Versatility and flexibility have become two of the greatest characteristics built into products in the 21st century. My wife has a watch that doesn’t just tell the time; it also counts her steps throughout the day.

Many of us carry smartphones that allow us to do much more than make a call. Our family vehicles are made so seats can move to accommodate cargo or more easily fit passengers. Infomercials fill the airwaves with new products that can perform a multitude of tasks.

Versatility and flexibility define the modern product experience. Those two words also define the greatest characteristics and value found in the options (puts and calls) market we spent time understanding in our last article.

As a quick refresher, options establish for the buyer the right, but not the obligation, to buy or sell something at a specific predetermined price (strike price) at any time within a specified time period. A call option grants the right to buy futures contracts while the put option grants the right to sell futures contracts.

The transaction between the buyer and seller of the options involves an exchange of premium whereby the buyer pays the seller for the rights extended to him or her. The seller, after receiving the premium, is then obligated to provide the rights to the buyer at that moment when the buyer chooses to exercise that right.

We had mentioned previously that very few producers are willing to buy 100 percent of their feed needs or sell 100 percent of their milk production all in one moment. Typically, those decisions are spread out over time and involve a number of different transactions.

However, while all of those decisions are being made, different risks are still present in the market. Moreover, while that risk may be fully understood, producers often recognize that market opportunities could improve from today to some other future date.

Options provide coverage against ever-present market risk while affording the buyer of the option the ability to wait out better opportunities or wait until further knowledge about different variables is better known. Options provide better clarity to future results by transferring risk to another party in exchange for more definitive pricing. But how do we bring this together?

There are several strategies for employing the use of options based on timing, historical market performance, bias, etc. Let’s explore a couple of these strategies so you may understand how to put these tools to work. Before we get to that, let’s first talk about you … yes, you the reader.

Many times when producers use options for the first time, they are perhaps a bit confused either about how the options work or what to expect from the options market under certain market conditions.

What is equally confusing is how often the user of the option doesn’t fully understand their own ability to execute and maintain a strategy, their cash-flow capacity to service a strategy or their tolerance for risk as found in a strategy.

Too often I have received phone calls from individuals who read an article or visited with a neighbor that suggested a specific strategy they now suddenly believe will be the silver bullet in their risk management efforts.

Before you get too far down that road, be sure to have a very specific conversation with your adviser about what to expect from a different strategy under different conditions and what amount of cash that strategy may require as well as the amount of time or follow-up decisions required to service that strategy.

There are a lot of things that sound good. However, be sure of what you are committing to before you jump in with both feet. The last thing you want to do with a hedging strategy is get into it and either get spooked by the market or shocked by the commitment, only to jump out in an emotionally driven manner. It is the recipe for disaster in any hedging effort.

Back to our discussion about strategy. Before choosing a strategy, it is important to determine what type of market you are in. I am not talking about whether it is the corn market or the milk market. I am talking about the characteristics of that market at the moment in which you are addressing it.

Is it a volatile market or a generally subdued market? Are we near historical highs or lows, or somewhere in the middle of the range? Is it a large, robust market with a lot of volume or a market with very few participants and smaller volumes?

Where are you at in the normal seasonal cycle of the market? These factors will play into whether or not you should be more or less aggressive in your efforts and how large of an allowance you should make for different price movement.

For example, if Class III milk is at $12 per hundredweight (cwt), you would not be as aggressive as when milk is at $22 per cwt. Your strategy should take these things into account. You wouldn’t want to put together a strategy that requires ongoing adjustment in a market with very little participation.

On the day when the market requires a move, you may not find anyone there to offset the actions you wish to execute. Elements such as this make for great conversations with your risk management adviser.

With strategies, the most basic option hedging strategy is to begin by simply purchasing the option. We have talked about the right extended to you by doing so. Let’s bring this discussion into real-life context.

Let’s say your ration requires 150 tons of dried corn each month, and you need to purchase corn in that same amount to cover your needs. That equates to roughly 5,357 bushels or just more than a single CME contract (5,000 bushels). You may like today’s price but also believe the market will follow its seasonal pattern of moving lower into harvest.

