S. average down $5 compared to April 2024.

Other hay

At $138 per ton, the April 2025 U.S. average price for other hay was down $1 from March. Prices rose in just 12 of 27 major hay-producing states, with the largest month-to-month increase in Arizona, Idaho, Iowa, Minnesota, Nevada, New Mexico, Oklahoma, Texas, Washington, Wisconsin and Wyoming. Declines were recorded in seven states: Colorado, Illinois, Kansas, Montana, North Dakota, Ohio and Utah.

Expanding the timeline, the April 2025 U.S. average price for other hay was $18 less than a year earlier, with declines of $50 or more in Colorado, Iowa, Kansas, Nebraska, New Mexico, Texas and Wisconsin. In contrast, prices increased in Arizona, Kentucky, Michigan, Nevada, New York and Pennsylvania.

The gap between average U.S. alfalfa and other hay prices was about $42 per ton in April.

Exports

At deadline, the U.S. saw notable shifts in its hay export market. This snapshot offers valuable insight into the nature of U.S. hay exports and its key global markets.

At 141,441 metric tons (MT), April exports of alfalfa hay decreased. China remained the top buyer, importing 50,397 MT during the month, about 35% of the total. April shipments to Japan decreased at 29,635 MT, 20% of the total for April.

Exports of other hay also decreased, to 81,673 MT in April. As usual, Japan and South Korea led buyers in the other hay category; Japan purchased 45,118 MT during the month, followed by South Korea’s 21,602 MT.

U.S. exports of most categories of alfalfa cubes and meal were lower in April, totaling about 7,318 MT. Japan imported about 85% of the total.

Regional markets

Regional hay sales and USDA Ag Marketing Service market reports have been moderate to good with steady demand, while export hay demand remains light.

- Midwest: In Iowa, markets are showing moderated trade activity, with steady hay demand. Compared to last month, offerings have increased slightly, but demand remains selective, particularly for Premium and Supreme grades.

In Kansas, demand was light, trade was moderate and prices were steady. Storms continued to cover most of the state, making it almost impossible to get into the fields, which made hay movement slow in many regions. There was some movement of new-crop alfalfa and continued movement of old-crop and grass hay.

In Illinois, comparable hays in small squares sold $1 to $3 higher. Trade was active with good demand with a small crowd.

In Missouri, some of the best pastures in the nation with 87% rated as good to excellent. Hay harvest for alfalfa and other types of hay is running slightly ahead of the five-year average. Still has not been a lot of new-crop hay sold with asking prices mostly steady; supply is moderate and demand is light to moderate.

In Nebraska, bales of alfalfa and grass hay sold steady. Demand was moderate at best as rain showers have moved through. Some reports on first-cutting alfalfa in the east, roughly 30% less than normal years' tonnage due to dry weather and weevils.

In South Dakota, few reported sales, steady undertones. Moderate demand for old-crop hay. First cutting of alfalfa was difficult between the rains and the cooler weather. There is still old-crop hay as the winter was mild and open.

- East: In Alabama, hay prices are steady, trade moderate with moderate supply and demand. Due to good rainfall in the past few weeks, many producers have already cut hay or will cut hay, weather permitting.

In Tennessee, no confirmed trades are recorded this month. Current hay stocks were noted to be lower, with some cooperators being sold out of current stock until new hay can be harvested. Wet conditions throughout have made cutting and drying hay difficult, with only small windows of opportunity available.

In Pennsylvania, showing steady trade activity with strong alfalfa sales on limited comparisons and consistent pricing for alfalfa/grass mixes.

- Southwest: In California, trade activity and demand were moderate to good. Retail hay demand was good. Dairy hay demand was steady. Export hay demand was light.

In Oklahoma, prices for new hay are still unknown, and demand is at a standstill. Rain continuously covers Oklahoma, preventing hay producers from moving hay and, at times, stopping hay from being harvested. The continued preparation for the new crop of grass hay is underway.

In Texas, hay prices are mostly steady across all regions with moderate to light demand.

- Northwest: In Montana, hay sold generally steady. Very little hay is moving, as most are waiting on first cutting. Ranchers are already reaching out to producers to purchase hay, with some making offerings to buy. Offers have been well received, but many are passing as they wait for the market to develop. Market activity was mostly slow.

In Utah, hay cubes sold steady with steady demand and movement. Demand for hay is slow with buyers waiting for new crop. New sales are expected in the next couple of weeks after the new crop is stacked and ready to go.

In Idaho, movement has increased with sales of new crop starting. Demand for hay is moderate but better than it has been. New crop is starting to get cut.

In the Washington-Oregon Columbia Basin, all grades of hay are steady. Trade remains slow with light to moderate demand. Timothy and orchardgrass are being put in the bale and stacked.

In Oregon, movement is about steady. The demand for new-crop and old-crop hay is slow. New crop is getting cut and raked in eastern Oregon and parts of Klamath Basin; it has been quiet with buyers not making any offers on new crop.

In Wyoming, movement is about steady; demand for hay has been slow. Most of the hay sold was in small loads. The demand for cubes has decreased slightly with grass greening up, and the demand for pellets remains steady.

In Colorado, trade activity and demand are light. No market trend is available due to a lack of comparable trades. Farmers are waiting for hay stands to dry so they can cut first cutting, with higher-elevation hay stands two to three weeks out.

Other things we’re seeing

- Dairy: April U.S. milk production increased from March and is up about 1.5% from the USDA’s estimates a year earlier. Eighteen states boosted production a combined 387 million pounds; six states reduced production a combined 91 million pounds. Year-over-year growth leaders were Texas (up 145 million pounds), Idaho (up 59 million pounds) and Kansas (up 39 million pounds).

- Cattle: The outlook for beef production in 2026 is forecast at 25.14 billion pounds, a 5% decline from 2025. It would mark the fourth consecutive year of lower production following the record volume set in 2022. A smaller expected calf crop in 2025, more heifers retained for breeding and fewer live cattle imports will contribute to fewer calves placed in feedlots in late 2025 and early 2026. Fewer placements during this period will limit marketings for slaughter in 2026.

- Fuel: National average fuel prices were slightly lower to start April, according to the U.S. Energy Information Administration (EIA). The U.S. retail price for regular-grade gasoline averaged $3.11 per gallon on June 9, down 1.9 cents from the previous week and 32 cents less than the same week a year earlier. The average U.S. on-highway price of diesel was $3.47 per gallon, up 2 cents from the prior week and 18 cents less than early June 2024.

- Trucking: Spot flatbed prices were mostly higher to start June, down in the Southeast and Northeast but higher elsewhere and averaging $2.55 per mile nationally, according to DAT Trendlines. Regionally, average spot prices per mile were: Southeast – $2.78, Midwest – $2.61, South – $2.71, Northeast – $2.41 and West – $2.23.

- Other costs: The USDA’s May prices paid index for commodities and services, interest, taxes and farm wage rates is up 0.4% from May 2025 and 5.1% from May 2024. Machinery costs were unchanged from May but were up 0.9% from May 2024. Compared to a month earlier, fertilizer prices were up 1.3% from May and 2.8% from May 2024. Prices are higher for potash and phosphate, nitrogen and mixed fertilizer.

- Total May feed prices remained relatively stable, with minor fluctuations across different categories.

- Interest rates: USDA Farm Service Agency (FSA) interest rates for farm operating loans (5%) and direct ownership loans (5.75%) were higher for June.