Heifer inventory is always a central topic in conversations with dairy producers. Shifts in market conditions can quickly influence breeding strategies, particularly decisions around semen type. Recent increases in beef prices are a clear example. Higher beef prices have created opportunities for dairy operations to generate additional revenue through dairy-beef crosses, raising an important and recurring question: Should I be breeding more beef semen or more dairy sexed semen in my herd?

While the question itself is straightforward, the answer rarely is. A successful breeding strategy depends on multiple interrelated factors. The first is whether a producer is generating enough replacement heifers to sustain herd size and any planned expansion. Producing too many heifers can reduce margins as additional replacements increase feed, housing and labor costs.

Extension estimates place the cost of raising a heifer to 24 months old between $1,700 and $2,200. Conversely, producing too few heifers may force a farm to purchase replacements, potentially at unfavorable market prices.

Therefore, understanding the replacement market is equally important. When there is a surplus of heifers nationally or regionally, the cost to purchase replacements may approach the cost of raising them, making it economically reasonable to buy replacements and allocate more breedings to beef semen. The same market dynamics apply to dairy-beef calves. In recent years, a short supply of growing beef calves has driven dairy-beef cross prices sharply higher, in some cases bringing the value of a day-old calf close to the full cost of raising a dairy replacement heifer. Under those conditions, selling more calves to beef markets can appear to be a very attractive business decision, and in many cases, it has been.

Of course, producers do not have access to a crystal ball that predicts future markets. Disease outbreaks, policies and other external factors can rapidly shift supply and demand in ways no model can fully anticipate. However, predictive models remain valuable tools. When built thoughtfully, they help frame risk, identify trends and guide decision-making under uncertainty.

Understanding models

Most models begin with known or observable inputs and work forward using assumptions derived from historical data, research and industry benchmarks. In the context of heifer supply, those starting points may include semen sales, proportions of sexed versus conventional semen or historical culling rates. From there, models apply assumptions about conception rates, pregnancy loss, calf sex ratios and heifer completion to estimate future replacement availability.

In practice, producers use simplified versions of these models every day. Adjusting feed deliveries as cattle move between pens, estimating how many cows must be bred with sexed semen to maintain herd size or determining how many replacements must be purchased in a given month all rely on assumptions layered onto known information. Even deciding which cows to sell when a favorable market opportunity arises could, at its core, be a form of modeling.

The challenge of predicting the future

The inherent limitation of any model is that it cannot perfectly account for every factor influencing biological or economic outcomes. Adding more known variables can improve precision, but each assumption introduces potential error. The risk is not in using models but in misunderstanding how sensitive their outputs may be to the assumptions embedded within them.

That said, when multiple independent models point in the same direction, confidence in the general trend increases, even if the exact magnitude remains uncertain.

In 2025, CoBank released a comprehensive report suggesting that the U.S. dairy industry is going to face a short supply of replacement heifers through 2027. Their analysis incorporated extensive historical and market data, including dairy cow culling trends, semen sales and adoption of sexed semen. At the same time, the model necessarily relied on several assumptions, such as how sexed semen is allocated across lactation groups, conception rates by semen type, pregnancy loss, culling of pregnant cows and heifer completion rates.

What are we trying to achieve?

This article is intended as a starting point for evaluating some of those assumptions using observed, farm-level data. Using our database, we aim to provide additional context that can support future projections and ultimately help producers make more informed breeding decisions.

An additional goal is to move beyond national averages. While national trends are important, dairy investment and expansion are not evenly distributed across the U.S. For example, large investments in new milk processing capacity may significantly increase replacement demand in surrounding regions while having little effect on markets hundreds of miles away. Understanding regional dynamics may therefore be just as important as understanding national supply.

What does farm data tell us?

