Due to the ongoing federal government shutdown, some USDA and federal data sources may be delayed or temporarily unavailable. This report draws on state extension services, private market analysts and industry observations to provide current forage market insights.

As of October 2025, U.S. hay markets remain regionally mixed, with improving moisture conditions in some areas and continued drought in others. Alfalfa prices are generally down, while grass hay prices show wide variability.

Here’s a review of what we do know about hay and forage markets as you continue to look for answers.

Drought conditions remain volatile across the U.S. Midwest and Northeast, where soil moisture continues to decline and fire risk increases. Missouri, Illinois, Indiana and Ohio face intensifying short-term drought, while New England sees expanding dryness.

In contrast, parts of the West – like Nevada, Utah and Oregon – are seeing improvement thanks to recent rainfall. The Southeast is mixed: Alabama and Georgia are drying out, but southeast Louisiana saw dramatic relief.

Forage producers face a narrowing window. Late-season growth may stall, and harvest quality could suffer where moisture remains elusive.

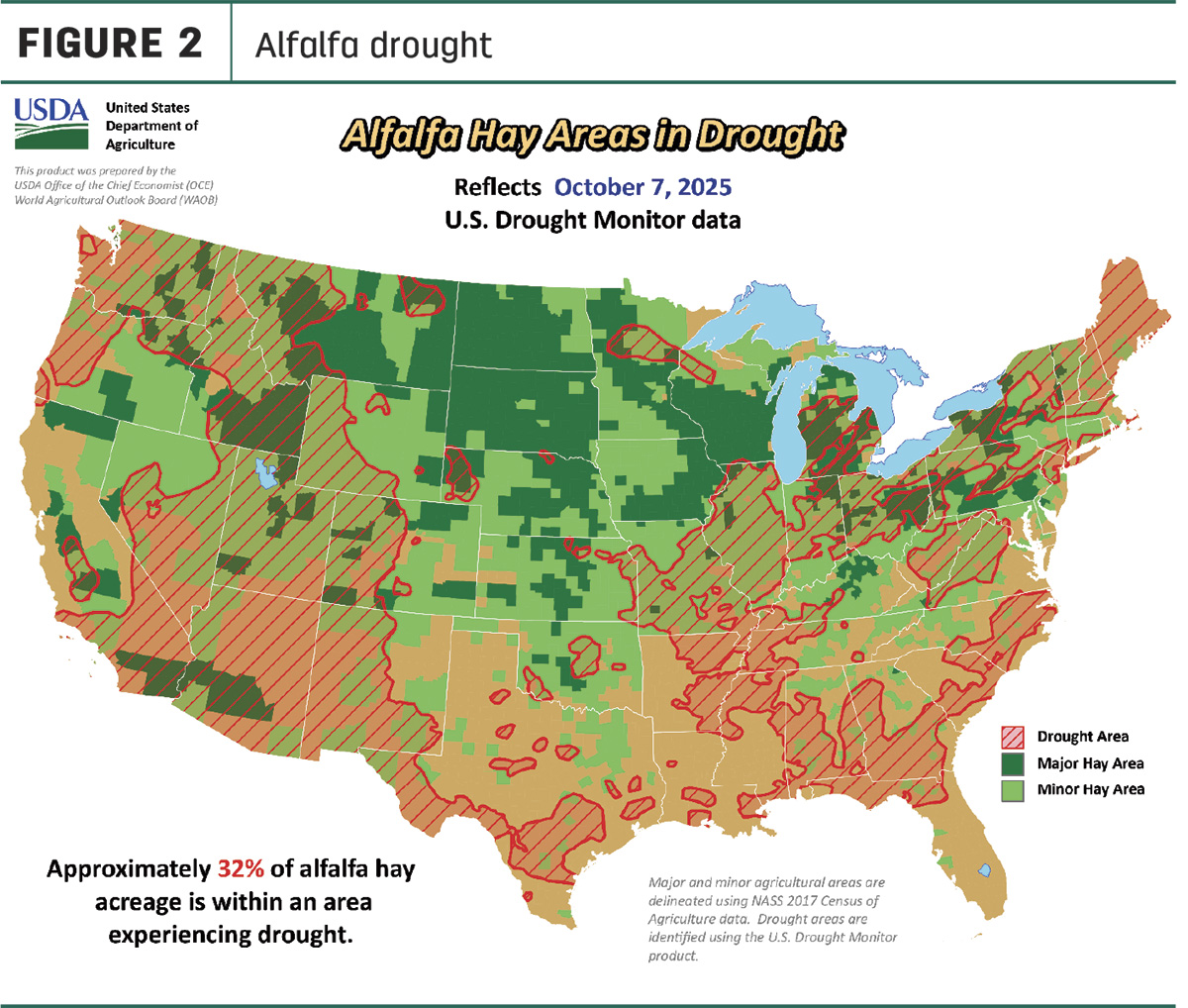

As of Oct. 7, approximately 33% of U.S. hay-producing acreage (Figure 1) was considered under drought conditions, an increase of 9% from a month earlier. The estimate of alfalfa hay-producing acreage (Figure 2) under drought conditions increased slightly to 32%, up 5% from a month earlier.

A snapshot of hay prices

USDA price data for 27 major hay-producing states is mapped in Figure 3, illustrating the most recent monthly average price and one-month change. The lag in USDA price reports and price averaging across several quality grades of hay may not always capture current markets, so check individual market reports elsewhere in Progressive Forage.

