In early September 2025, U.S. hay markets are steady but regionally mixed – high-quality alfalfa holds value in the Midwest, while grass hay prices vary widely. Rainfall is abundant in the Southeast and Pacific Northwest, but the Plains and West remain dry. Cooler temperatures are settling in the East, while the West stays warm, delaying dormancy and complicating fall forage plans.

Here’s a review of what we do know about hay and forage markets as you continue to look for answers.

U.S. Drought Monitor maps indicate that U.S. drought conditions continue to fluctuate across regions. September started with a reversal of August’s cautious optimism. Drought is expanding again across key forage-producing regions, especially the Midwest, where dry weather has rapidly intensified conditions in Missouri, Illinois, Indiana and Ohio. Soil moisture is decreasing and fire risk is increasing – particularly in areas where late-summer heat has outpaced rainfall.

Cooler air is setting in east of the Rockies, but it’s falling short of easing moisture loss.

For forage producers, the September maps signal a tightening window: Late-season growth may stall, harvest quality could suffer, and fall planning now hinges on moisture that may not come.

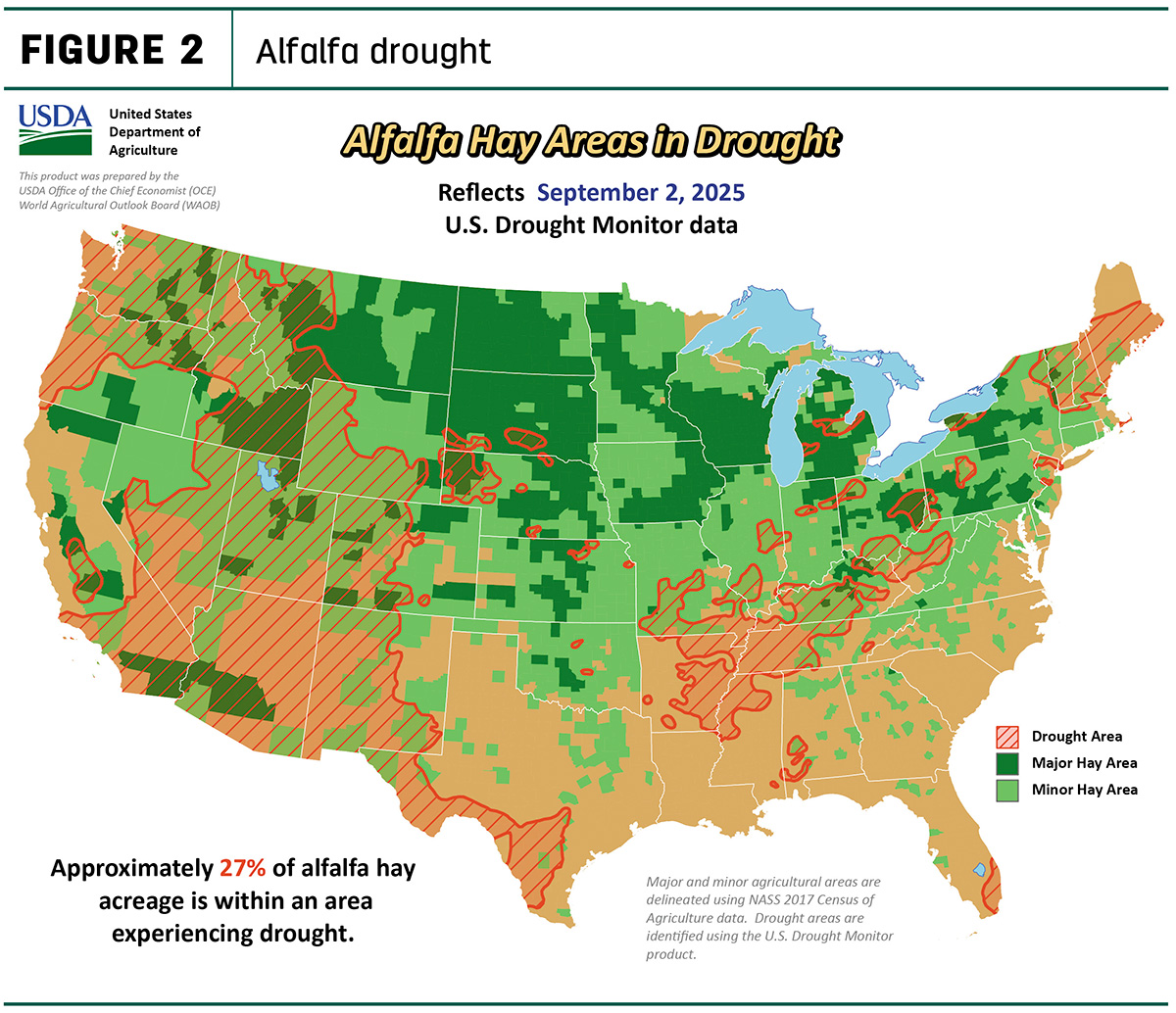

As of Sept. 2, approximately 24% of U.S. hay-producing acreage (Figure 1) was considered under drought conditions, an increase of 7% from a month earlier. The estimate of alfalfa hay-producing acreage (Figure 2) under drought conditions decreased slightly to 27%, down 1% from a month earlier.

A snapshot of hay prices

USDA price data for 27 major hay-producing states is mapped in Figure 3, illustrating the most recent monthly average price and one-month change. The lag in USDA price reports and price averaging across several quality grades of hay may not always capture current markets, so check individual market reports elsewhere in Progressive Forage.

