Markets remain steady as the season progresses. Quality is strong where moisture has held, while lighter tonnage in several regions continues to shape a more cautious outlook. Demand stays firm and prices are mostly unchanged, still defined by wide quality spreads and selective buying. Moisture patterns remain uneven, and attention is shifting toward how ongoing weather will influence regrowth, stretch inventories and guide midseason supply expectations.

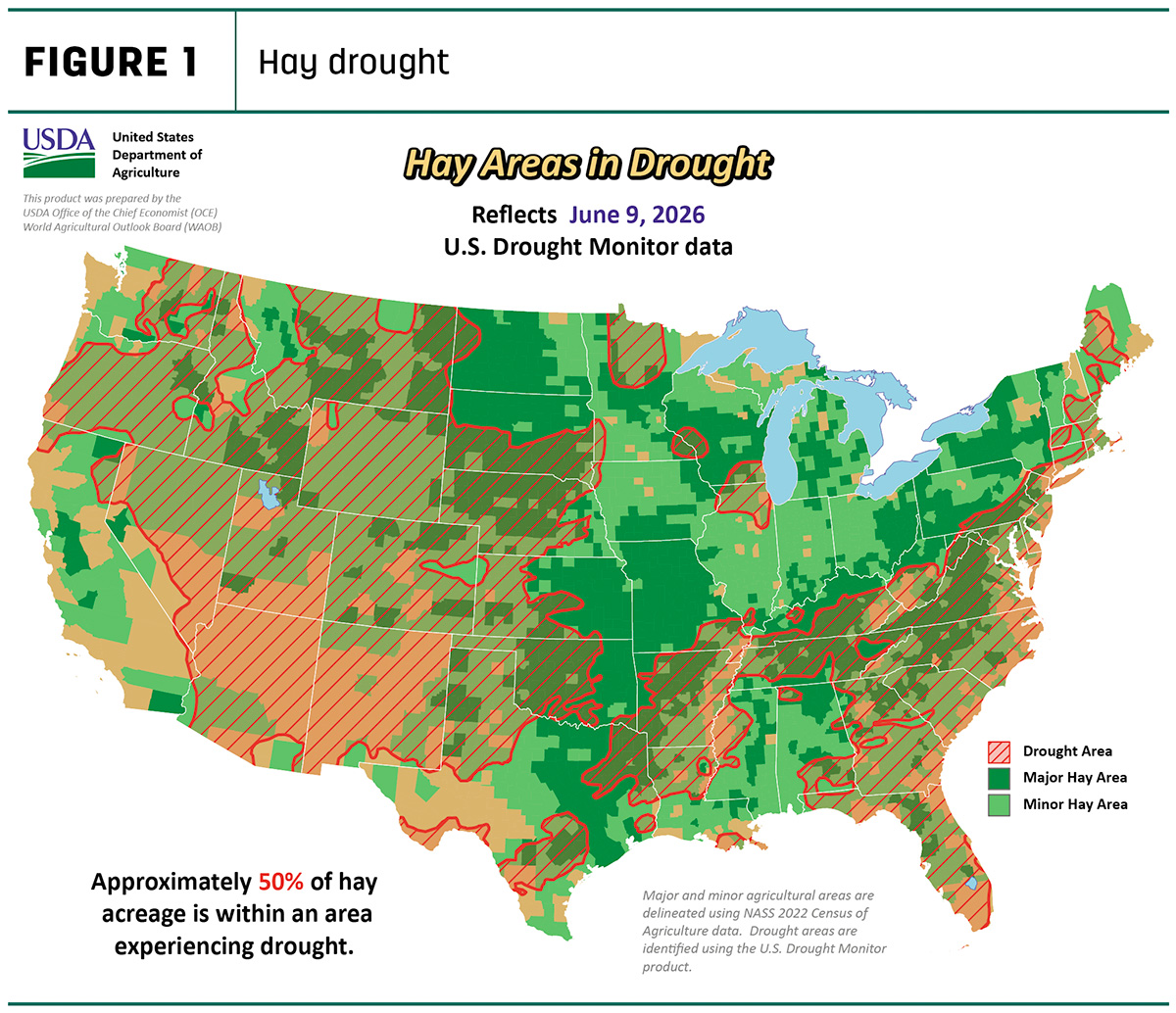

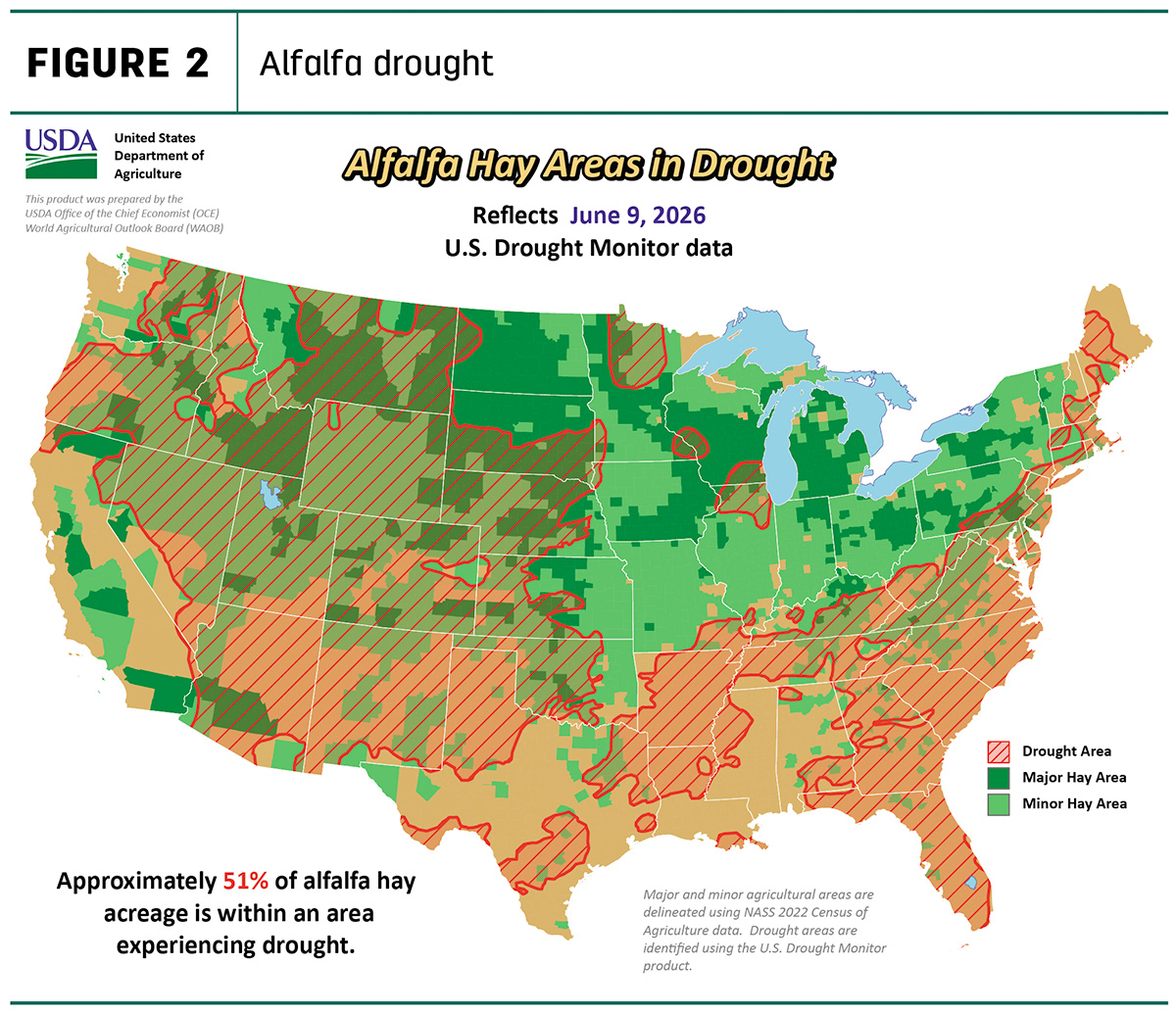

As of June 9, approximately 50% of U.S. hay-producing acreage (Figure 1) was considered under drought conditions, a decrease of 7% from a month earlier. The estimate of alfalfa hay-producing acreage (Figure 2) under drought conditions increased to 51%, 4% more than a month earlier.