Dairy hay

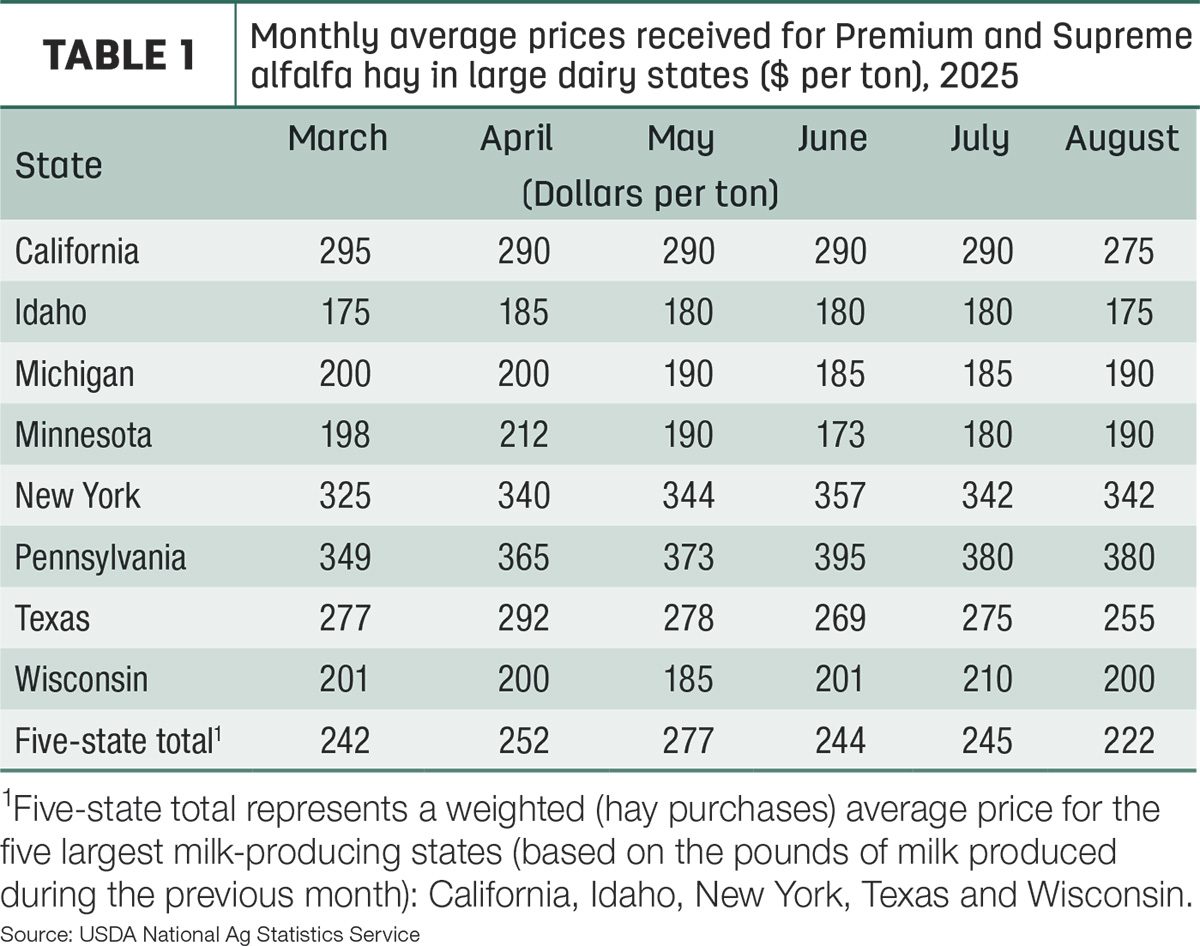

The top milk-producing states reported an average price of $222 per ton for Premium and Supreme alfalfa hay in August 2025, a $22 decrease from July 2025 (Table 1). The average price was $14 lower than May 2024.

Alfalfa

The U.S. average price for all alfalfa hay decreased $7 in August to $166 per ton. Compared to a month earlier, prices were lower in 12 of 27 major forage states, with the largest declines in Arizona, California, Colorado, Missouri, New York, North Dakota, Ohio, Pennsylvania, South Dakota, Texas, Wisconsin and Wyoming. Prices were up in 10 states including Iowa, Kansas, Kentucky, Michigan, Minnesota, Montana, Nevada, Oklahoma, Oregon and Utah.

With few exceptions, year-over-year alfalfa hay prices were down substantially, with the U.S. average down $9 compared to August 2024.

Other hay

At $138 per ton, the August 2025 U.S. average price for other hay was down $6 from July. Prices decreased in 10 of 27 major hay-producing states, with the largest month-to-month decrease in Arizona, Missouri, Montana, Nevada, New York, Oklahoma, Pennsylvania, Texas, Washington and Wisconsin. Increases were recorded in eight states, Idaho, Iowa, Michigan, Nebraska, New Mexico, North Dakota, South Dakota and Utah.

Expanding the timeline, the August 2025 U.S. average price for other hay was $12 less than a year earlier.

The gap between average U.S. alfalfa and other hay prices was about $28 per ton in August.

Exports

As federal reporting paused, private sources stepped in to highlight September’s hay export landscape. Total shipments dipped slightly, with alfalfa exports falling to 111,380 metric tons – a notable drop from August’s rebound. China remained the top buyer, though its volume softened to 54,592 metric tons (MT), suggesting a recalibration in feed demand or inventory. Japan held steady with 25,040 MT, reinforcing its role as a reliable trade partner.

