Since October 2022, drought conditions have improved for much of the U.S., to the point where U.S. Drought Monitor data notes that less than 24% of the U.S. is under drought conditions. Until February, at least 40% of the U.S. was experiencing some level of drought every week since September 2020. However, a core portion of the U.S. beef herd remains under severe drought conditions in the southern Plains. Although conditions have improved for many producers, the impact lingers.

On May 12, USDA National Agricultural Statistics Service (NASS) estimated hay stocks on farms on May 1 were 13% below those of last year, the lowest in a decade. Despite recent rains, for some producers, the very low hay supplies may not be sufficient to offset poor pastures to sustain herds this summer and allow producers to retain breeding stock to rebuild their herds. As a result, the culling of beef cows continues at a relatively high rate. Based on USDA Agricultural Marketing Service (AMS) reports for weekly slaughter under federal inspection, the pace of monthly beef cow slaughter remains relatively high, despite dropping to below the pace for the last two years in March and April. This has the potential to weaken the outlook for calf crops in late 2023 and 2024, further reducing potential cattle placements year over year in 2024. On the bright side, feed prices are forecast to decline, likely improving returns for producers.

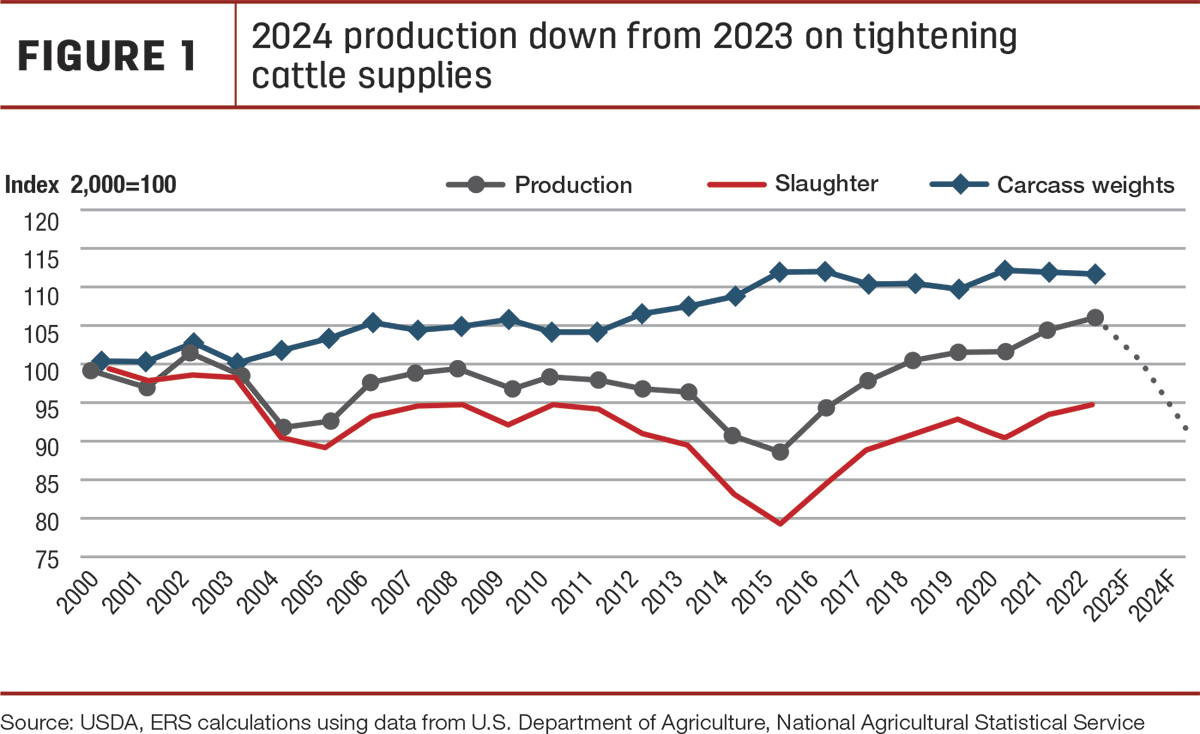

2024 beef production to drop 8% from 2023

The relatively strong pace of beef cow slaughter and relatively large placements of heifers in feedlots in 2022 and into early 2023, will likely yield a smaller year-over-year calf crop in 2023, tightening future cattle supplies. Further, this will likely lead to fewer cows and bulls in the slaughter mix in 2024, as both absolute numbers are lower and – assuming a return to normal pasture conditions – producers hold back animals for herd expansion.

