Progressive Dairy provides monthly online updates of important dates, reports and advice affecting risk management decisions.

High expense costs, further exacerbated by inflationary pressures, have lowered the real value of high milk prices, notes Daniel Munch, economist with the American Farm Bureau Federation. Writing in a recent Market Intel report, Munch said any impending recession could spell additional trouble on the dairy demand front if consumers begin to spend less and go out less, actions that would be compounded by increases in milk production. (Read: Strong dairy prices overshadowed by farm operating expenses.)

“A quick glance at the dairy market’s high prices and decent demand signals might suggest dairy farmers are in good shape,” Munch wrote. “Unfortunately, analyzing milk prices only by comparing their face value over time is futile to understanding the breadth of challenges facing dairy farmers across the country.”

By milk prices alone, the past year or so has gone well for dairy producers, Munch wrote. Between May 2021 and May 2022, the base Class I (fluid milk) price increased by $8.35 (49%), the Class II (soft products like ice cream and yogurt) price increased by $9.65 (59%), Class III (hard cheeses and whey) prices increased by $6.25 (33%), and Class IV (butter and powders) prices increased by $8.83 (55%) per hundredweight (cwt).

According to Munch’s economic analysis, those strong milk prices have largely been dwarfed by increases in production costs. As of May 2022, the average corn feed costs used to calculate the USDA Farm Service Agency’s Dairy Margin Coverage (DMC) program margin was 22% higher than last year ($5.91 per bushel to $7.26 per bushel), the average soybean meal cost was 5% higher ($421 per ton to $441 per ton), and the average blended alfalfa price was 5% more ($210 per ton to $274 per ton).

The average DMC margin (above feed cost margin) between the program’s launch in January 2019 and December 2020 was 52% of the all-milk price. Since December 2020, the DMC margin has come in at 40% of the all-milk price.

“Dairy farmers are keeping proportionally less of their milk check under these periods of high milk prices, revealing the impacts of inflationary price pressures on the value of revenue,” Munch said. “Though the number on the check is higher, its value and buying power in the broader market has weakened.”

Record-high milk prices did offset higher feed costs in May, improving monthly dairy producer milk income over feed cost (IOFC) margins calculated under DMC. The May DMC margin was $12.51 per cwt, the highest since November 2014. (Read: May DMC margin hits $12.51 per cwt.)

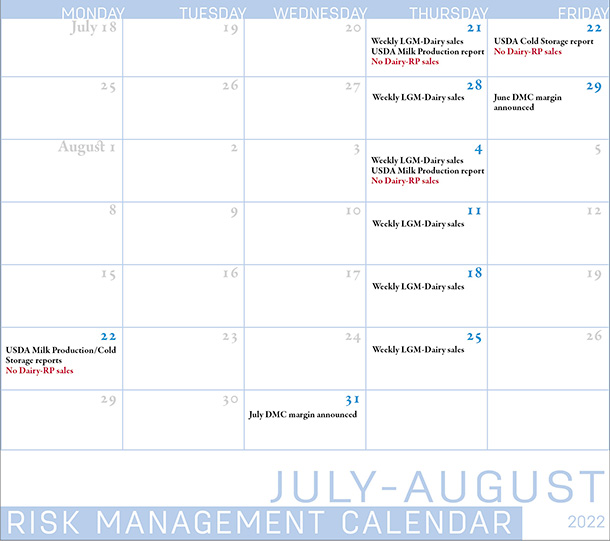

June’s DMC margin will be announced on July 29. As of July 14, the DMC decision tool forecast a margin of about $11.54 per cwt, down nearly $1 from May.

Dairy-RP, LGM-Dairy policy reminders

In addition to DMC, other risk management tools include Dairy Revenue Protection (Dairy-RP) and Livestock Gross Margin (LGM-Dairy), subsidized margin insurance programs administered by the USDA’s Risk Management Agency.

