The emphasis in California switched from dealing with the drought to managing too much water, at least in the short term, with heavy rainfall and flooding to start the year. That impacted everything from dairy cows and facilities to hay storage and movement.

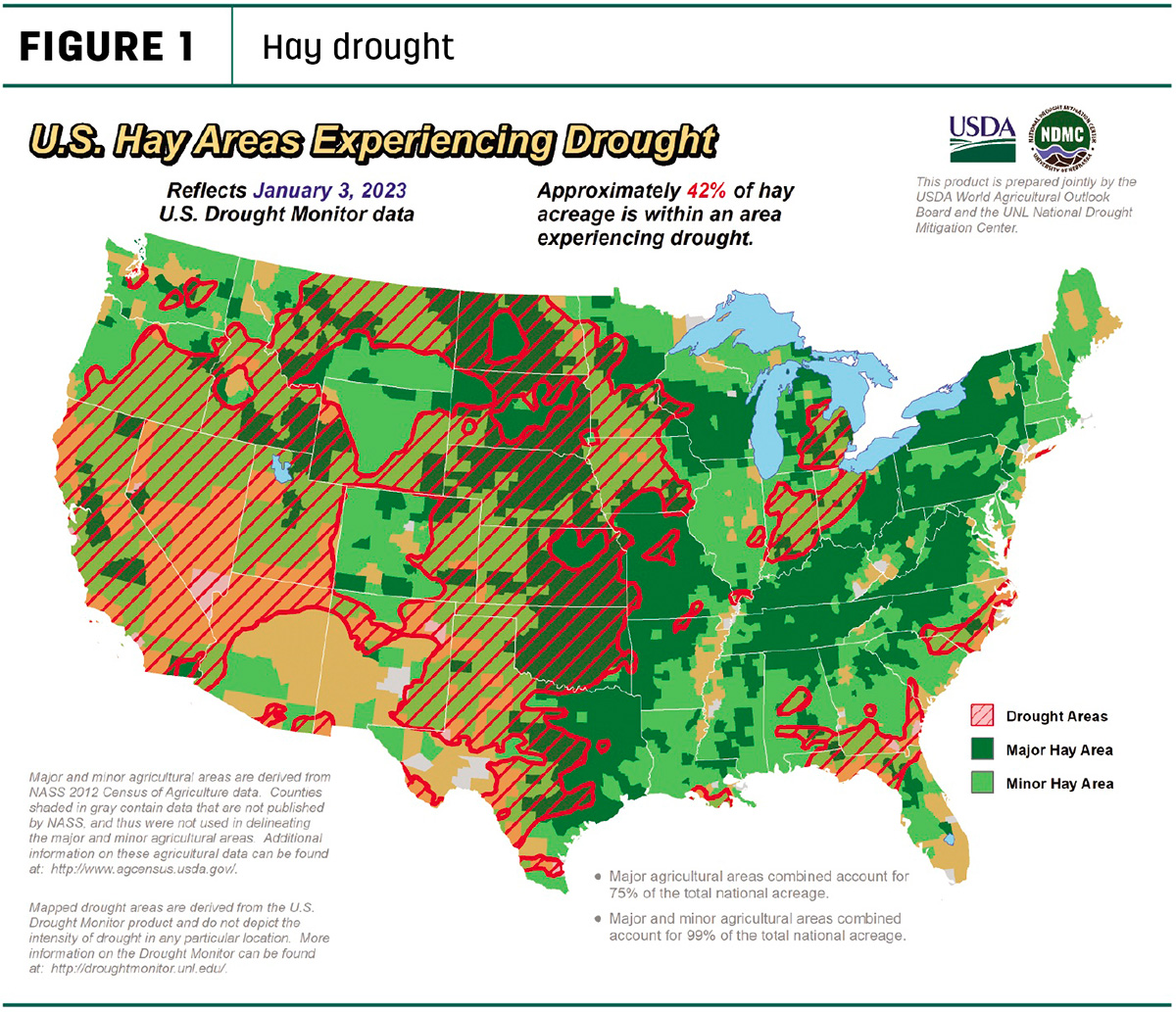

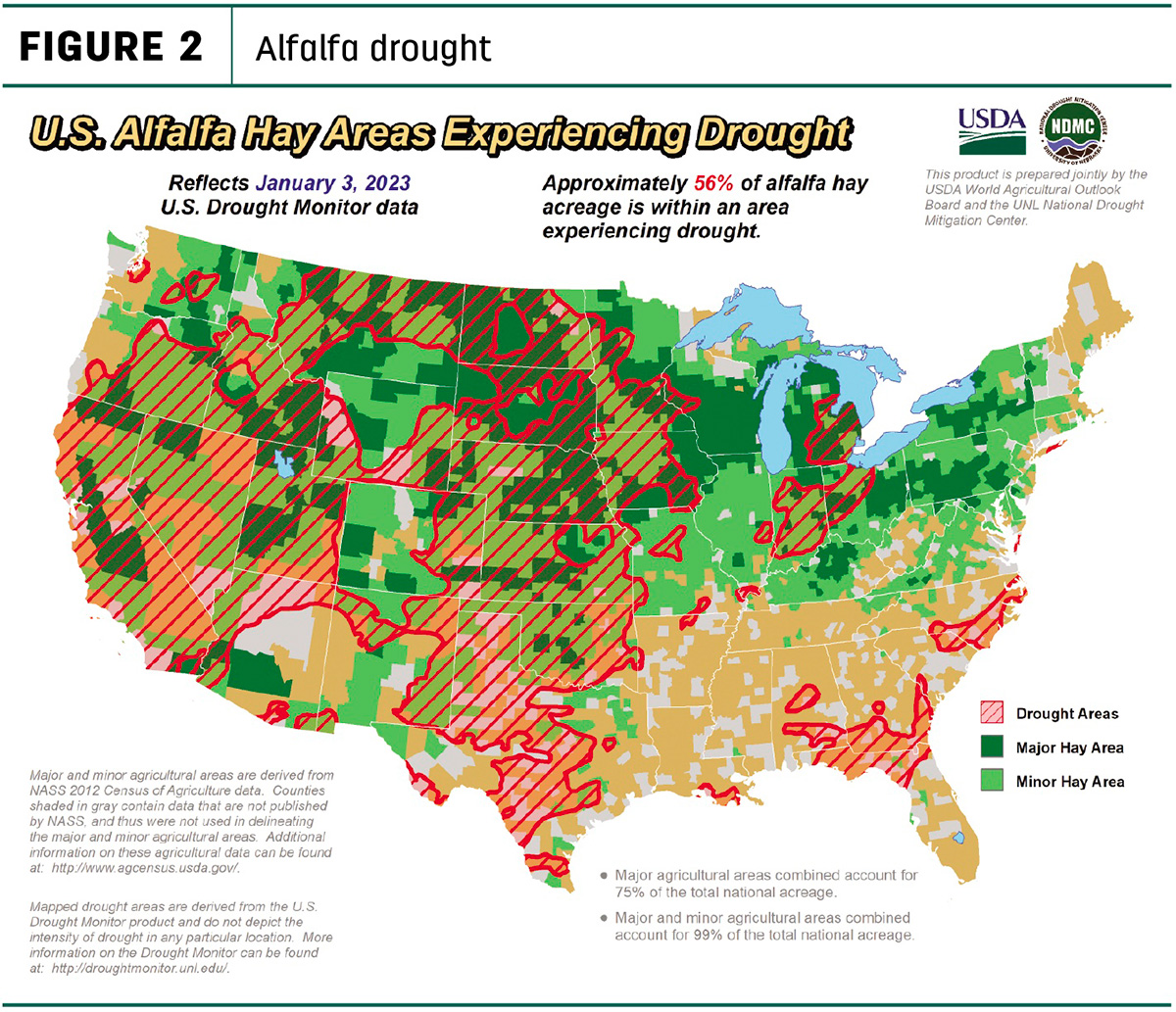

Early January U.S. Drought Monitor maps haven’t captured the full impact of that rain, but overall moisture conditions improved somewhat over the previous month, primarily in parts of Texas and the Pacific Northwest. As of Jan. 3, about 42% of U.S. hay-producing acreage (Figure 1) was considered under drought conditions, 14% less than a month earlier. The area of drought-impacted alfalfa acreage (Figure 2) was down 9%, to 56%.