In addition, due to tighter forage supplies heading into summer 2023 and lower feed prices, placements of calves in feedlots are likely to be larger than previously expected, potentially drawing cattle that would have been placed in the first part of 2024. With these anticipated placement patterns and lower expected cow slaughter, 2024 beef production is forecast to decline 8% from 2023 to 24.7 billion pounds.

In Figure 1, annual beef production, cattle slaughter volume and average carcass weights are indexed on the year 2000 to demonstrate the sharp decline after seven years of rising beef production volumes. 2024 will mark the second year of lower production following the record-large volume set in 2022 and will be the lowest production year since 2015 when the sector began to rebuild following the drought of 2011-14.

Although beef imports are forecast to increase and exports are forecast to decline year over year in 2024, lower expected beef production will have a large impact on available domestic disappearance. Total disappearance in 2024 is forecast to be the lowest since 2015, but on a per-capita retail weight basis it is expected to decline year over year by more than 7% to 52.8 pounds. This will be the lowest per-capita beef available domestically since records began in 1970.

2023 beef production raised on higher cattle slaughter

The latest Cattle on Feed report published by USDA NASS, showed the April 1 feedlot inventory at 11.61 million head, over 4% below 12.14 million head in the same month last year. Feedlot net placements in March were less than only 1% lower year over year at 1.93 million head. Although reported placements in March were lower year over year, they did not decline as much as expected. Marketings in March were 1.97 million head, down about 1% year over year. On April 1, the number of cattle on feed over 150 days fell below year-ago levels for the first time this year. However, as a percent of total cattle on feed, this grouping still tops year-ago levels. The unexpectedly high placement levels in March – combined with poor forage and small-grains pastures – suggest an increase in anticipated placements in the second quarter of 2023. This is further supported by higher cumulative feeder and stocker receipts in April and early May 2023 shown in the USDA AMS National Feeder and Stocker Cattle Summary report.

The forecast for second-quarter beef production is little changed from last month, as an increase in expected cow slaughter is more than offset by lower anticipated carcass weights. Third-quarter production forecast is lowered 40 million pounds on a slower pace of fed cattle slaughter and on lower expected average carcass weights, more than offsetting more cows in the slaughter mix. However, in the fourth quarter, the production outlook is higher than last month by 190 million pounds, as more fed cattle are expected to be marketed based on higher first-half placements. In addition, more cows are expected in the slaughter mix, and average carcass weights are lowered. For the year, more fed cattle and cows in the slaughter mix more than offset lower expected carcass weights, raising the outlook for 2023 beef production by 146 million pounds to 26.9 billion pounds.

