The verdict is in – an open cow is among the top three financial liabilities for cow-calf operators. Calf sales are the largest contributor to annual income; cows that fail to wean a calf are a financial burden borne by the productive cows. Profit-driven cattlemen focus on managing annual cow cost. Depreciation, which is the purchase/capitalization cost minus salvage value divided by years of useful life, is typically among the top three contributors – along with labor and fed feed – to annual cow cost.

Longevity is directly related to fertility. With that in mind, King Ranch Institute for Ranch Management students worked with a seedstock breeder to add financial metrics to the development of fertility/longevity expected progeny differences (EPDs). Seems like a simple metric; any cow in the herd after five years has had five calves, right? Ideally, yes, but of greater interest are cows that leave the herd before weaning a fifth calf. Cows that depart before recouping all of their depreciation saddle the productive cows with extra cost.

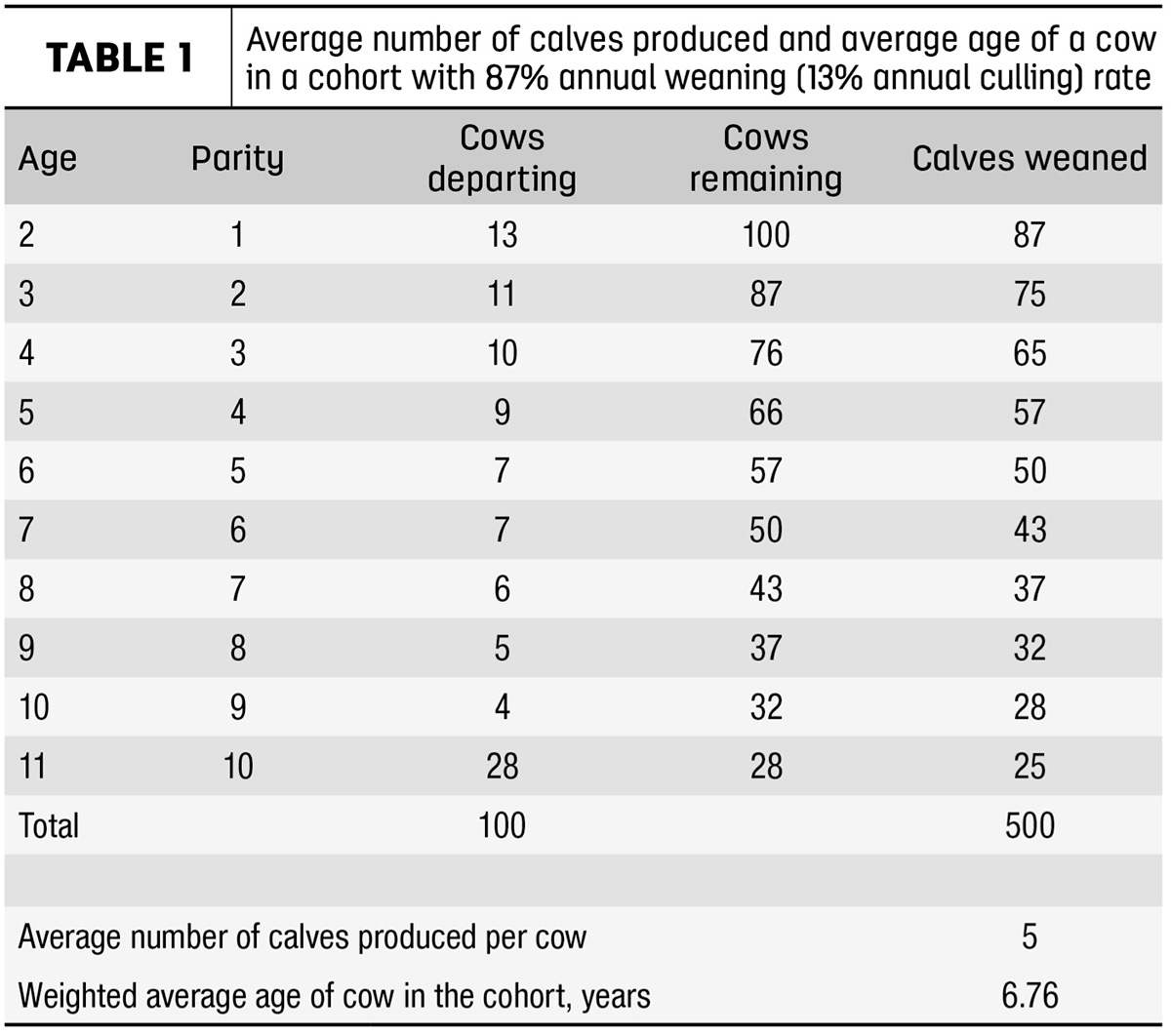

Excluding circumstances such as liquidation due to drought, pregnancy status is the primary determinant of the "keep or cull" decision. When relating the percent cow herd retained – or weaning percentage, since these have a direct relationship – to the average number of calves that a cow will produce in her lifetime, the weaning percentage resulting in a cow herd average of five calves per cow lifetime is 87% (Table 1).