Hay prices tracked

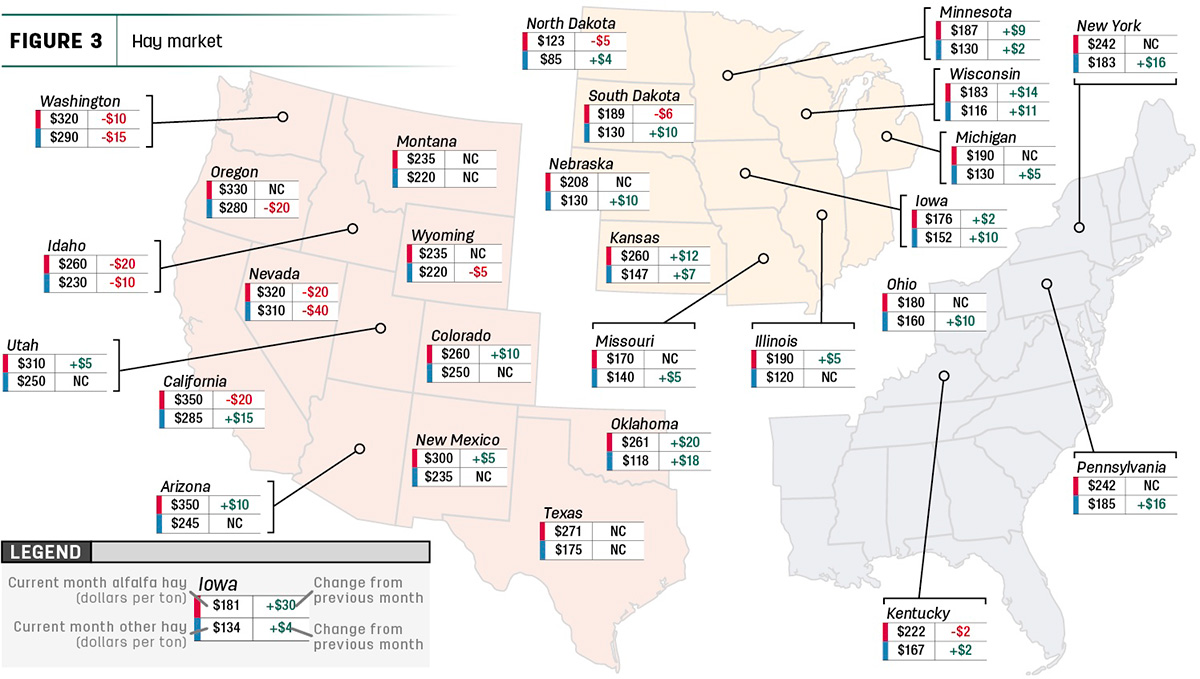

Price data for 27 major hay-producing states is mapped in Figure 3, illustrating the most recent monthly average price and one-month change. The lag in USDA price reports and price averaging across several quality grades of hay may not always capture current markets, so check individual market reports elsewhere in Progressive Forage.

