Tax law changes have been numerous in 2010, so it seems appropriate that the year closed out with one more. On December 17, 2010, President Obama signed into law the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010 that includes the highly anticipated extension of the Bush-era tax cuts. There was much debate on whether the favorable individual income tax rates should be extended for everyone, or for everyone except the “rich.” Ultimately the rates in effect in recent years (10 percent, 15 percent, 25 percent, 28 percent, 33 percent, and 35 percent) will stay in effect for two years for all individual taxpayers.

Additionally, the lower rates for long-term capital gains and qualified dividends, 0 percent for individuals in the 10 percent and 15 percent income tax brackets and 15 percent for everyone else, remain in effect. But remember, this is only a two-year extension of these rates and not a permanent change.

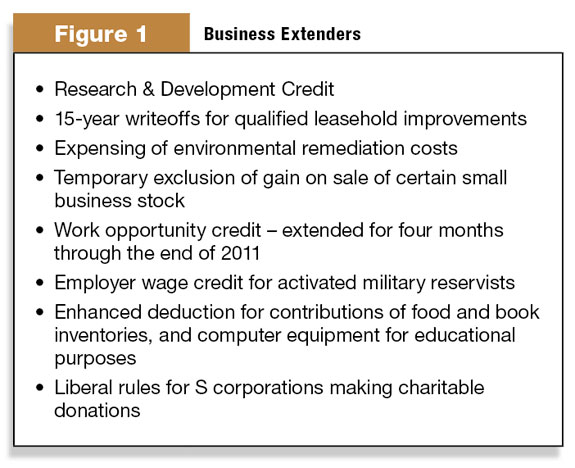

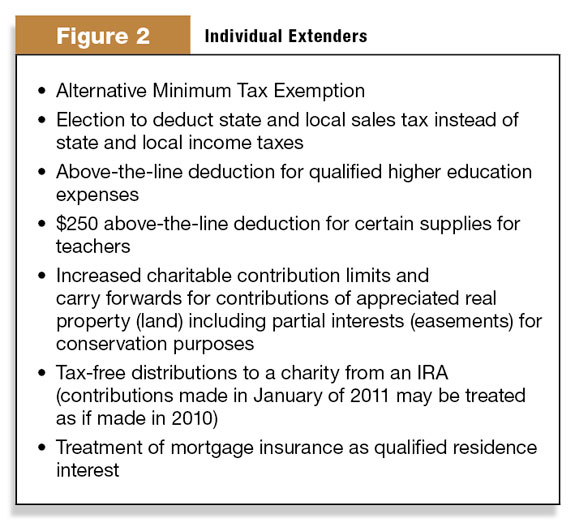

In addition to the extension of the lower individual tax brackets, the new law retroactively reinstates and extends through 2011 a number of individual and business tax breaks which had expired at the end of 2009. See the “Business and Individual Extenders” for a quick reference of a number of these extensions.

Earlier this year, we saw an increase in the amount of equipment and capital costs that small businesses could elect to write off in the year acquired. For property acquired in 2010 and 2011, the annual limit allowed as a write-off is $500,000 with a phaseout of this amount when total purchases exceed $2 million.

Note that property eligible for this deduction can be new or used. As with the other items in the new law, come 2013 the benefits of this deduction are set to diminish greatly.

The new law expands and extends additional first-year depreciation, commonly called bonus depreciation. Bonus depreciation is available for new property (i.e. the original use begins with the taxpayer) that has a recoverable period of 20 years or less (note all farming property will fall under this category), is computer software, or is qualified leasehold improvement property.

Under the new law, 100 percent of the purchase price of new equipment and machinery acquired and placed in service after September 8, 2010, and before December 31, 2011, can be deducted. For new property placed in service during 2012, 50 percent first-year bonus depreciation is available, similar to the rules for new assets acquired before September 8, 2010.

One of the more unexpected provisions of the new law is the one-year payroll tax reduction. Under this new provision, Employee Social Security payroll tax is reduced by two percentage points during 2011.

For an individual with wages of $60,000, this amounts to $1,200 in savings. If the individual is paid twice a month, this equates to an extra $50 in his or her paycheck starting in January.

The employer’s share of Social Security tax is not affected; it remains at 6.2 percent. Self-employed workers, such as many farmers, will also benefit from the reduction; self-employment taxes will be cut from 12.4 percent to 10.4 percent during 2011.

A provision of the new law that was the center of a great deal of debate between Democrats and Republicans is the return of the estate tax. Historically the estate tax rate was 55 percent with an exemption amount of $1 million. The estate tax rate fell from 55 percent in 2001 to 45 percent from 2007 through 2009 and the exemption amount increased to $3.5 million throughout those years.

In 2010, the estate tax was repealed. Prior to the enactment of the new law, the estate tax would have returned in 2011 at a tax rate of 55 percent on taxable estates valued over $1 million.

The new law reduces the estate tax rate to 35 percent for 2011 and 2012 and increases the exemption amount to $5 million per individual. At these levels, the vast majority of estates will not be subject to any federal estate tax.

Additionally, the new law gives heirs of decedents dying in 2010 a choice to apply either the 2010 or the 2011 estate tax rules. At first glance it may seem odd to elect the 2011 rules for 2010; however, as part of the repeal of the estate tax in 2010, the ability for heirs to receive a “step-up” in tax basis was also removed. The lack of the step-up could lead to a significant income tax burden for heirs who sell highly appreciated assets received from an estate in 2010.

Under the 2011 rules, by contrast, the tax basis would be stepped-up to the price of the asset at the date of death. While most heirs would choose the 2011 rules, the heirs of super-rich decedents may find the 2010 rules more advantageous.

A reprieve from higher tax rates, for both individuals and estates, has been granted. However, as with most of the provision of the new law, the reprieve is short. Come 2012, and the next major election cycle, individual tax rates, the estate tax, and all of the other extenders will once again become highly charged topics. PD

Paul Campbell

Tax Officer

Jones Simkins

pcampbell@jones-simkins.com