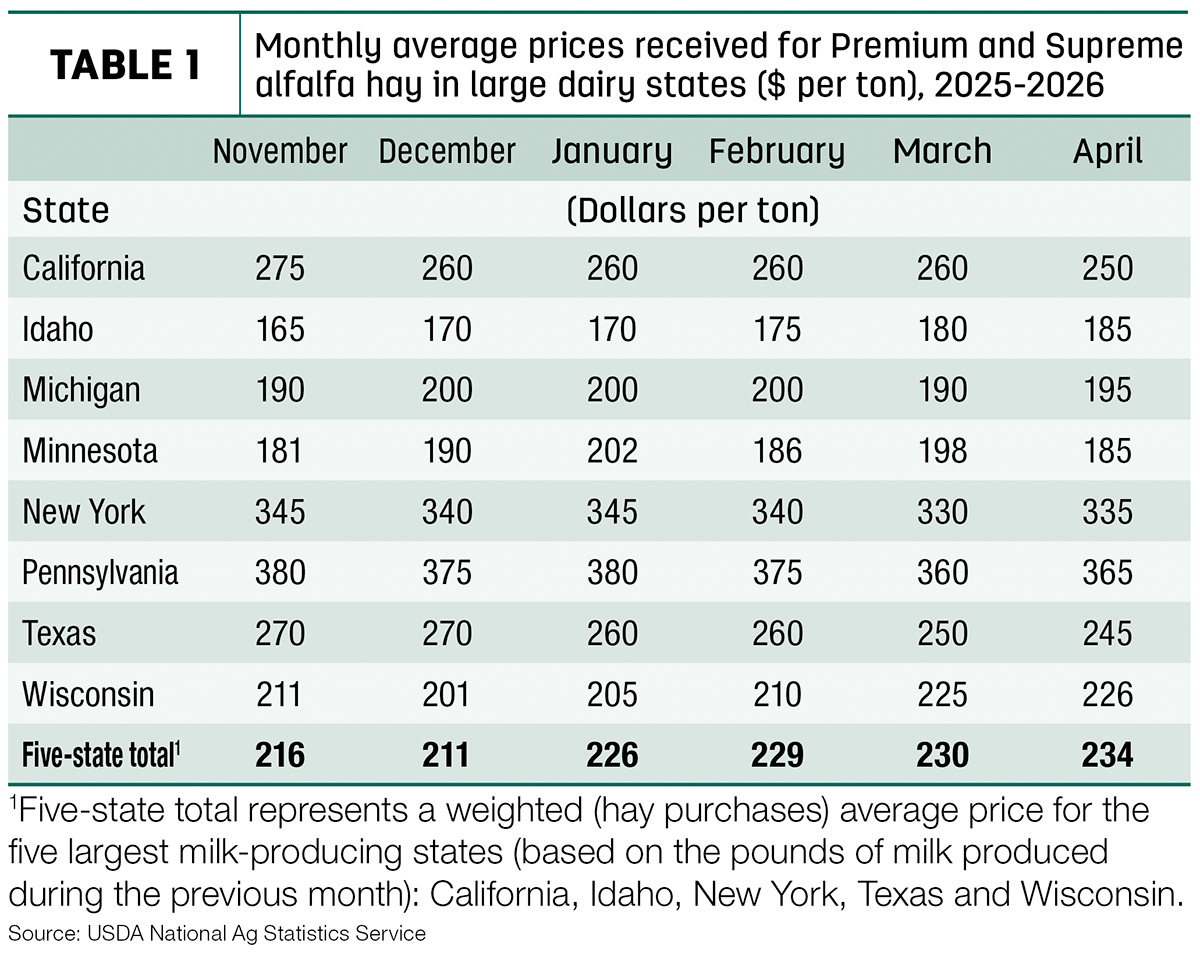

A snapshot of hay prices

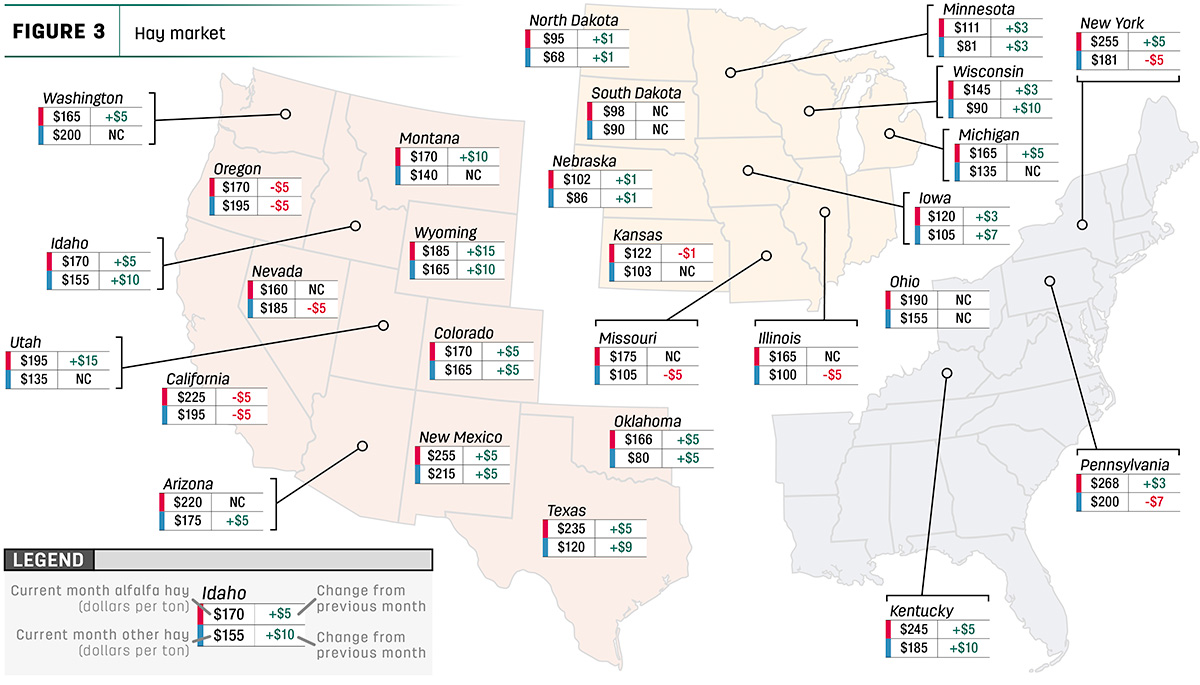

USDA price data for 27 major hay-producing states is mapped in Figure 3, illustrating the most recent monthly average price and one-month change. The lag in USDA price reports and price averaging across several quality grades of hay may not always capture current markets, so check individual market reports elsewhere in Progressive Forage.

Dairy hay

The top milk-producing states reported an average price of $234 per ton for Premium and Supreme alfalfa hay in April 2026, a $4 increase from March 2026 (Table 1). The average price was $18 lower than April 2025.

Alfalfa

The U.S. average price for all alfalfa hay increased $19 in April to $185 per ton. Compared to a month earlier, prices were lower in three of 27 major forage states, with the largest declines in California, Kansas and Oregon. Prices were up in 18 states including Colorado, Idaho, Iowa, Kentucky, Michigan, Minnesota, Montana, Nebraska, New Mexico, New York, North Dakota, Oklahoma, Pennsylvania, Texas, Utah, Washington, Wisconsin and Wyoming.

With few exceptions, year-over-year alfalfa hay prices were down, with the U.S. average about the same compared to April 2025.

Other hay

At $133 per ton, the April 2026 U.S. average price for other hay was down $5 from March. Prices decreased in eight of 27 major hay-producing states, with the largest month-to-month decrease in California, Illinois, Missouri, Nevada, New York, Oregon, Pennsylvania and Utah. Increases were recorded in 13 states including Arizona, Colorado, Idaho, Iowa, Kentucky, Minnesota, Nebraska, New Mexico, North Dakota, Oklahoma, Texas, Wisconsin and Wyoming.

Expanding the timeline, the April 2026 U.S. average price for other hay was $5 less than a year earlier.

The gap between average U.S. alfalfa and other hay prices was about $52 per ton in April.