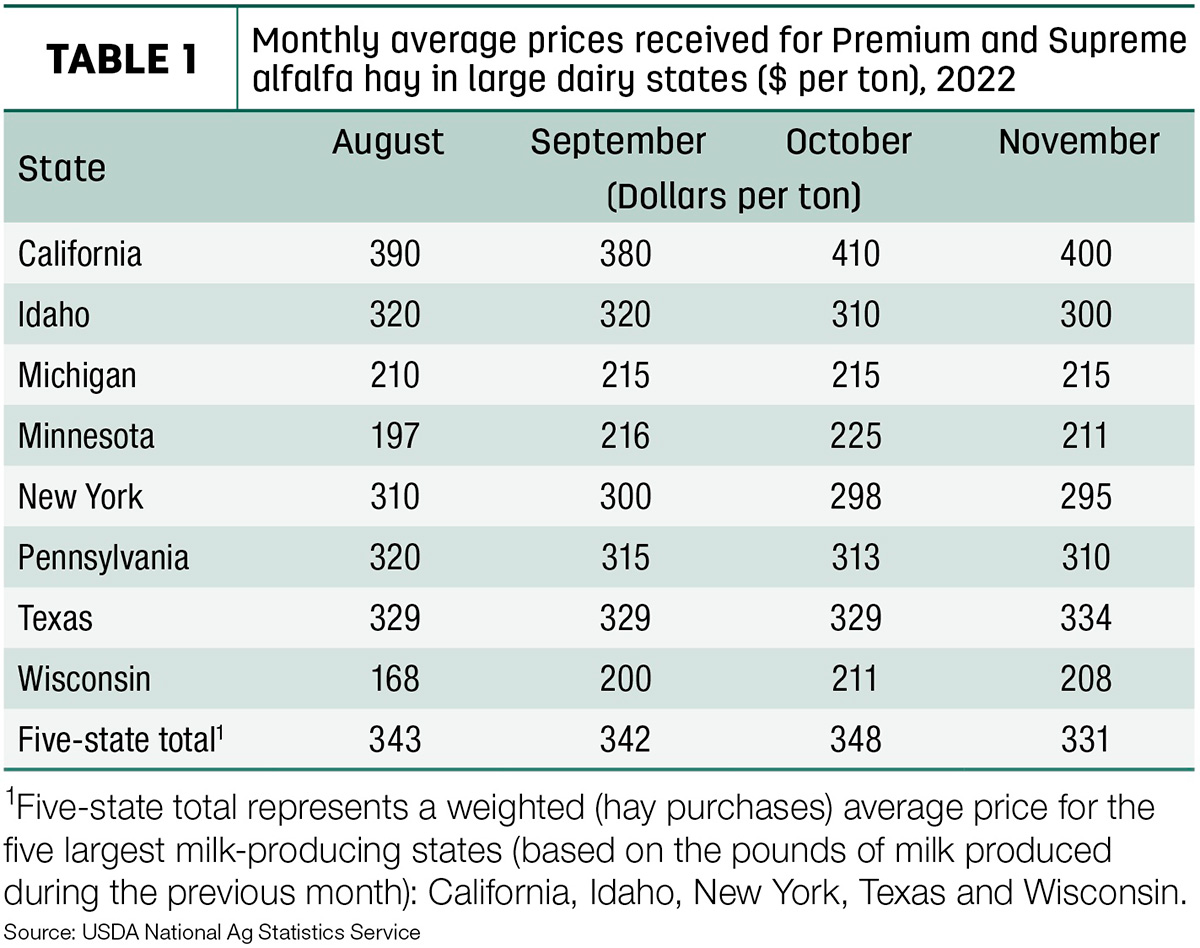

Dairy hay

At $331 per ton, November’s average price for Premium and Supreme alfalfa hay in the top milk-producing states declined $17 from October, the lowest average since June but still $85 higher than a year ago (Table 1). Only Texas posted an increase compared to a month earlier, with prices unchanged in Michigan.

Alfalfa

With lower prices for dairy-quality alfalfa hay, the U.S. average price for all alfalfa hay fell $14 in November to $267 per ton. Prices increased in 10 of 27 major forage states, led by a $20 increase in Oklahoma. Prices were lower in seven states, with California, Idaho and Nevada down $20.

Year-over-year prices were up $100 or more in Arizona, California and Nevada.

The spread between U.S. average alfalfa and other hay prices fell to about $85 per ton in November, the narrowest since March 2022.

Other hay

At $182 per ton, the November 2022 U.S. average price for other hay was up $2 per ton from October. Prices increased in 15 of 27 major hay-producing states, with largest month-to-month increases in Oklahoma, New York, Pennsylvania and California. Average prices for other hay were $100 more than a year ago in California and Nevada, and up $27 nationally.

Hay exports remain slower

At 226,113 metric tons (MT), November alfalfa hay exports picked up slightly from October but were still the third-lowest monthly total of the year.

Increased sales to Japan, Saudi Arabia, South Korea and Taiwan offset a 20,000 MT decline to China, where sales hit a six-month low. At 128,340 MT, sales to China represented 58% of all alfalfa hay exports in November.

Demand for other U.S. alfalfa products was mixed. At 4,118 MT, November exports of dehydrated alfalfa cubes rebounded slightly from a 13-year low in October. Exports of dehydrated alfalfa meal came off a 37-month low at 1,771 MT.

Export volume for other hay hit a five-month high in November but remained well below historical levels. Foreign sales totaled 89,948 MT, up about 3,000 MT from the month before. At 55,830 MT, November sales to Japan were the highest since June and represented about 62% of the monthly total. Albeit a small increase, sales of other hay to South Korea were the highest in three months.

