Attendees at the 2025 Range Beef Cow Symposium held in Cheyenne, Wyoming, were treated to a broad range of information on topics affecting the U.S. cattle industry – from market and weather outlooks to discussions surrounding sustainability and building back the cattle herd. Tyler Cozzens, agricultural economist with the Livestock Marketing Information Center, shared an update on the global beef market, and Troy Applehans, a senior market analyst with CattleFax, also discussed the current state of the cattle markets and gave an outlook for 2026.

Cozzens shared that U.S. beef exports have faced some headwinds in 2025, and not merely due to tariffs and other trade policy changes. The exchange rate of the U.S. dollar has made importing U.S. beef a challenge for many countries, although demand for quality is still strong, so exports are down but still less accessible from a price point compared to less costly competitors such as Australia, New Zealand and South America. South Korea and Japan remain our top markets for beef exports. “Korea is definitely one of our key markets. We've actually seen some gain there,” Cozzens says. “There's still a large consumer understanding of the value and the quality of the product that they're purchasing from the U.S. Japan is definitely in there too – down from a year ago but still very much in line with what we've seen.”

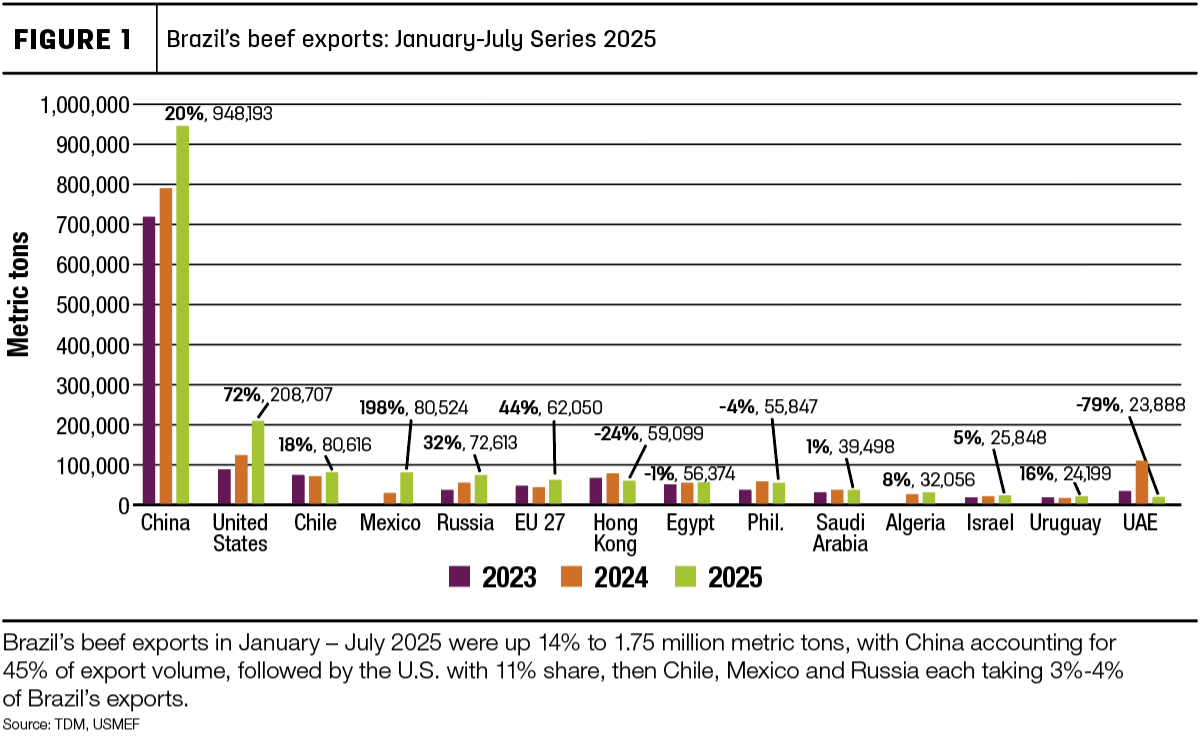

Brazil has taken center stage as a major beef exporter. The U.S. is currently Brazil's second-largest imported beef customer, with China in the number one spot, claiming 45% of Brazil's total beef export volume (Figure 1). Another import market that was hit significantly was live cattle imports from Mexico due to border closures caused by New World screwworm (NWS). The sudden and continued dearth of Mexican feeder cattle has contributed to market volatility through 2025 and into 2026. The threat of NWS continues to be a major concern for U.S. beef producers, and the possibility of the Mexican border reopening is unknown at this point but remains at the forefront of industry issues to watch in 2026.

Applehans says, looking purely at profit and loss, the cattle industry has faced a few years of record profits, and the cow-calf producers are currently in the driver’s seat. The national herd is at its lowest since 1961, and demand remains high, but the cattle cycle will eventually swing back around to signal expansion. “We know that we are expanding the herd,” he says. “I think it's a slow, methodical type of an expansion – much slower than the last cycle that we went through.”

Applehans shared some headwinds that, combined with the volatility in the markets, will likely keep an expansion in low gear: age of the producer, labor, high interest rates, lack of land and/or capital, and urban sprawl, to name a few. “We know that the economic incentive is there to expand,” he says. “It's the ability to expand, and the want to expand that is the question.”

Some indicators of expansion are tight cattle supplies and lower slaughter rates, which are down 30% since 2022, a younger cow herd and a slow retention of replacement heifers. Applehans says a slower expansion is better for the cow-calf producer to maintain some leverage in the market, unlike the expansion of the U.S. cattle herd back in 2014-16, when the herd rebuilt so rapidly that the cow-calf producers lost packing capacity, and thus a good deal of leverage.

“We know we're near the lows in terms of our harvest, and it would also imply that we're near the peak, regardless of policy situations, in price,” he says. “This isn't going to be a repeat of 2015 and 2016, where prices just plummeted lower for two years. With the policy decisions that have been made, it is a higher probability that we can have a significant correction in the market, but we're starting at a higher level.”

Applehans said the market volatility and uncertainty of so many moving parts makes it difficult to come close to a projection of how markets will react. “Markets do not like uncertainty. They do not like it at all, and that's what we've been going through,” says Applehans. The closure of the U.S.-Mexican border due to NWS drove up cattle futures, which, if the border reopens, will come back down, but there’s no way of knowing when that will happen. The market reaction to the proposal of bringing in more exports, specifically from Argentina, and artificially bringing down beef prices caused even more uncertainty. “All of this has led to the volatility that we've seen, but I also think it led to a high degree of the increase that we saw into the market as well.”

Applehans urged producers to prepare for sustained periods of volatility. “I think it's incumbent upon you all, as cow-calf producers, to do something with regards to managing your risk going forward, whether that be through LRP, forward contracts, or basis contracts, whatever the case may be.”