According to the USDA, the national corn crop in 2016 was in the neighborhood of 15.2 billion bushels; prices are hovering somewhere around $3.50 per bushel, which is much less than those prices we saw in 2012 (an average of $6.89 per bushel), but much more than what we paid in 2005 ($2 per bushel).

We do remember those few months when national prices nearly surged to $8 per bushel. Will we ever see $8 corn again? The answer is yes. When will this happen? I don’t know. What I can tell you is what it would take, approximately, for corn prices to surge to $8 per bushel.

“Toto, I’ve a feeling we’re not in Kansas anymore” … or Iowa … or Illinois

It’s a big world out there and most of its components (i.e., countries) are now connected through trade. To understand U.S. corn prices, we have to first understand world production, use and trade of corn grain. To do this, we will use USDA data for the 2015-2016 marketing year.

World corn production

In 2015, the total world corn production amounted to an estimated 38,105 million bushels. The U.S. is still the largest corn-producing country, accounting for roughly 35 percent of the world’s production.

The five largest corn-producing countries (U.S., China, Brazil, EU-27 and Argentina) accounted for more than 75 percent of the total corn supply in 2015. (Here, I considered the EU-27 as a single country, which is not quite correct, but because EU countries share a common agricultural policy, this is inconsequential for the task at hand).

World corn consumption

During the same year, world corn consumption totaled 38,038 million bushels – roughly the same as what was produced. The U.S. led corn consumption (about 31 percent of world corn consumption), while the five largest corn-consuming countries (U.S., China, EU-27, Brazil and Mexico) accounted for 71 percent of total world corn consumption.

Corn exporters

Obviously, corn-exporting countries are those whose corn production exceeds consumption. The five leading corn-exporting countries in 2015 were the U.S., Brazil, Argentina, Ukraine and Russia. The total volume of the world’s corn exports stood at 5,050 million bushels, or 13.2 percent of total world production.

The five largest exporters accounted for 90 percent of all the corn exported, with the U.S. as a leader at 34 percent of all exports.

Corn importers

Corn-importing countries are those whose corn consumption exceeds production. The five major importers were the EU-27, Japan, Mexico, South Korea and Egypt, but these five largest corn importers accounted for less than 47 percent of all corn imports. More than 35 percent of all corn imports are from countries that do not even appear in the list of the 10 largest importing countries.

What to make of it

First, the U.S. is obviously a large corn producer, but it is also a large corn consumer: 88 percent of U.S. corn production is consumed domestically. Second, the total amount of corn traded across countries is a relatively small proportion (13.2 percent) of the world’s production. Third, although the U.S. still leads all countries among corn exporters, its exports represent only one-third of total world corn exports, or less than 5 percent of total world production.

Fourth, the export market is fragmented among many counties – even the 27 EU countries amounted to only 12 percent of all corn imports. Hence, international corn trading is not for the faintest of hearts, and large changes in U.S. corn exports are not to be expected unless a disastrous corn crop occurs in either China or South America (Brazil, Argentina).

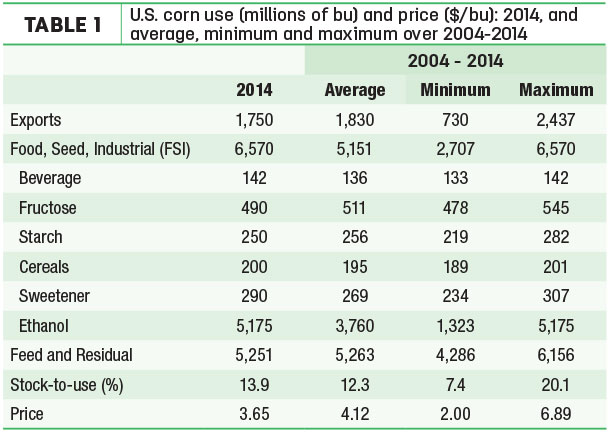

U.S. corn usage by segment

In 2014, the U.S. consumed 13,600 million bushels of corn in a year when 14,200 million bushels were produced. Where did all these bushels go? Table 1 provides the answer to this question.

To give you an idea of how domestic corn usage changed through time, Table 1 also reports the average, minimum and maximum usage for each segment between 2004 (pre-ethanol boom) and 2014.

Basically, corn usage is reported for three major segments: (1) exports, (2) food/seeds/industrial (FSI) and (3) feed/residual (F/R). The last segment is never actually “measured.”

Because there has to be a mass balance (i.e., no corn can mysteriously appear or disappear), the third segment is simply calculated from corn usage not accounted by the first two segments. What do we make out from the data in Table 1?

- Some usage segments simply do not vary much. Except for ethanol, all FSI segments simply don’t vary much. Economists would say that the demand for corn is inelastic to corn price. For example, the amount of corn flakes sold as a breakfast cereal doesn’t change much with the price of corn.

Therefore, the total amount of corn used by these segments can be considered nearly constant and predictable.

- One sector, corn used for ethanol production, has seen substantial growth, but not because of corn price. The Renewable Fuel Standard (RFS) – an outcome of the Energy Policy Act of 2005, followed by the Energy Independence and Security Act of 2007 – administered by the EPA sets the amount of renewable fuel that fuel suppliers must use in the U.S.

Therefore, the amount of corn use by this sector is nearly as predictable as ... politics. For now, we will consider the amount of corn used for ethanol production as highly predictable based on the current RFA mandate.