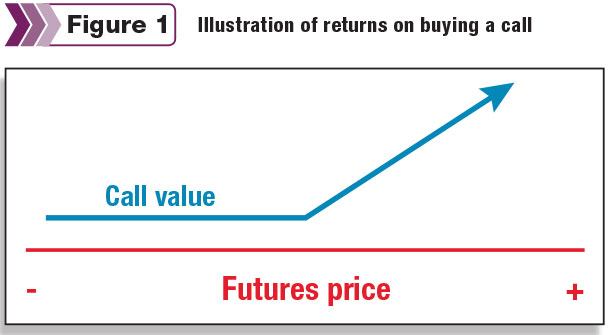

Purchasing a call option is a great way to attend to the market in this scenario. The purchase of the call option gives you the right to buy corn near today’s price. As corn prices rise, the value of the call option will also rise (see Figure 1). This characteristic is what affords you the protection you are seeking against the possibility of higher prices.

Hypothetically, if corn futures were near $3.70, you could purchase the $3.70 call to protect yourself from a rise in prices beyond $3.70. At the same time, you are eligible to participate in falling prices if they should occur. If such a fallout should occur, you will sacrifice the premium you have paid and become the benefactor of lower futures prices.

This is such a powerful tool because while the purchase of the call option may give you the right to buy corn at a certain price, it also gives you the freedom to realize lesser prices if they should become reality. That is the flexibility options give you. It is a very simple yet effective approach best used when markets are outside of what is historically your best opportunity.

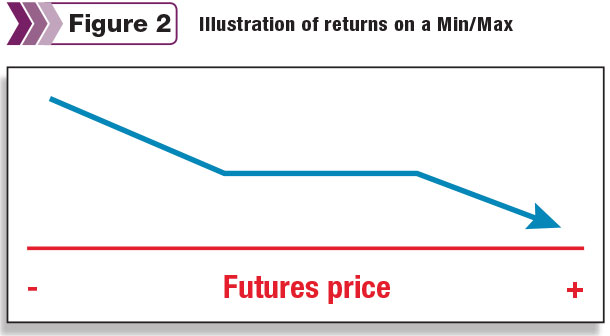

As opportunities become better, you may choose to become more aggressive. One strategy fitting that description is often referred to as a “fence” or “min/max” strategy. In its most basic form, you are simply buying a put then selling the call – or buying the call and selling the put.

Let’s bring this strategy closer to home. Let’s say milk prices are at $21 per cwt for a given period of time. You would like to protect that opportunity while allowing for additional price opportunity that may still exist, but the premium cost to purchase a nearby call is more than you care to initially spend.

You decide to purchase a $20 put for the months in question and sell a $24 call for those same months. The $20 put you purchase establishes the minimum that you receive for your milk in that circumstance. The $24 call you sell establishes the maximum you will receive. The sale of the call allows you to use the premium from its sale to lessen the cost of the put option that is ultimately desired for protection from falling markets.

In exchange for that premium, you are now obligated to offset the difference above the level at which the call is sold ($24 in this case). What should be understood about this position is that you will have to put up a good-faith sum to enter into this position.

We refer to this sum as “margin.” As the market rises, the amount of this requirement also rises. A detailed discussion about this process should be had with your adviser before entering into such a position. This discussion is important to help you budget the necessary cash flow for maintenance of the position.

In this example, if milk prices should end up at a price above the current $21 and less than the maximum price of $24, the producer will be the benefactor of a higher pay price for their milk. If prices should cascade lower to levels below the $20 put that was purchased, the producer will be guaranteed the minimum $20 per cwt established by purchasing the put.

This strategy provides a tremendous amount of flexibility in a market whose bias suggests lower values while history and volatility still allow for higher values. However, this strategy is not a silver bullet. If cash flow is tight and capital is unavailable, you should consider a different strategy.

These are just two strategies among dozens used in today’s markets. As puts and calls are mixed and matched, they provide users the opportunity to create flexibility that individually matches the constraints unique to their operation with the opportunities being presented in ever-fluctuating markets.

In a world filled with abundant uncertainty, constant volatility and ongoing opportunities, options take center stage as a tool that offers opportunity to their users.

Let this brief read give you a baseline understanding of how they work. However, there are countless resources available to help you grow your understanding. Seek them out and ask the tough questions. As you do, you will discover the vast amount of value options play in your risk management efforts. PD

For nearly 20 years, Mike North has educated and guided dairymen and farmers in their efforts to manage commodity price risk.

-

Mike North

- President

- Commodity Risk Management Group