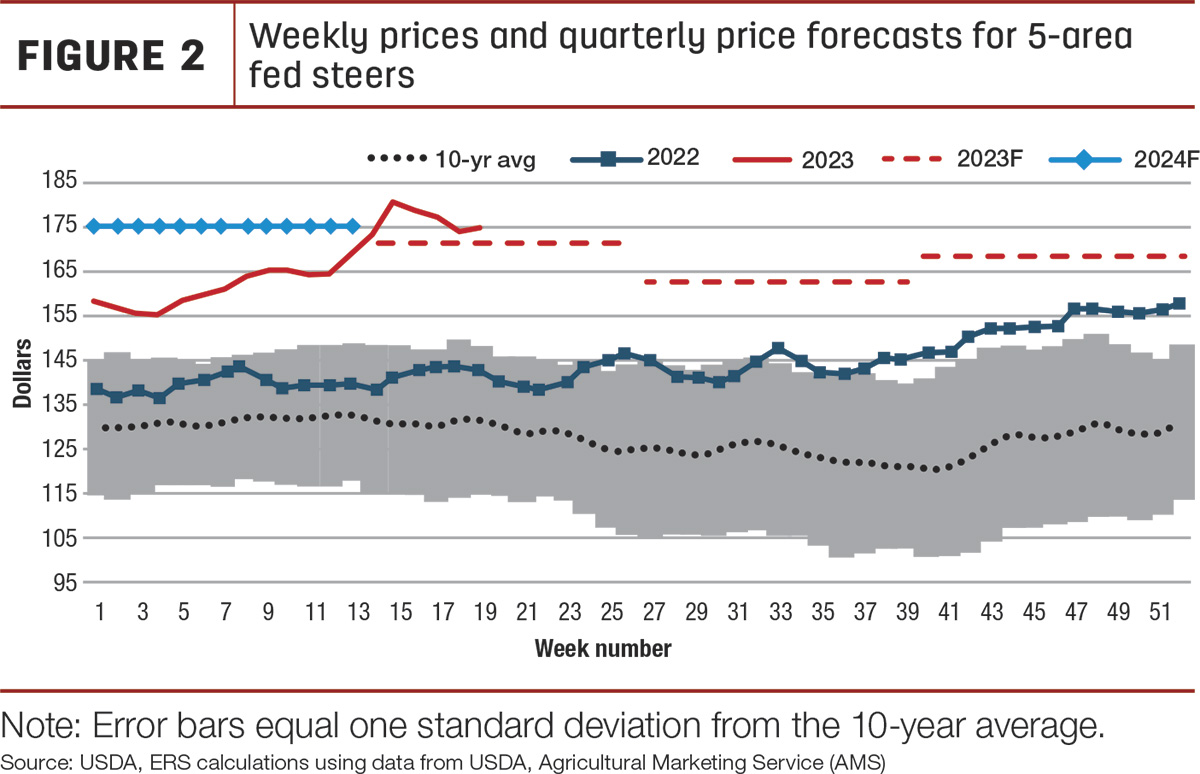

Tighter cattle supplies to push cattle prices higher in 2024

Typically, fed steer prices climb higher in the spring, as demand for slaughter-ready cattle increases from packers looking to fill orders for the impending grilling season. This spring, the reported fed steer prices in the 5-area marketing region for the week ending April 16 (week 14) set a record at $180.44 per hundredweight (cwt), and the month averaged $177 per cwt in April, over $35 above April 2022. The strong move in cattle prices was likely supported by packers trying to fill orders at record wholesale beef prices for the month of April.

Based on recent price data in early May and expected firm demand, the forecast for steers in the 5-area marketing region is raised $3 in the second quarter and $2 in the third and fourth quarters (Figure 2). The annual fed steer price is raised about $2, for a projection of $166.50 per cwt in 2023, which is 15% above last year. In 2024, packers will likely have to bid higher for the shrinking slaughter-ready cattle supply. Prices are projected to average $172 per cwt for the year.