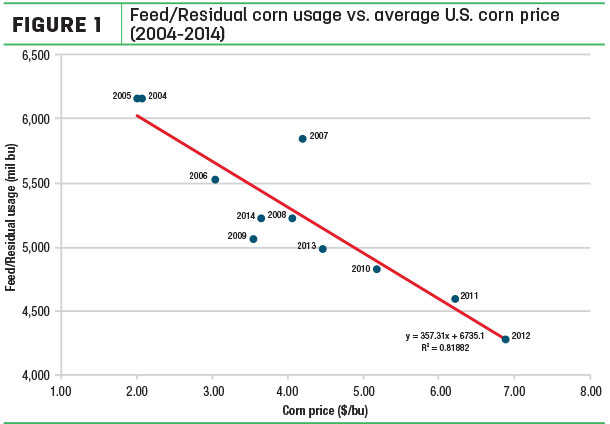

- As shown in Figure 1, the amount of corn used for feed/residual (F/R) is highly dependent on price. For a given corn price, we can predict reasonably well the total corn demand for F/R.

- The amount of corn exported varies, but mostly from factors affecting world supply and demand. These are unpredictable: We don’t know what the corn crop in China will be next year. In our analysis, we’ll be using the projected exports for the 2016-2017 crop year, with the understanding that much uncertainty surrounds this number.

What drives domestic corn price

The laws of economics are not violated when it comes to corn prices. The balance between supply and demand is the primary driver of our domestic prices. Two relationships will make corn prices somewhat predictable. The first one is absolutely exact.

It is simply the mass balance of corn over a crop year. Put in semi-algebra, it states:

Ending stocks = (Beginning stocks + production) – (Domestic consumption – exports + imports)

Because domestic consumption is simply the sum of FSI and F/R, the equation can also be written as:

Ending stocks = (Beginning stocks + production) – (FSI – F/R – exports + imports)

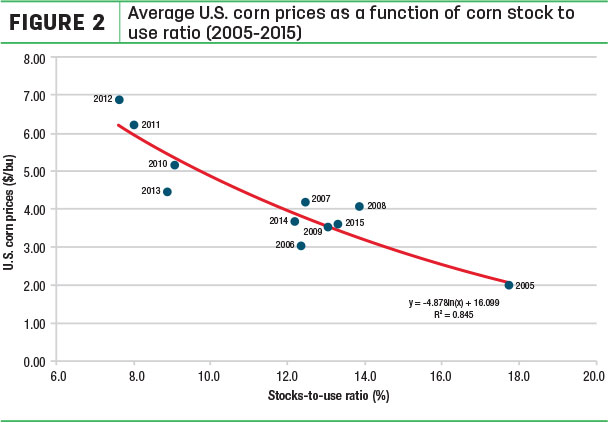

The second relationship is not as exact. As shown in Figure 2 there is a strong relationship between the amount of corn remaining in stock at the end of a crop year (expressed as a proportion of corn usage, which is the sum of domestic consumption and exports) and the price of corn.

This relationship is empirical, but it does make a lot of sense: The more corn left in stock at the end of a year, the lower corn prices are.

What would it take to have $6 corn next year?

I know that the title of this article was about $8 corn, but we haven’t seen $8 corn often before. It would be dangerous to extrapolate Figures 1 and 2 to $8 corn. So we’ll be a little more reasonable and wonder what it would take to get $6 corn, say for next year.

Remember that we know quite well what FSI will be, about 6,650 million bushels. We also know quite well the amount of corn we should have as beginning stocks: 2,300 million bushels. Using Figure 1, we estimate that F/R would be about 4,600 million tons if corn was to be priced at $6 per bushel in 2017-2018.

We don’t know the amount to be exported, but we’ll take an educated guess at 2,200 million bushels. The amount of corn imported is always relatively small: We’ll set it at 50 million bushels. From Figure 2, we figure that the stocks-to-use ratio would need to be around 0.08 (i.e., 8 percent) to get $6 corn.

At this point, the only remaining unknown is the amount of corn to be produced in the U.S., but there is only one number that would result in a stocks-to-use ratio of 8 percent. That is U.S. production at or below 12,180 million bushels.

How likely is the next U.S. corn crop to be short of 12,180 million bushels? I don’t know! But in five of the last 11 years, the U.S. corn crop was less than 12,180 million bushels. I’m not saying that there is a 5 in 11 chance for the crop to be below 12,180 million bushels; the economic conditions have changed too much over this span of time.

But 2012 was not that long ago, and corn production in the U.S. that year was only 10,755 million bushels. Some might say that 2012 was a “black swan” – a very uncommon occurrence. Well, how about 2011? That wasn’t a disastrous crop year, and total U.S. corn production was only 12,300 million bushels that year.

How many acres of corn will be harvested next year? This year, we had a fabulous year and harvested an estimated 86.6 million acres. But what if we have a lousy spring and some acres are switched to soybeans? What if some planted acres are so badly flooded that they are never harvested?

What if we harvest the same number of acres as, say, 2015-2016 or 80.7 million acres? All it would take then is an average yield of 151 bushels per acre, and “bang,” production would be at 12,180 million bushels and we likely would see $6 corn.

Remember the Alamo!

It’s one thing to get beaten up by feed prices as we did in 2012, but to naively plan as if this will never happen again is missing an important lesson we should have learned from the past. I don’t know what the future holds, but I know that if it’s a bad crop year in South America, China or North America next year, we could very well see $6 corn, or even $8 corn.

I also know that one can manage some of that risk by not being overly greedy. This means that dairy producers should cover at least a portion of their future needs when prices are somewhat reasonable – i.e., you can make some money by turning corn into milk.

I also know that cows do not require corn and can eat a wide range of feeds. So I can look for something else to feed.

So will we see $8 corn next year? I don’t know, but I know that we could! ![]()