In the calculation, weaning rate was equated to retention rate, and it was assumed all open females are removed from the herd at weaning. It was also assumed that all cows left the herd – regardless of pregnancy status – after their 10th pregnancy. Admittedly, weaning rate may exceed retention rate (e.g., culling bred females due to feet problems or disposition), but pairing weaning rate and retention rate facilitates evaluation of the relationship between longevity and retirement of depreciation. Additionally, in this calculation, a constant culling rate was assumed each year, although in a given year certain ages of cattle may be more likely to fall out than others.

For example, consider 100 bred heifers with an 87% average weaning/retention rate. In the first year of the simulation, 87 females successfully weaned a calf and progressed to their second parturition as a 3-year-old cow, and 13 opens were removed from the herd. Repeating this simulation through four more parities indicates that by the sixth pregnancy, 50 of the original 100 cows have departed the herd.

Consider the annual depreciation cost of keeping a cow in the herd. For this example, assume a heifer purchase/capitalization cost of $2,000 and an $800 salvage – these numbers can be adjusted to match specific ranch balance sheet entries. Therefore, depreciation equals $1,200 ($2,000 minus $800). Over a useful life of five years, the annual depreciation cost is $240.

Relating longevity and depreciation: for every year short of weaning five calves, there is $240 of unpaid depreciation. The productive cows remaining have to cover $240 for every year that a cow falls short of weaning her fifth calf. For example, if a heifer fails to conceive for her second calf and is culled, she is leaving $960 ($240 x 4 years) of depreciation on the balance sheet.