At any one time, Dairy-RP sales are open for as many as five future quarters. Sales close 15 days before the beginning of the quarter. For example, the period to purchase Dairy-RP coverage for the fourth quarter of 2022 closes on Sept. 15. The market changes daily, and Dairy-RP endorsements must be purchased between the Chicago Mercantile Exchange (CME) market closing and the next CME opening.

Dairy-RP coverage cannot be purchased on days when major USDA dairy reports that could impact markets, including Milk Production, Cold Storage and Dairy Product reports (see Calendar). Dairy-RP is also not available on days when applicable futures contracts move limit-up or limit-down, or on days when CME trading is closed due to holidays.

Click here or on the calendar above to view it at full size in a new window.

LGM-Dairy provides protection when feed costs rise or milk prices drop and can be tailored to any size farm. LGM-Dairy uses futures prices for corn, soybean meal and milk to determine the expected gross margin and the actual gross margin. LGM Dairy is similar to buying both a call option to limit higher feed costs and a put option to set a floor on milk prices.

Coverage can be purchased on expected milk marketings over a rolling 11-month insurance period. For example, the insurance period for the Jan. 29 sales closing date contains the months of February through December. Coverage begins the second month of the insurance period, so the coverage period for this example is March through December.

Sales periods for the LGM-Dairy program are open on a weekly basis. Unlike Dairy-RP, LGM-Dairy is available even if a sales period falls on the day of a USDA report.

June uniform prices announced

Administrators of the 11 Federal Milk Marketing Orders (FMMOs) reported June 2022 uniform milk prices, producer price differentials (PPDs) and milk pooling data, July 11-13. As expected, uniform or blend prices inched higher in most FMMOs, while the wide spread between Class III-IV milk prices affected pooling. For a look at Progressive Dairy’s monthly review of the numbers to provide some additional transparency on your milk check, read: Most June FMMO uniform prices inch higher but Class IV pool shrinks.

USDA milk production report, outlook

Monthly U.S. milk production was below year-ago levels for a fifth consecutive month in May, with slow growth in milk per cow and cow numbers well below last year’s peak. (Read: May 2022 milk production remains below year-earlier levels.)

The USDA’s preliminary May milk production estimate will be released July 21. Check the Progressive Dairy website late that day for a summary.

The USDA’s monthly World Ag Supply and Demand Estimates (WASDE) report, released July 12, 2022, again revised the 2022-23 U.S. milk production estimates lower due to slower growth in milk per cow. (Read: Weekly Digest: USDA cuts 2022-23 milk production forecasts, raises 2023 price projections.)

Despite the outlook for production lowered in 2022, projected farm-level milk prices were steady to slightly lower for 2022 but raised for 2023 when compared to last month’s price projections.

Since that outlook, however, milk futures prices have weakened somewhat, and are well below USDA price projects for both 2022 and 2023.

The USDA’s WASDE report projected 2022 annual average Class III price at $22.80 per cwt. The projected Class IV price was $24.70 per cwt, with 2022 all-milk price forecast at $26.15 per cwt. Annual average price projects for 2023 were: Class III – $20.85 per cwt, Class IV – $22.30 per cwt and all-milk – $24.15 per cwt.

At the close of CME trading on July 18, Class III prices for the second half of 2022 average $21.01 per cwt, for an annual average of $21.98 per cwt. Class IV futures prices for the second half of 2022 averaged $23.45 per cwt, yielding an annual average of $24.06 per cwt.

Based on futures prices as of July 18, Class III prices would average $19.24 per cwt in 2023, with Class IV prices averaging $19.95 per cwt.

Other resources

- Zach Myers, risk education manager with the Pennsylvania Center for Dairy Excellence (CDE), will host the next “Protecting Your Profits” webinar, July 27, 12-1 p.m. (Eastern time).

Myers will highlight the latest Class III and IV futures milk price forecasts and share updates on DMC margins and the Dairy-RP program. The event will also feature Beverly Hampton Phifer, director of animal care for the FARM Program.

Advance registration is not necessary. Each webinar is available via podcast or phone. To participate, click here or phone: (646) 558-8656. When prompted, enter meeting ID 848 3416 1708 and passcode 474057.