Role of ranch accounting systems

The new year symbolizes a great opportunity to reflect on ways to improve upon 2020 profitability. Ranch profitability begins with identifying areas of operational inefficiency, and records are a key component in this process. While knowing cost of production is a critical element of any ranch management plan, many ranch managers do not know their true unit cost of production (UCOP). Few ranchers enjoy recordkeeping, but good records support sound management in the face of rising costs, weather uncertainty and volatile markets.

Despite ranches having access to more data than ever before, it remains a challenge for these same ranch managers to turn that data into meaningful information that supports better decision-making.

Setting up a good managerial accounting system is likely the first step towards transforming data into more useful information. This accounting system should have the ability to: (1) determine the general financial health and performance of the business, (2) determine the profit/loss of each enterprise on the ranch and (3) provide valuable information for strategic decision-making. For any ranch that operates as a business, these are significant factors to evaluate as important plans or projections are being discussed.

A managerial approach to ranch recordkeeping

Ranch managers should seek to employ a managerial-accounting approach rather than a cash or taxed-based accounting approach. Managerial accounting strives to develop performance measures that best reflect actual management performance. When utilizing ranch accounting for management purposes, there are three central concepts to consider.

- Transition away from a cash-based accounting system: Cash accounting is typically used for simplicity and the purposes of satisfying tax obligations. However, if expenses are not matched to the year in which the revenues were realized (a system known as accrual accounting), an accurate UCOP is difficult to calculate.

- Consider the non-cash expenses of depreciation and unpaid management: Cash expenses are often the only expenses used by ranch managers when calculating UCOP. Data collected by Colorado State University’s ranch analysis program show depreciation and labor are two of the top three expenses on any given ranch, so it is critical to include these expenses when analyzing ranch financial measures.

- Determine a way to allocate overhead expenses into each enterprise: Allocation schemes can include acres used or animal unit months per enterprise. Allocation schemes can vary depending on the ranch. The key to allocating overhead expenses is consistency.

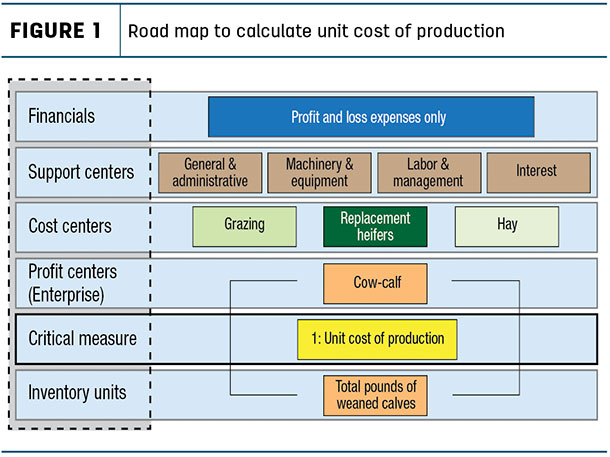

Road map to calculate UCOP

It may be helpful to visualize an effective accounting system in the form of a road map. Figure 1 illustrates a simple setup that could be used to more accurately calculate UCOP.

Let’s quickly review the specific components of an effective record-keeping system, as illustrated in the figure.

- Financials: Expenses should be taken directly from the fiscal year income statement. If the enterprise incurred expenses in the previous fiscal year, those costs are directly assigned as cost of goods sold.

- Support centers: The four support centers listed in the figure are the same for every operation, and they represent the fixed cost structure of the ranch.

- Cost centers: Each operation will identify unique cost centers that support their objectives. In the cow-calf example, cost centers can be as broad as grazing or as narrow as preconditioning. The manager will determine which operational aspects need to be measured closely year over year.

- Profit centers: These are enterprises on the ranch that both accumulate expenses and realize revenue during the fiscal year. Each profit center will record its own net income, which will contribute to the overall ranch net income.

- Critical measure: The objective of this process is to calculate the UCOP. This number is only accurate if appropriate expenses are compared against appropriate inventory units.

- Inventory units: Match appropriate inventory units with selected profit centers. Cow-calf enterprises use pounds of weaned calves as the unit of measure. A hay enterprise would use tons of hay as the inventory unit of measure.

Once the big picture road map is in place, five easy steps can be used to put the new record-keeping system into action.

Step 1: Identify the operation’s profit and cost centers. For cattle operations, this determination should go hand in hand with the various classes of livestock on the ranch.

Step 2: Classify income statement expenses into one of three categories:

- Support centers – fixed costs

- Cost centers – expenses directly incurred by the cost center determined by the ranch

- Profit centers – expenses directly incurred by the enterprise being evaluated

Step 3: Allocate support center (fixed costs) to either a cost or profit center.

Step 4: Transfer cost center expenses into other cost or profit centers.

Step 5: Calculate UCOP by dividing enterprise expenses by inventory units.

Accurate analysis is key

A good analysis starts with good data, which requires a good system. The goal of creating an effective managerial accounting system is to offer the ranch manager accurate data-driven facts that can be utilized to inform decision-making. Quality data allows the manager to evaluate strategic production and financial decisions and more accurately project cash flow and working capital needs. The most powerful output of managerial accounting for beef producers is an accurate UCOP for each enterprise on the ranch.