Dairy hay

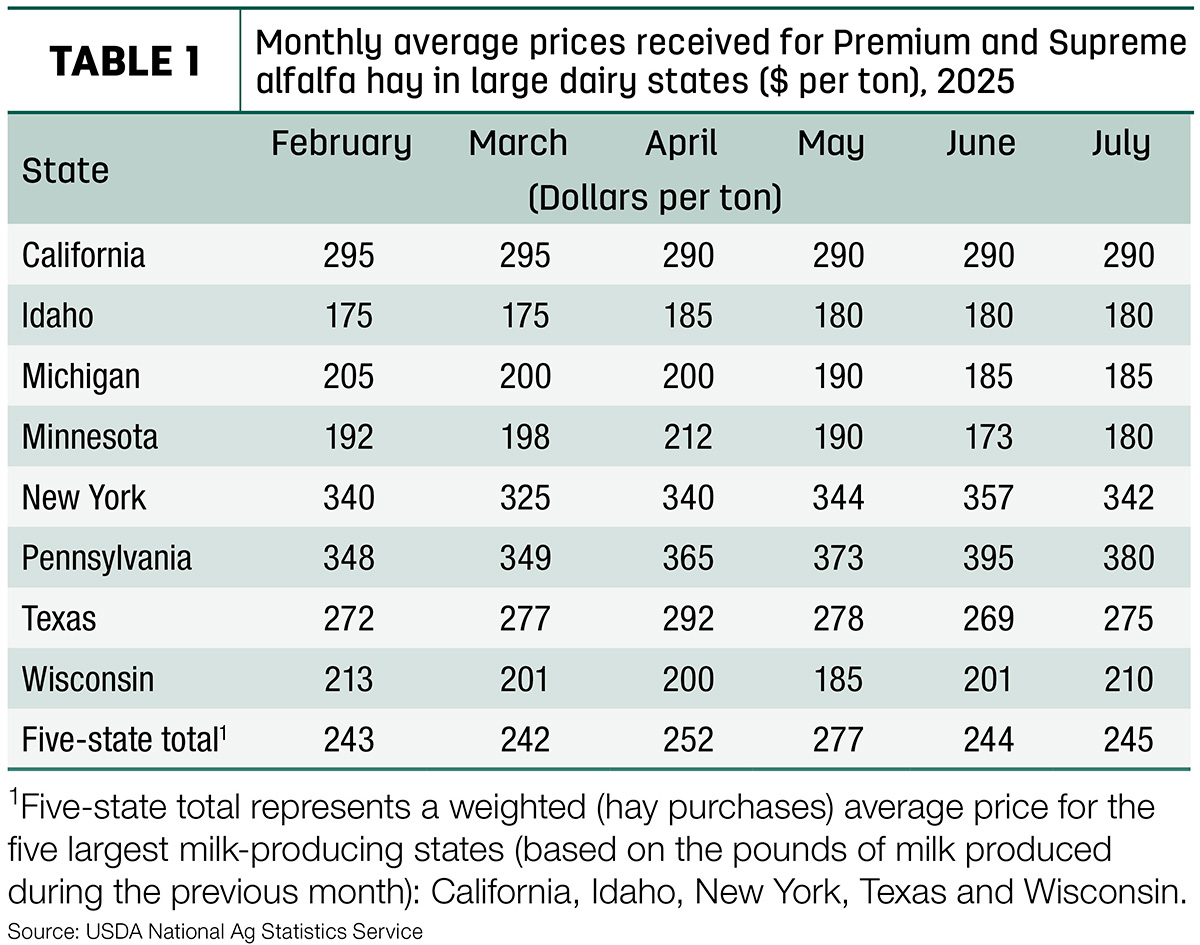

The top milk-producing states reported an average price of $245 per ton for Premium and Supreme alfalfa hay in July 2025, a $1 increase from June 2025 (Table 1). The average price was $8 higher than May 2024.

Alfalfa

The U.S. average price for all alfalfa hay decreased $4 in July to $173 per ton. Compared to a month earlier, prices were lower in 11 of 27 major forage states, with the largest declines in Arizona, California, Idaho, Iowa, Kansas, Minnesota, Nebraska, Nevada, Ohio, Oklahoma and Oregon. Prices were up in eight states including Colorado, Illinois, Kentucky, New Mexico, North Dakota, Texas, Utah and Wisconsin.

With few exceptions, year-over-year alfalfa hay prices were down substantially, with the U.S. average down $10 compared to July 2024.

Other hay

At $144 per ton, the July 2025 U.S. average price for other hay was up $3 from June. Prices decreased in nine of 27 major hay-producing states, with the largest month-to-month decrease in Iowa, Kansas, Nebraska, New York, North Dakota, Ohio, Oklahoma, Pennsylvania and Wisconsin. Increases were recorded in 13 states: California, Colorado, Idaho, Illinois, Kentucky, Minnesota, Montana, Nevada, New Mexico, Oregon, Texas, Utah and Wyoming.

Expanding the timeline, the July 2025 U.S. average price for other hay was $10 less than a year earlier.

The gap between average U.S. alfalfa and other hay prices was about $29 per ton in July.

Exports

At deadline, July exports held steady, with early gains tapering as global buyers grew more selective. Tariff questions and weather-related quality concerns continue to influence exports.