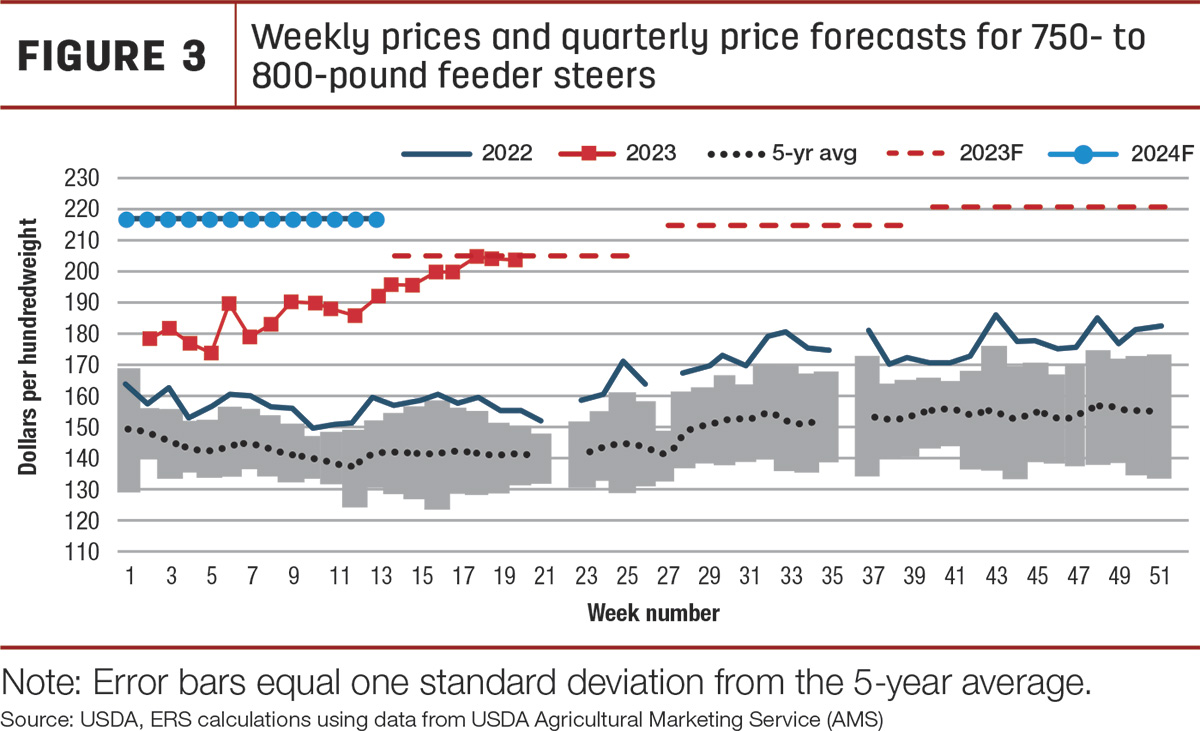

Demand for feeder calves has shown significant strength this spring. In April, the weighted-average price for feeder steers between 750 pounds and 800 pounds at the Oklahoma City National Stockyards was recorded at $198.06 per cwt, almost $40 above April 2022 (Figure 3). The feeder steer price reported on May 8 reached $203.15 per cwt, over $48 above the same week last year. Based on recent price data and declines in forecast corn season average prices, the second-quarter forecast is raised by $5 to $204 per cwt for an annual feeder steer price of $205.40 per cwt, a 24% increase from last year. In 2024, demand for feeder calves will continue, with fewer calves and lower feed input prices for an annual forecast of $221 per cwt, an increase year over year of 7%.

