Based on the most recent U.S. Drought Monitor data, beef cattle producers are getting a slight reprieve from extremely dry conditions. However, pasture and forage availability this winter will likely still be limited. For the week ending Dec. 6, the U.S. Drought Monitor reported that over 78% of the U.S. is experiencing some level of drought. According to the USDA World Agricultural Outlook Board, approximately 69% of the U.S. cattle herd is located in drought-stricken areas; this is an increase of 33 percentage points from a year ago.

The latest NASS Cattle on Feed report showed a Nov. 1 feedlot inventory of 11.706 million head, about 2% below 11.948 million head in the same month last year. Feedlot net placements in October were down over 6% year over year at 2.054 million head, the lowest for the month since the series began in 1996. Marketings in October were 1.802 million head, up less than 1% year over year with the same number of weekdays in the month. On Nov. 1, the number of cattle on feed over 150 days dipped below year-ago volumes for the first time since April. Tighter market-ready supplies in Kansas and Iowa more than offset larger volumes of cattle on feed over 150 days in Texas and Nebraska.

Based on actual and estimated slaughter for November, the pace of slaughter based on the number of weekdays in a month for fed cattle and nonfed cattle slaughter was up over 1% and 4%, respectively, from last year. In fourth-quarter 2022, anticipated fed cattle marketings are raised on a relatively strong pace of fed cattle slaughter through November. In addition, beef cow slaughter is expected to be higher than previously assumed through the end of December. As a result, the beef production forecast for fourth-quarter 2022 is raised by 70 million pounds on higher expected total cattle slaughter, along with slightly heavier carcass weights. Total 2022 beef production is projected at 28.4 billion pounds, an increase of nearly 2% from 2021.

Estimated slaughter in early December suggests a slowing year-over-year pace of fed cattle slaughter. The slower expected pace is carried over into early 2023, as a portion of expected fed cattle marketings were shifted from the first to the second quarter. Heavier expected carcass weights in fourth-quarter 2022 are also carried over into early 2023. The temporal shift in expected marketings and heavier anticipated weights are offsetting, keeping the 2023 beef production forecast unchanged at 26.3 billion pounds.

Cattle prices unchanged

After nearly three months of feeder cattle prices averaging around $174 per hundredweight (cwt), tighter supplies of feeder steers likely helped support higher prices in November and early December. For November, prices for feeder steers 750-800 pounds at the Oklahoma City National Stockyards recorded a weighted average of $177.35 per cwt. The average price of feeder steers from the Dec. 5 report sales was $177.18 per cwt. Lower projected corn prices for fourth quarter also likely supported firm feedlot demand. Price projections for 2022 and 2023 feeder steers are unchanged.

From last month, packer margins continued to decline as the rally in wholesale prices pulled back, and fed cattle prices improved. For the week ending Dec. 4, the negotiated price for fed steers in the 5-area marketing region climbed to $156.42 per cwt, the highest weekly price for any December since 2014 (which was $166.83 per cwt). Saturday slaughter volumes in early December are lighter than last year at this time and may portend a slight pullback from relatively high fed cattle prices through the end of the year. Accounting for current price data, the fourth-quarter 2022 price forecast is unchanged from last month at $152 per cwt. Price projections for 2023 are also unchanged at $156 per cwt.

October exports rebound from previous month

After a slight slowdown in September, exports rebounded in October, setting a new record for the month at 301 million pounds (Table 1). Exports to China and South Korea were particularly high in October. Shipments to China were up 28% over last year and were the second-highest monthly export to the country on record. Exports to South Korea increased nearly 18% year over year and were a record for October.

Cumulative exports through October continue to outpace last year by more than 5%, setting a pace for another record year of exports. This has been supported by very strong exports to China, with a year-over-year increase of over 114 million pounds, or 26%. The share of exports to China has increased to 19% this year, making it the third-largest market for beef exports. Exports to Japan have decreased slightly year over year, down less than 1%; however, the country remains the largest export market for the U.S. Exports to South Korea are up 3% this year. Year-to-date exports to North America are net lower as fewer shipments to Mexico (down 12%) have more than offset a slight increase in exports to Canada.