Other hay exports hovered near August levels at 75,015 MT. Japan again led the category, importing 42,218 MT, followed by South Korea and Taiwan. These consistent patterns reflect stable demand for grass hay across East Asia, even as global buyers remain cautious amid tariff questions and weather-related quality concerns.

Regional markets

Hay trade remains slow, with light to moderate demand and minimal export movement. Many exporters are cautious, focusing on domestic sales. Weather disruptions – especially storms and wildfire smoke – have lowered hay quality in several regions. Prices vary widely by grade and location, and some states now report biweekly. Despite the quiet market, producers remain steady, watching for clearer skies and stronger movement ahead.

- Midwest: All grades of hay steady. Alfalfa sold slightly higher and grass sold weaker. Trade slow to moderate with light to moderate demand. Buyer attendance was light as most interests are engaged in harvest.

In Kansas, there had been no change in demand, but some lower prices were reported. Trade remains slow to moderate. There is still plenty of hay to be put up and plenty of hay to be moved, but the weather has thrown a wrench on many producers' plans.

In Illinois, a small quantity of high quality of mostly alfalfa hay sold higher per bale in small squares. Alfalfa sold higher. Grass hays traded steady.

In Missouri, hay movement is moderate as early feeding has everyone paying attention to inventories on hand given the shortness of pasture and quickly approaching average first frost date. Hay prices are steady to firm.