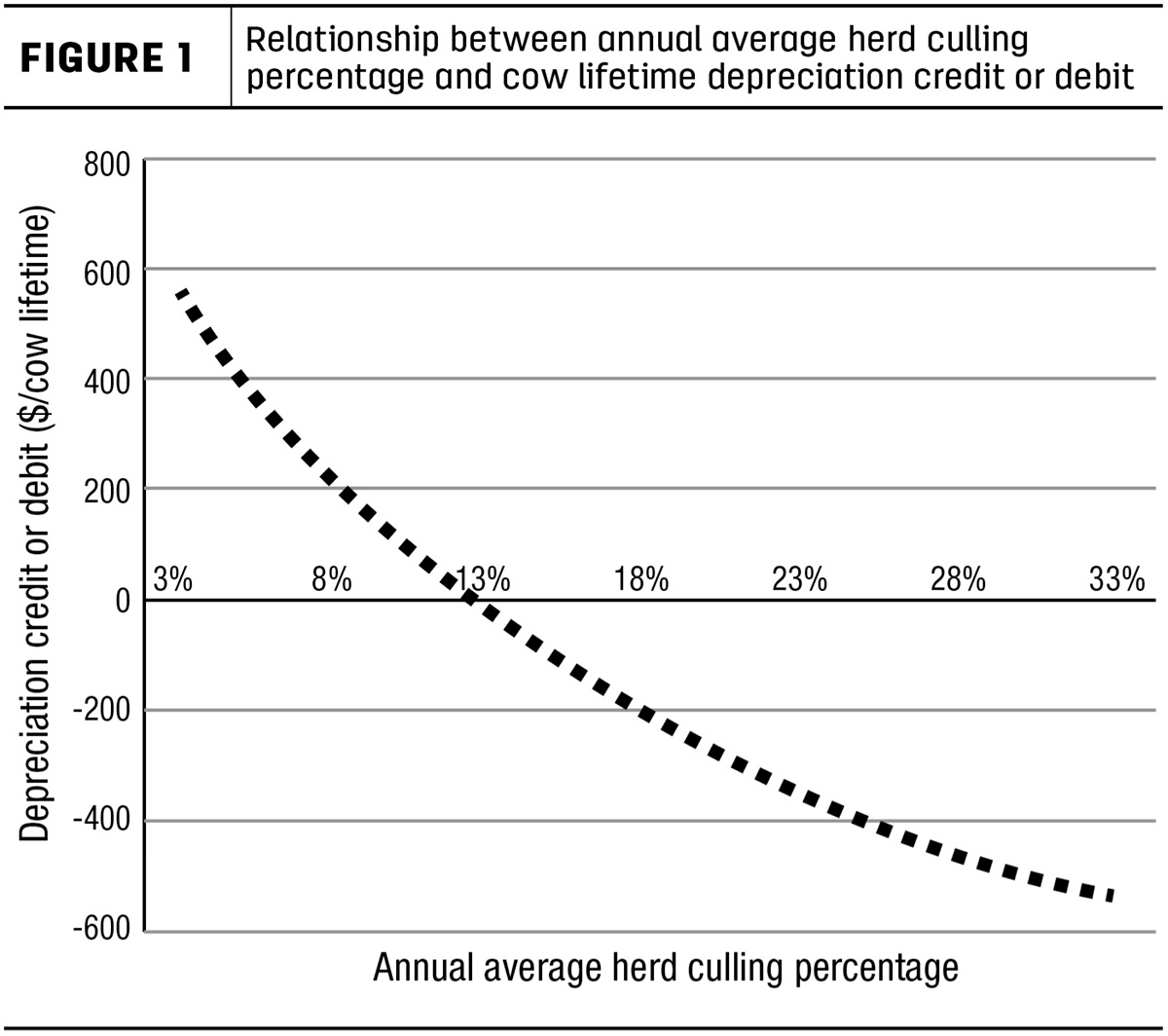

Fertility and longevity are the solutions. As depicted in Figure 1, for every year after weaning a fifth calf – which occurs in a herd with an 87% weaning rate and 13% culling rate – there is a $240 reduction in annual cow cost – described as a depreciation credit – compared to a young replacement entering the herd and incurring depreciation.

As shown in Table 1, with an 87% weaning rate, 50 cows have left the herd before producing five calves, but the remaining 50 cows stay in the herd long enough to cover accumulated depreciation for their cohort.

Takeaways

First, though not a cash cost, cow depreciation is real and must be accounted for on the balance sheet. Second, profit-driven managers can decrease cow depreciation by increasing salvage value (expose and market as bred cows calving in a different season versus packer cows), grazing spring-calving cows after weaning, adding weight and marketing them in the historically annual high spring-packer cow market, or by decreasing the purchase/capitalization cost of replacements. (Read more about this topic here.)

Finally, cow longevity is directly related to profitability. The industry average female replacement rate is 15%. In this example, cows leaving the herd before weaning a fifth calf – a 13% annual culling rate – often results in a capital loss on the balance sheet due to residual (unpaid) depreciation. Use herd records and fertility/longevity/stayability tools to select females that are adapted to the production environment and herd management to improve longevity and cow-calf enterprise profitability.

Caroline Wild and Nathan Clackum are King Ranch Institute for Ranch Management graduate students.