At 128,303 metric tons (MT), July exports of alfalfa hay decreased. Japan was the top buyer, importing 28,835 MT during the month, about 22% of the total. June shipments to China declined to 24,190 MT, 19% of the total for July.

Exports of other hay increased slightly to 74,409 MT in July. As usual, Japan and South Korea led buyers in the other hay category: Japan purchased 44,017 MT during the month, or about 59% of the total, followed by South Korea’s 16,157 MT, 22% of the total.

U.S. exports of most categories of alfalfa cubes and meal were lower in July, totaling about 6,112 MT. Japan imported about 74% of the total.

Regional markets

Regional hay sales and USDA Ag Marketing Service market reports remain mostly steady, with light to moderate demand. Prices vary widely by quality and region. Export movement is very light and few confirmed shipments. Many exporters are holding back, watching global signs and focusing on domestic markets.

- Midwest: In Iowa, compared to last market, all grades of hay steady to firm, especially on alfalfa on a smaller supply of offerings. Many buyers are preoccupied with silage cutting and will be for the next couple of weeks. Trade active with good demand.

In Kansas, demand was light and prices were steady. Trade remains slow to moderate. Producers continue to bale hay, despite the rain. Conversations revolved around there being lots of grinder hay available but not much high-quality hay.

In Illinois, comparable hays in small squares traded mostly steady, and comparable hays in large packages traded steady to lower.