Exports

April 2026 exports showed little change, with buyers continuing to favor selective, cost‑sensitive purchasing as currency pressure, freight costs and uneven dairy margins limited broader movement. Volumes held close to early‑spring levels, reinforcing a cautious tone as key markets waited for clearer midsummer supply signals. With no major shifts in demand and only modest adjustments in trade flow, exports remained steady but restrained, defined by targeted buying and persistent attention to delivered cost.

At 152,712 metric tons (MT), April alfalfa hay exports increased. China remained the top buyer at 70,729 MT, accounting for about 46% of total shipments. Sales to Japan decreased at 33,140 MT, shipments to South Korea decreased to 23,185 and shipments to Saudi Arabia decreased to 9,445 MT – representing 22%, 15% and 6% of the month’s total, respectively.

Exports of other hay decreased, to 78,069 MT in April. As usual, Japan and South Korea led buyers in the other hay category: Japan purchased 41,228 MT during the month, or about 53% of the total, followed by South Korea’s 24,142 MT, 31% of the total.

U.S. exports of most categories of alfalfa cubes and meal were lower in April, totaling about 9,154 MT. Japan imported about 67% of the total.

Regional markets

Regional hay markets hold steady with early‑season supplies firming and quality driving wider price spreads. Premiums remain selective for top alfalfa, and movement improves slowly as moisture, freight and fuel guide delivered prices into July.

- Midwest: In Nebraska, alfalfa rounds were steady to slightly higher, large squares steady. Ground and delivered hay was mostly steady with firmer tones in the west. Demand stayed strong with slow pasture growth. Yields ran light, with eastern areas edging toward second cutting and much of the west still on first; some producers green‑chopped alfalfa and ryegrass.