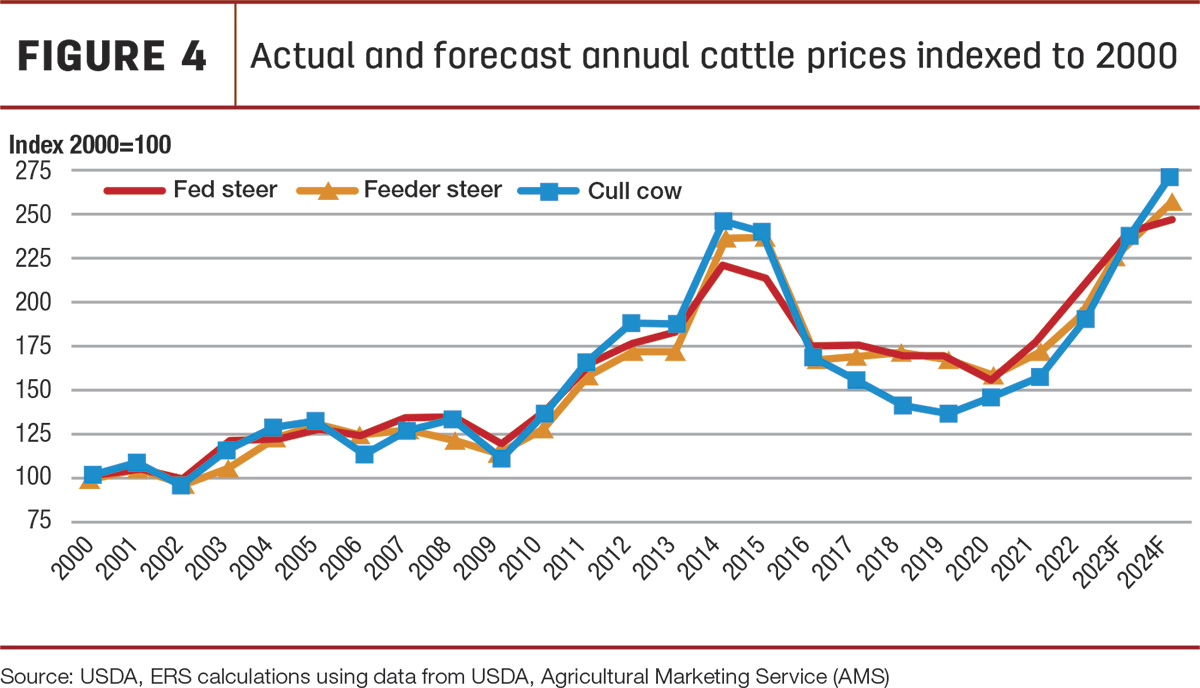

Last, cull cow prices in 2023 are forecast to be $99.20 per cwt, an increase of 26% from 2022. In 2024, a decline in cull cow slaughter is expected to lift prices to $113 per cwt, a year-over-year increase of 13%.

To give perspective on all three price forecasts for 2023 and 2024, Figure 4 is where the actual and forecast annual prices are indexed to prices in 2000. The year 2000 is a good period from which to index, as it is recent and before the major disruptions in the cattle industry in late 2003.

Stronger-than-expected first-quarter exports raise 2023 forecast; exports to continue lower in 2024

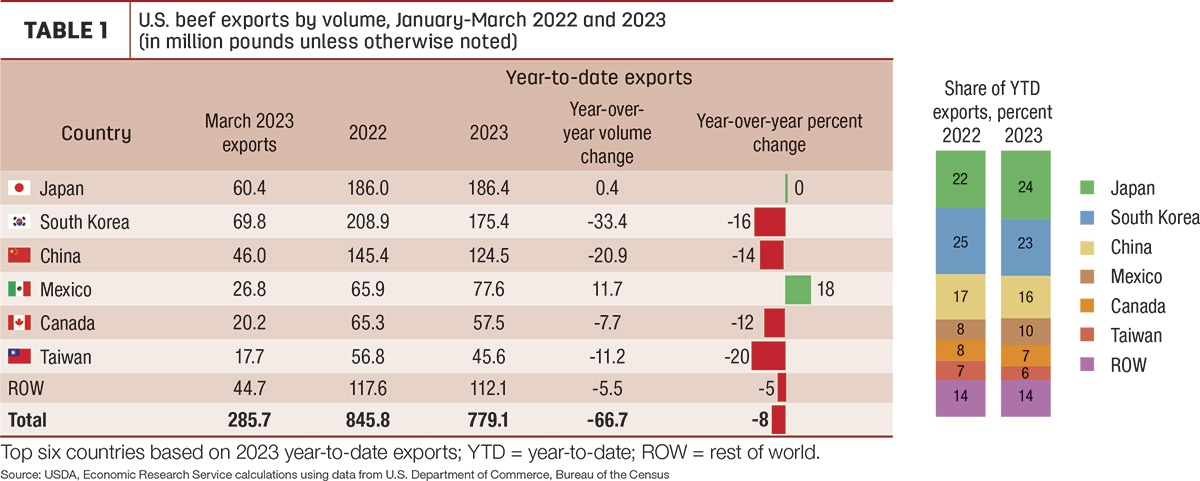

Beef exports in March were 286 million pounds, 6% lower year over year but 4% higher than the five-year average. Monthly exports to Mexico were up 18%, and exports to Hong Kong were more than double the previous year. However, these increases were more than offset by decreases in exports to Canada (-17%), China (-15%) and Japan (-11%).