In Missouri, hay movement has been mostly slow, prices are steady to weak, supplies are heavy, and demand is light to moderate.

In Nebraska, reported hay sales sold steady; demand is light.

In South Dakota, demand is light for all types of hay, best demand coming from out-of-state interests. With the large carryover of old-crop hay across the greater region, interest in buying hay has been fairly light. High-quality hay is in tighter supply.

- East: In Alabama, hay prices are fully steady. Trade moderate with moderate to good supply and demand.

In Tennessee, too few trades for a price comparison.

In Pennsylvania, holding firm with Premium grades commanding strong prices and steady movement despite a slight dip in volume. Buyers remained quality-focused as seasonal shifts began to tighten supply.

- Southwest: In California, trade activity and demand were slow. Retail and dairy hay demand was steady while export hay demand was very light.

In Oklahoma, demand is mainly at a standstill. There has been hardly any movement of hay being traded.

In Texas, hay prices are mostly steady with some instances lower prices, light to moderate demand. Adequate to excellent supplies were reported in all regions.

- Northwest: In Montana, hay sold generally steady, demand was mostly moderate, and supplies of grain hay remain large.

In Utah, demand has been steady to slightly higher, but movement is slightly lower. A few bigger sales are being made with hay going to California, and some smaller sales are being made to local ranchers to feed. Feeder hay prices are increasing due to the demand starting to grow, especially grain hays.

In Idaho, demand for hay is slow, the quality of hay is looking better than it was at the beginning of the season, and a few contracts were made for feeder hay.

In the Washington-Oregon Columbia Basin, alfalfa is weak and retail hay steady. Smoke from surrounding wildfires affecting quality of hay. Trade moderate with moderate to good demand.

In Wyoming, most hay sales sold steady; demand was mostly light to instances moderate. Some producers are getting very low-quality hay sold to feedlots, dairies and hay grinders mostly going to out-of-state customers. There appears to be a limited amount of that quality of hay produced so far this year.

In Colorado, trade activity and demand moderate. Small squares of horse hay sold mostly steady.

Other things we’re seeing

- Dairy: October milk production remains strong, with herd sizes steady and year-over-year gains in output per cow. However, month-over-month growth is slowing, hinting at seasonal limits and potential price pressure if demand lags.

- Cattle: The outlook for 2025 beef production is lowered 262 million pounds from last month to 25.926 billion pounds for an expected year-over-year decline of 4%. This is the result of slower than previously anticipated pace of cattle slaughter and lower expected carcass weights in the second half of the year. The pace of slaughter in July and early August was much slower than expected, and fewer-than-anticipated placements in June lowered expectations for marketings in late 2025. Lastly, cow slaughter for 2025 is adjusted lower.

- Fuel: National average fuel prices were slightly higher to start September, according to the U.S. Energy Information Administration (EIA). The U.S. retail price for regular-grade gasoline averaged $3.18 per gallon on Sept. 1, up 3 cents from the previous week and 11.2 cents less than the same week a year earlier. The average U.S. on-highway price of diesel was $3.73 per gallon, up 0.3 cent from the prior week and 1.9 cents more than early September 2024.

- Trucking: Spot flatbed prices were mostly lower to start August, down in the Southeast, Midwest, Northeast and South, only higher in the West, averaging $2.45 per mile nationally, according to DAT Trendlines. Regionally, average spot prices per mile were: Southeast – $2.65, Midwest – $2.51, South – $2.58, Northeast – $2.33 and West – $2.20.

- Other costs: The USDA’s July prices paid index for commodities and services, interest, taxes and farm wage rates is up 0.5% from June 2025 and 7.9% from July 2024. Diesel, cattle and nitrogen drove the increase, while feed and fertilizer prices showed mixed movement.

- Total July feed prices, the index is 115.2, unchanged from June and down 2.2% from July 2024. This continued the summer trend of easing feed costs, with declines across hay, feed grains, complete feeds and supplements.

- Interest rates: USDA Farm Service Agency (FSA) interest rates for farm operating loans (4.875%) decreased and direct ownership loans (5.875%) was lower for September.