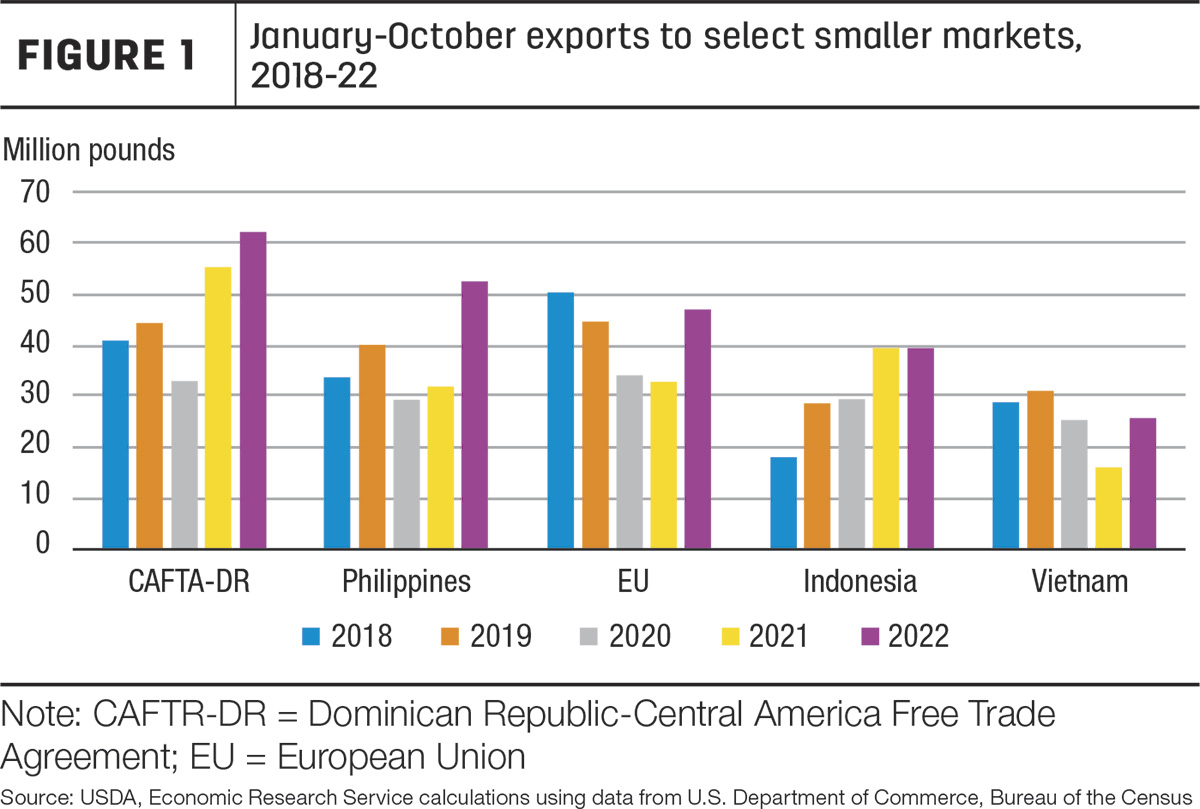

Also supporting the strong export pace this year are combined exports to smaller markets not in the top six, which are up 8% from last year. Of these, the five largest markets with increases over last year are shown in Figure 1. These five markets account for an aggregate increase of 51 million pounds, or 36% of the overall increase in exports through October this year.