In Kansas, recent moisture eased short‑term forage pressure and softened hay demand. Drought categories shifted only slightly, and pasture conditions remain mixed as producers wait for sustained relief.

In Iowa, alfalfa and grass hay trended lower as overall quality slipped. Trade was slow with light to moderate demand and similarly light buyer attendance.

In Missouri, brief haying windows have allowed progress, though yields are running light after late frost and weather stress. Hay demand is light, supplies moderate and prices steady.

In South Dakota, demand stayed strong as drought effects persisted and grass growth lagged. Recent rains helped but left dry pockets, keeping forage pressure high. Grass remained stressed after cold, dry and hot weather, while alfalfa held up better with uneven yields.

- East: In Alabama, hay prices were mostly steady. Trade moderate, with moderate supply and demand.

In Tennessee, hay supplies remain tight, with most old crop gone and trucking shortages limiting incoming loads. Moisture improved in the southwest, but drought persists elsewhere, keeping forage pressure high and pastures mixed.

- Southwest: In California, trade activity is good with very good demand. Export and retail hay demand is good while dairy hay demand is very good.

In Oklahoma, movement remains slow as producers juggle uneven moisture and scattered harvest windows. Conditions vary widely across Oklahoma, with drought, pricing pressure and early‑season uncertainty shaping decisions. Light carryover has pushed some to contract early, while new‑crop grass hay prices remain unsettled.

In Texas, hay prices and demand held steady as wetter weather improved conditions in parts of Texas and eastern Oklahoma.

- Northwest: In Montana, hay prices strengthened on very tight supplies as ranchers bought heavily to cover feed needs. Dry conditions pushed some early cattle sales and spurred producers to secure winter hay. Drought, winterkill and short irrigation seasons are raising concern over summer production.

In Utah, too few sales to set a trend, though tone was firmer. Most old‑crop hay is gone, demand is strong and supplies very light. First cutting is underway after a rough start, with some chopped early. Frost damage and drought are expected to limit yields and tighten summer availability.

In Idaho, demand is steady as new‑crop hay moves, most old crop is gone, and prices are higher. Alfalfa is drawing stronger interest, while drought, low water and frost damage are keeping yields light statewide.

In the Washington-Oregon region, export, dairy and retail new‑crop hay held steady, with good demand as supplies at all levels remain thin. Trade was moderate, with many producers sold out and waiting on shipping and payment, and overall demand remained strong to moderate as many producers are sold out and waiting on shipping or payment.

In Wyoming, a strong demand for uncut hay continues, but producers are hesitant to contract. Weevils are appearing in some western fields, cutting is just starting, and uncertain water supplies point to lighter yields unless rain arrives.

In Colorado, trade was light, but demand stayed strong for old‑ and new‑crop hay. First cutting is underway, and new‑crop prices remain firm under drought pressure and reduced irrigation, which is also increasing prevent‑plant acres.

Other things we’re seeing

- Dairy: Milk output eases slightly under midsummer heat, while northern herds stay steady. Cheese and butter remain firm, but Class III and IV prices show little improvement, keeping margins tight. Export interest holds steady, domestic demand uneven, and producers stay disciplined as summer peaks.

- Cattle: Cattle supplies remain tight, keeping prices supported as feedlot placements stay below last year. Feeder numbers are still limited, moisture uneven and herd rebuilding slow. Cow retention holds, but high costs and heat keep expansion muted, leaving margins tight as summer sets in.

- Fuel: National average fuel prices were significantly higher to start June, according to the U.S. Energy Information Administration (EIA). The U.S. retail price for regular-grade gasoline averaged $4.15 per gallon on June 9, down 15.9 cents from the previous week, $1.04 higher than the same week a year earlier. The average U.S. on-highway price of diesel was $5.21 per gallon, down 14 cents from the prior week and $1.21 more than early June 2025.

- Trucking: Spot flatbed prices were significantly higher to start June, averaging $3.65 per mile nationally, according to DAT Trendlines. Regionally, average spot prices per mile were: Southeast – $4.03, Midwest – $3.73, South – $3.94, Northeast – $3.33 and West – $3.21.

- Other costs: The prices paid index holds steady, with livestock, machinery and fuel costs still elevated. Non‑feed expenses show little relief, keeping margins tight as producers move through midsummer.

- Total feed prices: Total feed costs stay mostly steady, with firm feed grains and complete feeds anchoring the index. Hay, forages and supplements remain soft, and easing energy prices offer only modest relief. Midsummer feeding keeps ration management front and center as producers navigate ongoing cost pressure.

- Interest rates: USDA Farm Service Agency (FSA) interest rates for direct farm operating loans (5%) and direct ownership loans (5.875%) increased for June.