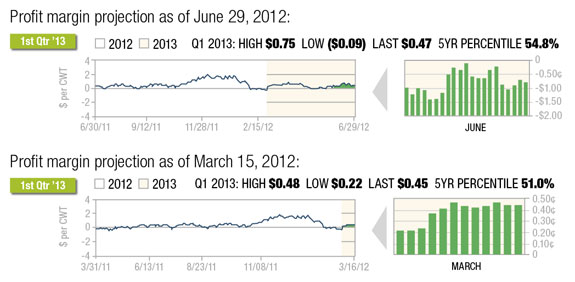

Projected forward profit margins for dairy producers held relatively steady over the past quarter, although that masks some rather extreme volatility in price variation of both feed costs and milk values since March. Margins remain only average for dairy producers through the first half of 2013, although positive all the same. It looks to be a challenging landscape for dairy producers in the second half of the year given the uncertain outlook for feed, with adverse weather across the Corn Belt reducing yield prospects. What once seemed to be a very promising growing season has now been thrown into question.

On a positive note, the recent strength in milk prices has stemmed some concern over the large monthly production figures that were tied to abnormally mild weather this past winter and spring. The accompanying graphs reflect both the current outlook for dairy margins through the second quarter of 2013 as well as comparisons to these same forward profit margin projections back in March.

Milk prices varied greatly over the past few months, dropping more than $2 per hundredweight (cwt) between mid-March and early May, then rebounding by nearly $3 per cwt from early May to late June, as deferred Class III Milk futures posted new contract highs.

Prior to the sharp advance since the beginning of May, milk prices had generally been trending lower through the first four months of the year. The May Milk Production report showed a 2 percent year-over-year gain to 17.625 billion pounds, with the milking cow herd down 4,000 head to 9,270.

That figure represented the first reduction since September 2010, which was encouraging after the last few reports similarly reflected large year-over-year milk production and milking cow herd gains. The prior month showed April milk production at 17.1 billion pounds, up 3.23 percent from 2011 while March milk production was up 4.2 percent from last year at 17.7 billion pounds.

Extremely mild spring weather contributed to the large year-over-year gains in milk production while the weather normalized during May.

Despite the large monthly milk production relative to last year, the cold storage data has generally not been that negative. American cheese stocks on May 31 totaled 623.2 million pounds, down 9.5 million from April and only slightly above a year ago.

Given that stocks normally tend to increase between April and May, with 2007 being the only other exception in recent times, the data suggest better demand and support the firming cheese price trend during June.

The prior month’s data had demonstrated a similar trend as April American cheese production was up 3.3 percent from last year, while stocks as of April 30 were only up 1 percent from a year ago, reflecting stronger demand for cheese as the stocks build failed to keep up with the production increase.

Block and barrel cheese on the CME has come up to around the $1.65-per-lb level by late June from $1.45 to $1.50 back in April and May. Meanwhile, milk production figures may begin to moderate significantly given the strong heat wave that has surged through the central U.S. recently.

The heat appears to be centered over Kansas, with the mercury soaring into the triple digits there and readings well into the ’90s across a broad swath of the Midwest.

Unfortunately, the heat is arriving at a terrible time for this season’s corn crop, particularly as it has been accompanied by drought. Following a fast planting pace and quick emergence, corn crop condition ratings have steadily declined from a record high to a record low for this point in the growing season.

As of July 1, 48 percent of the crop was rated in good-excellent condition, down 8 percent from the week before and down sharply from the 77 percent initial condition reading from NASS on May 20.

Given the quick pace of planting and early development, the crop is also tasseling earlier as it enters its critical reproduction period when yields are determined.

As of July 1, 25 percent of the corn crop was in the silking stage according to NASS. The eastern Corn Belt has missed crucial rainfall in recent storms including a recent weekend when only 0.25 to 0.75 inches of rain fell across 25 percent of the region. Almost one-quarter of the nation’s corn crop is grown in Illinois and Indiana, and conditions are particularly dire in both states.

The USDA released updated acreage figures on June 29, increasing the area planted to corn by 541,000 acres to 96.405 million. Unfortunately, they also reduced the projection for harvested area from 89.1 million to 88.9 million acres.

The reduced harvested area coupled with what will likely be a much-reduced yield forecast from the latest June WASDE estimate of 166 bushels per acre will tighten the new-crop balance sheet significantly from current assumptions.

While it will take a severe yield loss to revert back to a balance sheet as tight as the current season, that scenario is definitely a possibility given the weather right now.It also likely takes away the potential for a move back below $5-per-bushel corn that was previously hoped for by dairymen and livestock feeders.

While there is still time for a change in the weather pattern to improve the outlook for soybeans, declining crop conditions there also suggest a lower yield than what was originally forecast. NASS crop condition ratings as of July 1 show the crop in 45 percent good-excellent condition, down 8 percent from the week before and down from 65 percent projected initially on June 4.

Given that soybeans set pods later in the summer, their yield is yet to be determined and a combination of cooler temperatures and soaking rain between now and then could go a long way to preserve the yield profile of this year’s crop. The USDA currently estimates soybean yield at 43.9 bushels per acre based on the June WASDE .

Another benefit for soybeans is that the acreage base has risen from earlier this spring. The revised acreage forecast from NASS pegged soybean planted area at 76.1 million acres, up 2.2 million from the March Planting Intentions report.

Harvested area is also expected to be up 2.3 million acres to 75.3 million, which will provide some buffer for a reduced yield.

Unlike corn, however, the new-crop balance sheet is already forecast to be precariously tight and a sharply reduced yield on this year’s soybean crop would have profound bullish implications for soybean meal prices given the crop losses this season in South America.

Whatever the outlook for feed costs and milk revenue, dairy margins remain profitable through early 2013, based upon current projections, and there are many different tools dairymen can take advantage of to protect their profitability.

Given that projected forward margins are only about average from a historical perspective, coupled with the fact that feed costs are very high, it is important that producers remain flexible in their strategies to protect these costs.

Option contracts that convey the right without the corresponding obligation to buy corn and soybean meal at a pre-determined price allow for higher costs to be protected while retaining the opportunity to participate in lower prices.

Alternatively, a range of higher prices can be protected for a more limited cost that also would preserve the opportunity to participate in savings should prices eventually come down.

With regard to milk, similar strategies to protect against lower prices would help dairymen in a declining market while preserving the opportunity to participate in further strength should milk continue moving higher.

Here also, a range of lower prices could be protected for a more limited cost – with or without a corresponding obligation to sell above the market.

While option-based strategies involve premiums that represent additional costs to a dairy, one feature to highlight is the added flexibility they provide. This flexibility becomes an advantage in periods of price volatility such as we are now experiencing.

The ability to adjust a strategy over time to capture opportunities that develop allows costs to be minimized such that the impact on the bottom line profit margin is limited.

As mentioned in this column previously, it is important to remember that the markets, by nature, are dynamic and move significantly both up and down over time.

Managing profitability is a function of managing the volatility in forward prices and making periodic changes to strategies in order to take advantage of these swings is a fundamental part of the process.

Learning the various ways to protect margins and mitigate risks on both the revenue and cost sides of the equation will empower you to make more informed decisions about your operation and become a better margin manager. PD

Chip Whalen

Senior Risk Manager and Director of Education

Commodities & Ingredient Hedging LLC