I wrote earlier this year about the drivers of U.S. milk production and, in particular, the link between the dollar margin over feed cost and production growth trends (See “U.S. milk production: Shouting down the supply chain,” May 2nd issue, pg. 23). It seemed clear at the time that the sharp decline in seasonal production during the latter part of 2010 was due to a margin squeeze on dairy producers – feed prices were rising and milk prices falling.

In the first quarter of 2011, milk production lagged well below the long-term growth trend line. (See Figure 1 .) A milk price rise was required to stimulate growth and feed the normal increases in U.S. milk demand as well as rapidly increasing dairy exports.

At the time, buyers were not listening. In fact, they were suggesting the reverse should happen, with Class III and IV futures seeking a lower price point during the course of 2011. Almost six months later, it is an interesting point in time to see how the U.S. dairy industry has responded to the tension between market demand and producer margins and profits.

The price signal resets

In my earlier article, I noted that if buyers wanted more milk they would need to show producers the color of their money, and so they did. During May the short-term futures for Class III and IV milk started rising again. This translated into higher milk prices in June and record-high prices in July and August.

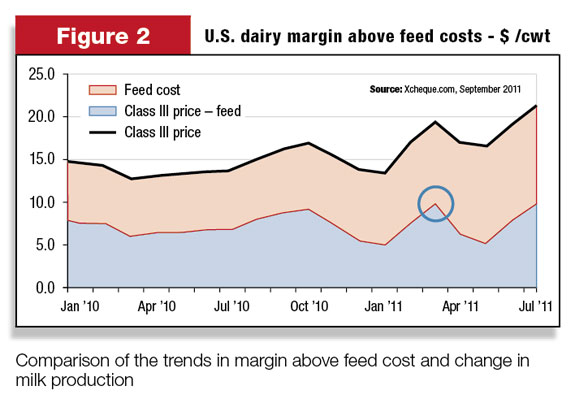

Figure 2 shows the U.S. average Class III price. Also shown is the cost of a typical feed mix (corn, soybeans, alfalfa). The blue area at the bottom of the chart shows how much money is left over after feed costs – the margin available to contribute to all other costs and any residual profit.

The buyers appear to have played their part in the supply and demand game, lifting the margin after feed cost back above the level of $10 per hundredweight (cwt). From our prior analysis, this appears to be the point that supply growth is stimulated and starts to accelerate. Significantly, the increase in margin for Class III milk is very sharp, doubling from $5 per cwt to just under $10 per cwt.

… and production follows

My comments here may well be in conflict with the sentiment in the mainstream press over the past few months. I have seen comments like “July saw the lowest rise in year-on-year U.S. dairy production since February 2010.” The implications are that milk production growth is slowing. In fact, the reverse is true.

In fact, as shown in Figure 1 , daily U.S. milk production is shown after correction for normal seasonal variation. The long-term trend is for approximately 1 percent annual growth in production. The chart shows that in the past two months, milk production has climbed back above the long-term trend line, recovering much of the ground lost in the early part of the year.

Bang, bang control in action

The cause-and-effect relationship in U.S. and global milk production can be hard to find. My contention has been that production responds to price signals very crudely – it drifts along until there is a strong and obvious market signal to change or when critical limits are reached – the so-called bang, bang control theory. The past six months of data has provided more evidence for this theory.

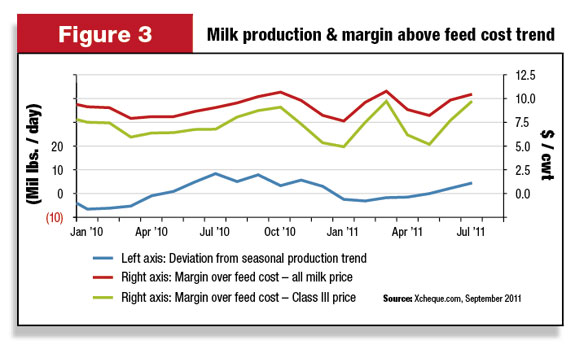

Figure 3 (on page 36) shows the deviation from the milk production trend over the past 18 months. This is the difference between seasonally adjusted milk production and the long-term trend line. A number greater than zero means milk production is growing faster than about 1 percent per annum.

Negative numbers signal a growth rate lower than this long-term trend. Also shown on this chart is the margin above feed cost using the all-milk price and the Class III price. The past three months have seen margins track back towards the magical number of $10 per cwt.

This has prompted a supply response and moved production growth back above the long-term trend line. It is all quite simple, really – if you want the milk, you have to pay for it.

The outlook from here

As you might imagine, predicting the future direction of the market is a much more difficult task than explaining past history. On the supply side, there is plenty of incentive for production growth with a reasonable margin above feed cost

International dairy commodity prices are, however, trending weaker with significant falls in the Fonterra Auction in the past two months. The U.S. dairy futures market echoes that sentiment.

At the same time, feed costs are projected higher still and so, if the future prices held, margins for Class III milk would fall back to $5 per cwt again (bang, bang, bang). This is not a recipe for continued production growth and, notwithstanding the fall in international market value, export prices are still high relative to the U.S. market.

The opportunity for export growth remains and milk prices within the U.S. will need to stay high to service both domestic and export demand.

For those watching U.S. dairy production from Europe and Oceania, there is one final piece of data that will be somewhat of concern. The increase in U.S. milk production during 2011 has been driven by increased cow numbers.

This is a relatively unusual situation. Historically, cow numbers have been relatively stagnant and production growth has been achieved via ongoing increases in milk production per cow.

Since 2008, there has been an improvement in U.S. daily milk production per cow per day for the past four years, until July’s milk production report. Milk was then tracking at about the same level as last year.

There is every indication from historical trends, and the milk-per-cow performance in early 2011, that if margins remain relatively high, milk production could be lifted by a further 1 percent and very quickly through increased production per cow. In other words, the U.S. has plenty of latent capacity to increase production and take up any short-term slack in the international market.

The media has noted that the U.S. is moving up in the rankings of international dairy exporters, and I see no reason why that trend won’t continue. PD

Dr. Jon Hauser has over 25 years’ experience in food and agriculture industries as a researcher, manager, CEO, consultant and company director. More recently he has established Xcheque.com , an online news and analysis service for the global dairy industry.