Exports to countries in the Dominican Republic-Central America Free Trade Agreement combined are up 12% year over year. Year-to-date exports to the Philippines have increased 20 million pounds, or 64% year over year, and are more than double the five-year average. Exports to countries in the European Union have increased 44% from last year. Shipments to Indonesia are relatively unchanged from last year, up less than 1% but are 51% over the five-year average. Exports to Vietnam have increased 59% year over year. For many of these markets, the easing of COVID-19 restrictions, the return of tourism and a continuing limited supply from Australia have supported increased demand for U.S. beef.

Exports to countries in the Dominican Republic-Central America Free Trade Agreement combined are up 12% year over year. Year-to-date exports to the Philippines have increased 20 million pounds, or 64% year over year, and are more than double the five-year average. Exports to countries in the European Union have increased 44% from last year. Shipments to Indonesia are relatively unchanged from last year, up less than 1% but are 51% over the five-year average. Exports to Vietnam have increased 59% year over year. For many of these markets, the easing of COVID-19 restrictions, the return of tourism and a continuing limited supply from Australia have supported increased demand for U.S. beef.

Based on anticipated firm demand from Asia and recent trade data showing stronger-than-expected exports to a number of smaller markets, the U.S. beef export forecast for fourth-quarter 2022 is raised 20 million pounds to 870 million. The 2022 annual forecast is 3.562 billion pounds. The anticipated demand is carried into first-quarter 2023, which is also raised 20 million pounds to 760 million, although the forecast remains 10% below first-quarter 2022. The 2023 annual forecast is raised to 3.09 billion pounds.

October imports down year over year

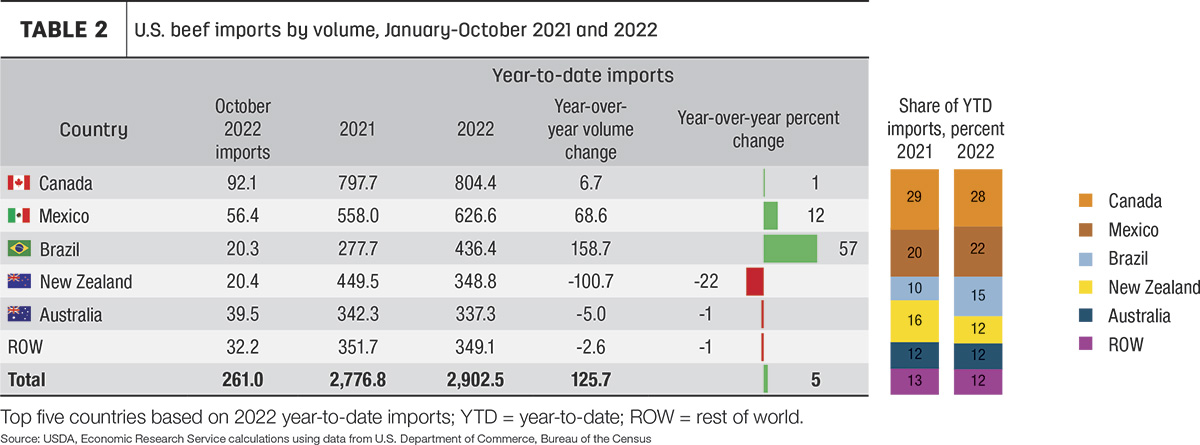

Beef imports in October were 261 million pounds, a year-over-year decrease of about 11% (Table 2). Nearly all major suppliers were lower year over year in October, except for imports from Canada, which were 3% higher year over year. The greatest decreases came from Brazil (down 46%) and New Zealand (down 32%). Monthly imports from Mexico were also down 6% year over year; however, year-to-date imports from Mexico continue to outpace last year, up 12% through October.

Annual U.S. imports are projected to remain largely flat into 2023, decreasing less than 1% from the 2022 forecast. The annual forecasts for 2022 and 2023 are unchanged this month at 3.376 and 3.35 billion pounds, respectively.