Regional markets

Due to the holidays, some regional hay market summaries were not available at Progressive Forage’s deadline. Here’s a limited snapshot of regional markets to start January:

- Southwest: In Texas, hay prices remained firm in all regions to end 2022. Hay demand was very good. Supplemental feeding was taking place due to limited or short winter grazing.

In Oklahoma, hay trade was light during the holiday weeks.

In California, trade activity and demand were slow to end 2022; export and dairy hay demand were light.

- Northwest: In Montana, hay sold mostly steady to $10 higher. Demand was mostly good to very good for light offerings. Hay supplies had tightened significantly. The cold spell that hit before Christmas forced many ranchers to use up more hay than anticipated.

In Idaho, high testing and retail hay remained in good demand with steady prices.

In Colorado, late-December trade activity was moderate on good demand for horse hay, with market prices mostly steady.

In the Columbia Basin, exporters were dealing with the upcoming Chinese New Year, making export trade very slow. Domestic hay sales remain steady with good demand.

In Wyoming, most bales of hay sold steady, with instances $30 higher on small square bales of alfalfa. Demand was good.

- Midwest: In Nebraska, livestock owners were feeding up their hay supplies earlier than they wanted. Most hay contacts stated their phone was busy this first week of the new year.

In Kansas, demand to end the year remained strong and prices strengthened. Producers and brokers reported that there is a lot of hay moving.

In South Dakota, prices remained steady to firm with very good demand for all classes of hay. Cold weather prevented some hay movement.

In Missouri, following the deep freeze just prior to Christmas, weather conditions turned pleasant, with beneficial rainfall. Quite a bit of hay was moving around the state, both locally on small trailers and some longer distances by the semi loads. The supply of hay is light to moderate, demand is moderate, and prices are mostly steady.

In Iowa, the market overall sold weak on a very light test.

In Wisconsin, prices for dairy-quality hay were steady. Overall forage supplies were good, but lower-quality hay was discounted.

- East: In Pennsylvania, alfalfa and alfalfa-grass blends sold higher. Buyer attendance was moderate, with moderate demand overall on a light to moderate sale supply.

In Alabama, trade was moderate on light supply and moderate demand.

Other things we’re seeing

- Dairy: November’s U.S. average milk price declined but not as much as average feed costs, boosting monthly dairy producer milk income margins ever so slightly. November 2022 U.S. milk production was up about 1.3% from a year ago, with continued slow growth in cow numbers and a small increase in milk output per cow being contributing factors. Preliminary November 2022 U.S. cow numbers were estimated at 9.42 million head, up 38,000 from a year ago.

- Cattle: Cattle and calves on feed in the largest U.S. feedlots (1,000 head or more) totaled 11.7 million head on Dec. 1, 2022, 3% less than a year earlier. Placements in feedlots during November totaled 1.93 million head, 2% below 2021.

Despite high cattle prices, analysis by Purdue University’s Michael Langemeier indicates “feeding cost of gain” factors resulted in 2022 average cattle finishing losses to be approximately $70 per head. Current breakeven and fed cattle price projections suggest that the cattle finishing sector will experience net losses in the first half of 2023.

- Fuel: The U.S. Energy Information Administration (EIA) said the U.S. retail price for regular-grade gasoline averaged $3.95 per gallon in 2022. The price hit its high point for the year at $5.01 per gallon in June before decreasing to $3.09 per gallon at the end of the year.

The U.S. average price for gasoline was $3.22 per gallon on Jan. 2, up 13 cents from the week before but 6 cents less than the corresponding date a year earlier, according to the EIA.

The average U.S. on-highway price of diesel was $4.58 per gallon as of Jan. 2, about 4 cents per gallon above the prior week and about 10 cents more than early January 2022. Unlike crude oil and gasoline prices, the distillate (diesel and fuel oil) price ended the year higher than both January 2022 and its five-year average.

- Trucking: Spot and contract flatbed prices were slightly higher to start the new year, according to DAT Trendlines. The national average spot price was $2.82 per mile, up a nickel from early December but down 59 cents from June. Regionally, average prices per mile were: Southeast – $2.80, Midwest – $3.05, South – $2.76, Northeast – $2.74 and West – $2.40.