Where is the optimism in the dairy industry? What should the producer hang his or her hat on when the milk price less feed cost goes from over $11 per hundredweight (cwt) to a projected level under $7 per cwt? The future can be projected but the actual situation is not known until the future has arrived. What is known, however, is the financial data that paints a picture of the trends in an individual operation and in a cohort group of similar dairy producers. Looking to the past with financial benchmarking can provide insight into the future, even when the industry is experiencing the stress that exists in 2012.

The 2011 data for Minnesota dairy producers shows significant similarities to 2010 – giving dairy farmers the second profitable year after the severe stress of 2009. As students in the Farm Business Management Education program (FBM), 468 dairy producers used a thorough set of business records to benchmark their business in a unique subset of dairy production in Minnesota.

Each producer in the FBM program uses a farm business analysis using FINPACK through the Center for Farm Financial Management (CFFM) at the University of Minnesota . The data from these producers is merged into a state database which is hosted by CFFM in FINBIN .

The Farm Business Management program is offered through Minnesota state colleges and universities and regional and statewide data.

This unique database shows a significant increase in average herd size for 2011 to a level of 158 cows, up from 142 cows in 2010. This dairy database includes 11 percent of all herds in Minnesota and 35 percent of all operations with a herd size of over 200 cows. These percentages are based on herd size estimates provided by the Minnesota Department of Agriculture.

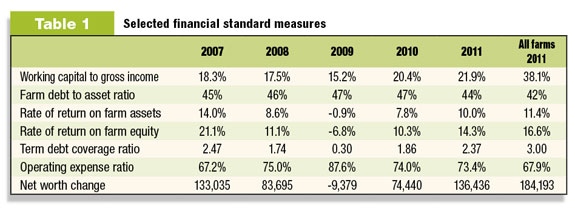

Whole-farm financial data

Minnesota dairy producers experienced positive returns in 2011, even with continued increases in their costs of production.

In Table 1 , it is evident how trends from 2007 to 2009 mirror the trend from 2009 to 2011. These selected financial factors can be measured from year to year for the individual producer to evaluate business decisions that impacted these trends and how those decisions were influenced by the marketplace.

Dairy producers continue to experience weakness in liquidity measures but did demonstrate improvement in all factors for the second straight year.

The right column in Table 1 shows the data for all producers in the state database, where crop operations, which were very profitable, amount to about 50 percent of the total group. Dairy operations were slightly lower than the state average for these whole-farm factors but demonstrated similar positive signs overall.

With two consecutive years of profitability, there was gain in the overall business stability. In 2011, the median net farm income increased by over $25,000 above 2010, to a level of $94,664. That positive trend in the revenue stream resulted in a significant net worth change, where the average farm showed a $136,436 gain in net worth on the market balance sheet.

While some of this increase resulted from changes in the estimated value of assets, this positive movement was fueled primarily by the improved milk price. The current outlook for price suggests a negative impact on these numbers in 2012.

Data by herd size

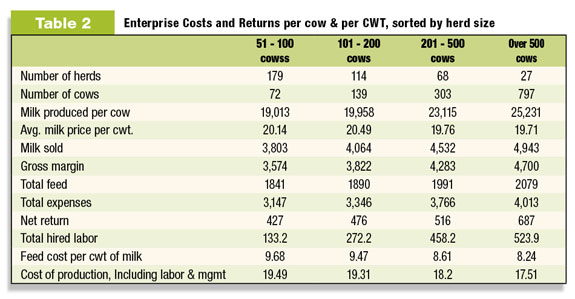

Table 2 demonstrates the variations found when these Minnesota operations are sorted by herd size.

The steady increase in milk produced per cow as herd size increases continues in 2011. Net returns per cow show a similar increasing trend based on herd size; over double the increase from 2010.

With that said, smaller herds continued to struggle to generate adequate revenue to cover family living and repayment of debt. The improved margin in 2011 was not adequate for smaller herds because the business volume was not adequate to generate the needed revenue.

Average milk price has not varied significantly by herd size in recent years. What has continued to stand out is the revenue generated per cow as herd size increases. The ability to focus on production and cow satisfaction in the larger herds earns financial gain for the larger producers.

Even though total direct and overhead costs increase with herd size, the additional revenue resulting from increased milk production more than covers that increase.

Feed costs have moved to a new plateau, exceeding the extreme levels of 2008. Based on the overall commodity pricing at the current time, this plateau is here to stay. Anticipating that feed costs will be in the $8 to $9 range for 2012, the milk price less feed price is heading to a level similar to 2009.

Producers must ask: What changes have I made since 2009 that will generate added revenue if or when conditions approximate that difficult environment?

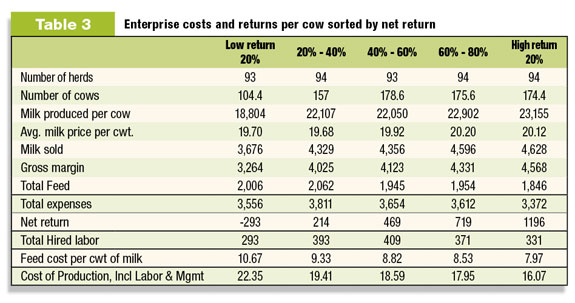

Data by profitability group

The first thing that stands out in Table 3 , sorting these farms into high-profit and low-profit herds, is the relative steadiness of farm size and production per cow in the three higher-profit categories.

Those similarities would suggest that high returns per cow can result from both smaller and larger-size operations.

A herd size of 175 to 180 cows is only slightly larger than the overall average size of 158 cows. The high- return farms show the highest milk production per cow, which has not been the trend in recent years.

Another significant difference is shown in the feed cost per cwt of milk produced. There is a steady reduction up to the high-return farms, which have a feed cost just below $8 per cwt of milk. That same trend was true in the total cost of production and total expenses as well.

The top three return categories see a net return that is over double, and up to almost six times, that of the 20 to 40 percent return group. The financial benefits of cost containment and strong milk production levels are demonstrated very clearly in this dataset.

Summary thoughts

Profitability over the past five years in the dairy industry in Minnesota has been varied. The need to generate adequate volume in the business has been demonstrated by the steady increase in herd size, having a significant increase in 2011. Profitability can be found in herds of varying sizes and that will be true in the future as well.

This article opened with questions about optimism regarding the future.

Highs and lows in farming are given and producers understand that situation. Current times suggest, however, that some producers are being tested yet again in 2012. Decisions related to herd size, whether expanding or contracting, will be occurring – along with decisions related to increased emphasis on crop production due to the current price situation with the major crops.

Decisions in these difficult times need to be made with controlled emotions and a strong business management influence. Understanding the individual farm financial picture, comparing it to the benchmark data of their peers and discussing the options with an adviser who has firsthand knowledge of the financial aspects of the industry, such as an FBM instructor, will be critical in 2012 and beyond.

Optimism is earned when decisions are based on complete financial records for the business. With quality data as a foundation, producers can build an understanding of the strengths of their dairy enterprise and their costs of production.

When producers “know their numbers,” optimism in difficult times comes from confidence in their ability to interpret benchmark data and apply that knowledge to improve their business.

PD

Lecy is associate dean at Central Lakes College , a member of the Minnesota State Colleges and Universities System and Nordquist is associate director of the Center for Farm Financial Management at the University of Minnesota .