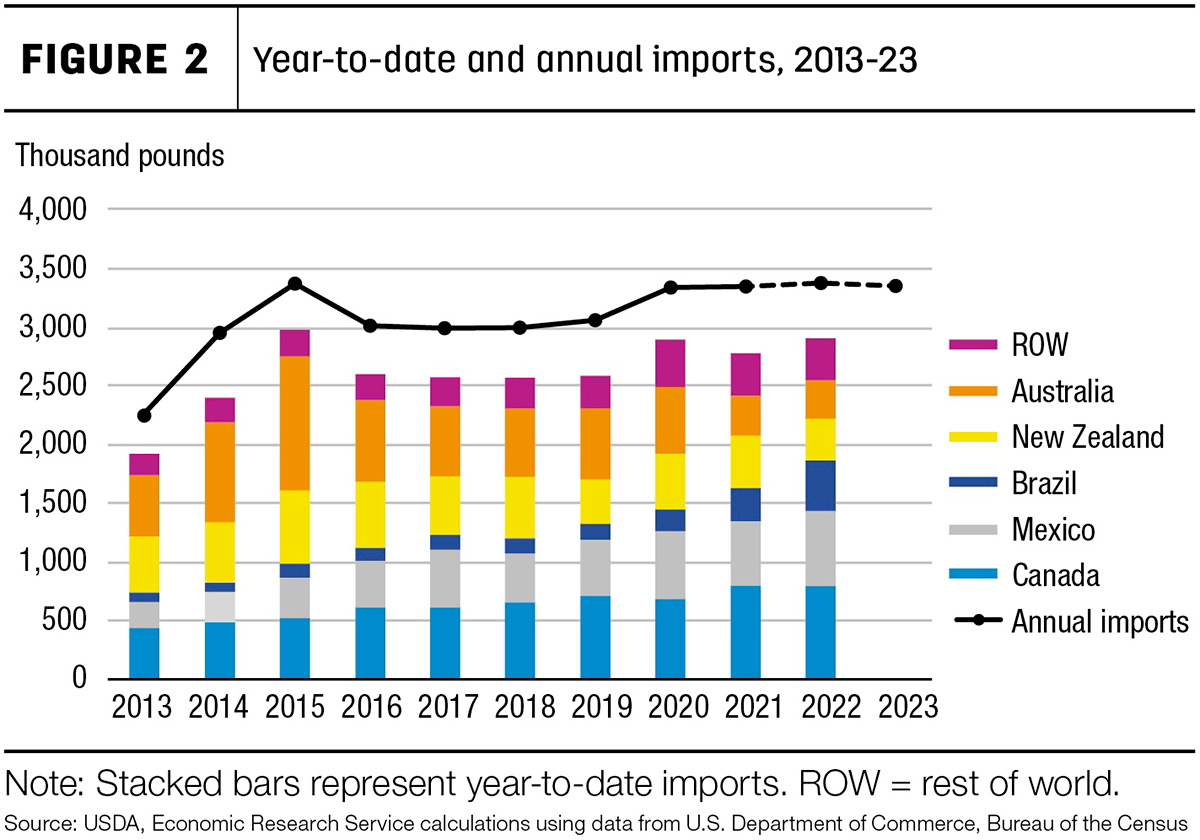

The share of U.S. imports from the top five suppliers has shifted throughout the last few years, as shown in Figure 2. This has been influenced by many factors. One of the more sweeping changes over the past couple of years has been the increase in imports from Brazil.

The lifting of the ban of fresh beef imports from Brazil in 2020 has greatly contributed to the country’s ability to ship beef to the U.S. and offset lower exportable supplies from Oceania. Imports from Australia have decreased substantially from 2015, influenced by drought-induced herd liquidation followed by herd rebuilding and finally by labor and supply chain issues this year. In addition, increased competition for global beef imports, especially from China, has compounded the limited beef supplies from Oceania available for U.S. import in recent years. Imports from Mexico have trended upward over time as the country continues to build production capacity. Imports from Canada have also grown over the years.