Just over 12 months ago, I reported Xcheque.com’s analysis of the delicate balance of supply and demand in the U.S. market. At that time, the milk price and margin available in the U.S. was at odds with the value of milk commodities in international markets. The conclusion that U.S. milk was undervalued has proved correct with prices rallying and a return to more sustainable margins for most of 2011. So how do things look one year later and what is the prognosis for the rest of 2012? Unfortunately, the current state of the market is an ugly sight and is only going to get worse if you believe that the futures market is a guide.

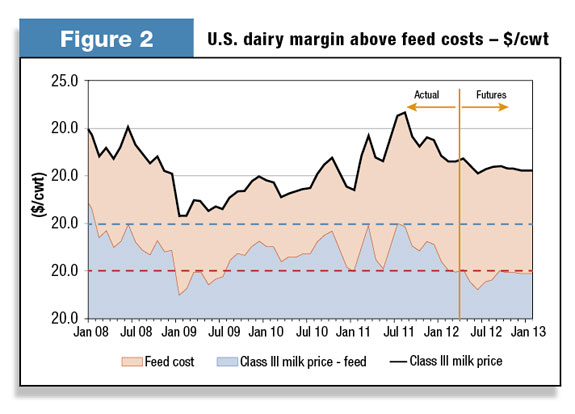

Figure 1 shows our analysis of value of milk flowing to ingredients in the U.S. The black line at the top is the Class III milk price. The pink area shows the cost of a typical feed mix (corn, soybeans, alfalfa). The blue area at the bottom of the chart shows how much money is left over after feed costs – the margin available to pay for all other costs.

The milk price and feed cost used in this chart gives a milk:feed price ratio that is very close to the monthly figure routinely reported by the USDA.

Current margins are down to the critical lower limit of $5 per hundredweight (cwt). Beyond this, the short-term futures for feed and milk price take us back to the depths of 2009 and no sign of a recovery any time soon.

The current state of the market is a consequence of rapid growth of milk production by all the major exporting nations. During 2011, the combined milk production increase of U.S., EU, NZ, Argentina and Australia amounted to 17 billion pounds of milk.

That is almost double the previous year and three times the normal annual growth. In the first three months of 2012, production grew by a further eight billion pounds. Global demand has not been able to keep pace and international commodity prices have fallen steadily, with the fall accelerating in the early part of 2012.

Unlike 2011, the U.S. cannot look to international markets to take stock out of the system at better value than the domestic price offers.

Another year like 2009 doesn’t bear thinking about, but the U.S. milk production data for April has provided a glimmer of hope. It appears that the message to slow down is getting through to U.S. milk producers.

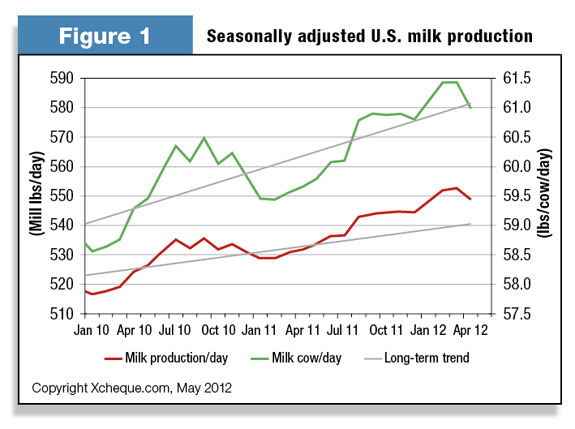

Figure 2 shows Xcheque’s seasonally adjusted milk production trend for the U.S. In this chart, monthly milk production has been corrected for the normal increase and decrease across the year. Also shown is the milk production per cow after adjustment for seasonal effects.

Farmers appear to have responded in the fastest way possible – by turning down feed supply. Cow numbers are slightly up for April but milk production per cow is down almost 1 percent on the peak of the past few months.

The longer-term trends suggest that another 1 percent reduction is readily achievable but, beyond that, cow numbers will need to decrease.

For U.S. dairy farmers, this is good news. 12 months of margins at less than $5 per cwt is completely unsustainable. It is entirely possible that we will see further margin reductions in the next few months, but I can’t believe this will continue in the second half of 2012 and early 2013 (as suggested by the futures prices).

Farmers will keep turning off production until they start to see higher margins in the futures price and their milk checks. The U.S. market is finely tuned on stocks and it doesn’t take much time for a recovery to flow through.

The U.S. production data is also good news for the global dairy industry. Stabilization of U.S. milk production at current levels is necessary to allow time for global dairy demand to catch up. We now need Europe, Argentina, New Zealand and Australia to respond accordingly.

It may, however, take a little longer before the slowdown in those regions becomes evident. The storm surge of reducing commodity and milk prices is only just becoming apparent in Oceania and Europe. Despite a positive turnaround in Fonterra’s June auction results, my prediction is that it will be six months or more before we see a real recovery, with lots more anguish and dramatic news headlines to come.

As the saying goes – one swallow does not a summer make – nevertheless, I am for the moment hanging on to this one piece of positive news and the knowledge that the market can and will (eventually) correct itself. PD

—Excerpts from Xcheque.com

Xcheque provides a unique, independent perspective on the economics of the gloabl dairy supply chain.

Jon Hauser

Director

Xcheque