First-quarter beef exports were 779 million pounds, about 8% lower than last year’s record for the quarter but 2% higher than the five-year average. Table 1 shows that for January through March, only exports to Mexico and Japan increased year over year. Exports to China, while lower year over year, represent a large portion of the increase over the five-year average. Exports to South Korea and Taiwan were also relatively strong compared to previous years, despite the year-over-year decrease from a record quarter last year.

Although lower year over year, first-quarter exports were stronger than earlier anticipated, especially to Asia and Mexico. The forecast for the second quarter of 2023 is raised 40 million pounds to 825 million. This would be significantly lower when compared to last year’s record for the quarter, although slightly higher than the five-year average. The forecasts for the third and fourth quarters are raised 25 million and 10 million pounds, respectively, but are still expected to remain below last year and the five-year average. The annual forecast for 2023 is 3.22 billion pounds, which, if realized, would be a year-over-year decrease of about 9%.

In 2024, beef production is expected to decrease by about 8%. With fewer exportable supplies and higher price levels, U.S. beef will likely be less competitive in the global market. The annual forecast for 2024 is 2.95 billion pounds, which would be a year-over-year decrease of about 9%. The first-quarter forecast is 730 million pounds.

2023 import forecast raised slightly; imports to increase marginally in 2024

Beef imports in March were 308 million pounds, nearly 13% lower year over year. Lower shipments from Brazil, New Zealand and Mexico more than offset slightly higher imports from Canada, Australia and Uruguay. Imports for the quarter totaled 956 million pounds, 3% below a year ago but 22% higher than the five-year average. As shown in Table 2, from January to March only, imports from Canada and Australia have increased year over year. Imports from Brazil have not been as high as last year but are still significantly above the five-year average. The tariff-rate quota under which fresh beef imports from Brazil enter the U.S. was filled for the year as of May 2.

The import forecast for the second quarter of 2023 is raised 20 million pounds to 890 million. The third and fourth quarters are unchanged at 890 million pounds and 765 million pounds, respectively. The annual forecast for 2023 is 3.5 billion pounds, a year-over-year increase of about 3%.

Lower expected production in 2024, especially from lower expected cow slaughter, will increase the need for imports. Greater availability of exportable supplies from Oceania and South America will support a forecast increase in imports of less than 2%, marking the seventh consecutive year-over-year increase, and averaging just below the growth rate from 2018-22. The quarterly import pattern in 2022 and 2023 has been heavily front-loaded in the first and second quarters. This was mostly due to large early shipments from Brazil until the tariff-rate quota was filled for the year. This pattern is expected to continue in 2024; the first-quarter forecast is 960 million pounds.

After two years of beef trade surplus, imports are forecast higher than exports in 2023 and 2024. Over the last few years, the U.S. has alternated between being a net importer and a net exporter of beef. Domestic beef production largely drives the amount of beef exported and imported. With the contraction in beef production forecast in 2023 and 2024, the U.S. is expected to remain a net importer of beef for at least the next couple of years until production is able to expand again.

U.S. cattle import and export forecasts

The U.S. cattle import forecast for 2023 is 1.8 million head, due to a much slower pace of feeder cattle imports from Canada so far this year. The annual forecast for cattle imports in 2024 is 1.95 million head, based on expected demand for feeder and slaughter cattle. The 2023 forecast for cattle exports is 300,000 head, based on stronger exports to Canada so far this year. The annual forecast for cattle exports in 2024 is 200,000 head.