In Nebraska, all reported hay sold steady. Overall, demand for hay is rather slow across the state for this time of year. Some hay is moving to feedlots or backgrounders as they are getting fresh calves in to wean.

In South Dakota, demand is light to moderate; best demand continues to come from out-of-state interests. High-testing alfalfa hay is harder to find this year as the persistent rain showers and high humidity kept hay from curing quickly.

- East: In Alabama, hay prices are steady, trade moderate with moderate supply and demand.

In Tennessee, no price comparison is available due to no recorded trades last month.

In Pennsylvania, premium hay grades remain in strong demand, with prices holding firm amid tightening supply. Seasonal shifts and cooler weather are slowing harvests, but buyers continue to prioritize quality, keeping market movement steady.

- Southwest: In California, trade activity and demand were moderate to good. Retail hay demand was good. Dairy hay demand was steady.

In Oklahoma, demand is slow to some movement. Oklahoma continues to cut and bale more hay. This adds to the supply of hay we have across Oklahoma.

In Texas, hay prices are steady with light to good demand. Some cooler temperatures contributed to good demand for hay.

- Northwest: In Montana, hay sold generally steady. Few new hay sales were seen because producers are busy with fall harvest.

In Utah, demand has been slow, which has been steady. Three-way hay demand remains steady. Hay producers are finishing fourth cutting and getting in the mindset of moving hay and assessing inventory afterward.

In Idaho, demand for hay is slow; the quality of hay is looking better than it was at the beginning of the season, but there doesn't seem to be a lot of buyers looking for hay. Some are holding onto hay waiting for better prices.

In the Washington-Oregon Columbia Basin, all grades of hay steady. Trade remains slow as recent thunderstorms and smoke from wildfires has decreased the quality of hay in the trade area. Demand remains light to moderate.

In Wyoming, reported hay sales sold steady. Buyer inquiry and demand has picked up. Some hay is going to ranchers that have lost winter grazing due to fires. Some producers are finishing third cutting in the east and finishing second cutting in the west.

In Colorado, trade activity and demand moderate. As the hay season is ending, it is becoming harder for buyers to find hay without rain damage or striped from dew.

Other things we’re seeing

- Dairy: November 2025 milk production remains strong, but year-over-year output is slightly down. Cow numbers are steady, and productivity per cow continues to increase, yet seasonal slowdowns and price pressure persist.

- Cattle: November 2025 cattle outlook shows continued tight supplies and record-high prices. Feedlot placements and marketings are down, while cow retention hints at future herd rebuilding.

- Fuel: National average fuel prices were slightly higher to start October, according to the U.S. Energy Information Administration (EIA). The U.S. retail price for regular-grade gasoline averaged $3.12 per gallon on Oct. 6, up 0.6 cents from the previous week and 1.2 cents less than the same week a year earlier. The average U.S. on-highway price of diesel was $3.71 per gallon, down 4.3 cents from the prior week and 12.7 cents more than early October 2024.

- Trucking: Spot flatbed prices were mostly higher to start October, down in the South, higher in the Southeast, Midwest, South, Northeast and West, averaging $2.48 per mile nationally, according to DAT Trendlines. Regionally, average spot prices per mile were: Southeast – $2.69, Midwest – $2.56, South – $2.57, Northeast – $2.34 and West – $2.22.

- Other costs: The USDA’s prices paid index rose 0.9% in August, reaching 152, an increase of 9.9% from a year ago. Diesel, nitrogen and cattle prices continued to drive the increase, while feed and fertilizer showed mixed movement. September data has not yet been released, but August’s figures reflect ongoing cost pressure across farm inputs.

- Total July feed prices: After holding steady in July, total feed prices edged up in August. The USDA’s feed price index rose to 116.3, a 1% increase from July, though still 1.4% below August 2024 levels. This increase breaks the summer trend of easing costs, with slight gains across feed grains and complete feeds offsetting continued softness in hay and supplements.

- Interest rates: USDA Farm Service Agency (FSA) interest rates for farm operating loans (4.875%) decreased and direct ownership loans (5.875%) were lower for September. No update available.