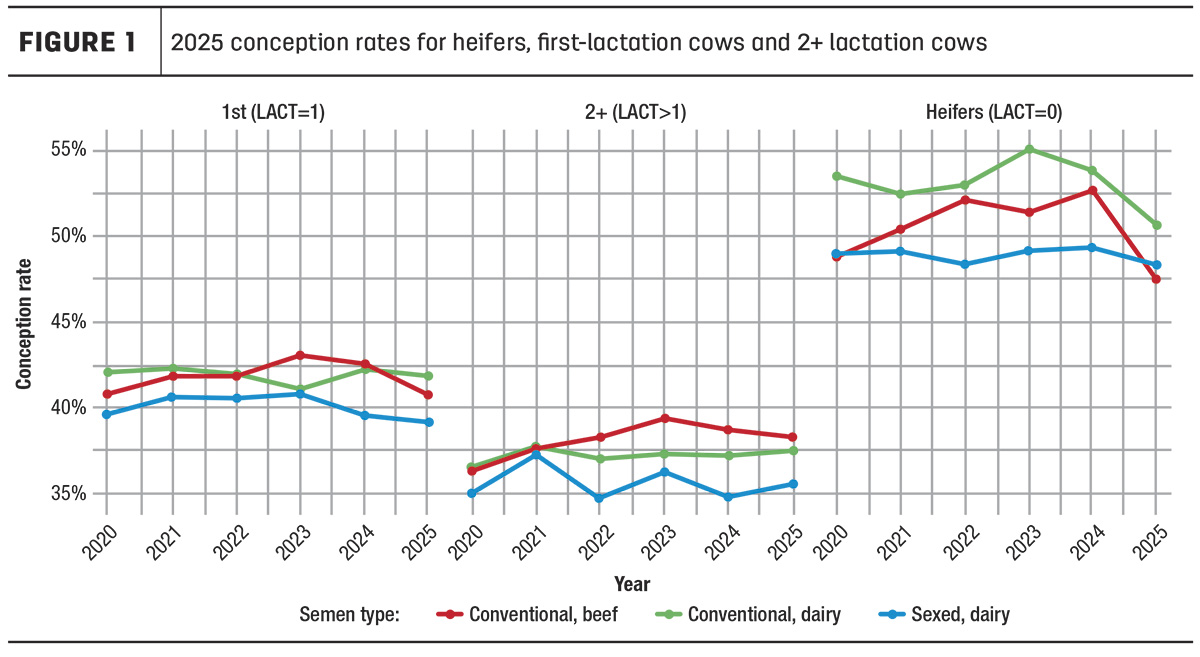

Our database shows an overall conception rate in 2025 of 48.4% for heifers (lactation 0), 40.2% for first-lactation cows and 37.6% for cows in second lactation or greater, with results aggregated across cow breeds. For heifers, conception rates were 48.2% for sexed semen and 50.6% for conventional dairy semen. In first-lactation cows, conception rates were 39.2% for sexed semen and 41.9% for conventional semen, while older cows achieved conception rates of 35.6% and 37.5%, respectively (Figure 1). Overall, conception rates for conventional and female sexed semen in the database were lower than those assumed in the CoBank model.

Pregnancy loss rates were also modestly higher in the database. In 2024, overall pregnancy loss was approximately 8.2%, compared with the 5% assumed in the CoBank model. Heifers experienced the lowest loss rate at 4%, while first-lactation and older cows had pregnancy loss rates of 9% and 10.6%, respectively.

Female pregnancies and replacement generation

Herds participating in our database have grown since 2020. The number of fresh events increased from approximately 892,000 in 2020 to 1.1 million in 2025, representing an average annual increase of about 4% over the past five years (Figure 2). While fresh events are not equivalent to herd size, they provide a conservative proxy for herd growth within the database.

After accounting for confirmed pregnancy losses, and assuming that 90% of sexed semen and 50% of conventional semen result in female calves, participating herds generated approximately 454,900 female pregnancies in 2020. That number increased to roughly 531,900 in 2024. Female pregnancies grew at an approximate annual rate of 6%, 3% and 8% in 2022, 2023 and 2024, respectively. In 2025, female pregnancies were approximately 3% higher than 2024 levels; however, a portion of these pregnancies is still ongoing, and associated pregnancy losses have not yet occurred.

Using annual fresh events as the denominator, and assuming a 79% heifer completion rate, farms in the database produced approximately 38% replacement heifers in 2021, 2022 and 2023, increasing to about 40% in 2024. Preliminary results for 2025 indicate 39.2%; however, this value includes ongoing pregnancies that may still result in pregnancy loss.

Looking ahead

This analysis does not attempt to define a precise heifer inventory, nor does it seek to challenge existing national projections. Rather, it illustrates how observed farm-level data from herds contributing to this database compare with commonly used model assumptions, emphasizing the importance of understanding the inputs that drive predictive outcomes.

Future work will expand this analysis to include sold and died events, along with regional breakdowns that may better reflect localized market dynamics. Together, these insights can help producers more clearly evaluate risk and align breeding strategies with both biological performance and market realities.