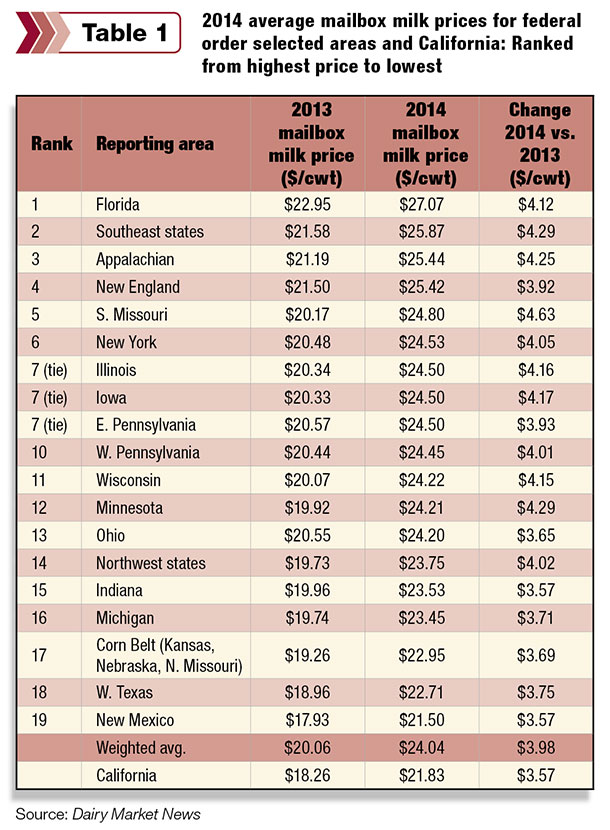

As we all know, 2014 was a record year for farm milk prices, and this was reflected in a record average mailbox milk price of $24.04 per hundredweight (cwt) for various federal order reporting areas. The California 2014 mailbox average was $21.83 per cwt.

The high Class I utilization markets, Florida, Southeast states and Appalachian, continue to have the highest mailbox prices while California, New Mexico and west Texas have the lowest mailbox prices (see Table 1 ).

Southern Missouri had the largest increase in mailbox price from 2013 to 2014, which was $4.63 per cwt. In fact, southern Missouri moved from ranking 11th on the 2013 mailbox price list to fourth on the 2014 list. In comparison, California, Indiana and New Mexico dairy farmers experienced the lowest increase, $3.57 per cwt.

Comparing mailbox prices to federal order blend prices provides us with some insight on market conditions in the various reporting areas. However, to make an “apples to apples” comparison, an adjustment must be made to the order blend price.

Mailbox prices are announced at the average component tests for the reporting area. On the other hand, the federal order blend price is announced at a standardized test, 3.5 percent butterfat. And for orders with multiple component pricing, protein is standardized to 2.99 percent and other solids to 5.69 percent.

Orders also have location adjustments within the order. Mailbox prices are an average of these location adjustments while the order blend price is announced at the base location. Taking all of this into consideration, I estimate an “adjusted federal order blend price” for each mailbox reporting area, to make the comparison between the two prices (see Table 2 ).

What might we learn from comparing the two prices? In markets with a mailbox price higher than the order blend price, dairy farmers are most likely receiving premiums over the federal order blend price, including subsidized hauling.

Milk supply and demand are in reasonable balance in such markets. Extra money is not needed to ship surplus milk out or bring additional milk in. The market is probably competitive for raw milk, and plants are willing to pay above order prices to procure milk.

If the mailbox price is lower than the federal order minimum, then the opposite may be occurring. There are little or no over-order premiums or subsidized milk hauling. The market may have excess milk, and cooperatives are transporting milk some distance to find a home.

Excess milk may be sold at a price lower than the federal order minimum. Or in deficit markets, a cooperative may have to pay additional money to bring in enough milk to meet full-service contract obligations.

These additional costs most likely are charged back to cooperative members, resulting in a lower milk price, a price below the federal order minimum. Remember, a regulated proprietary milk plant cannot pay dairy farmers or cooperatives a price below the federal order minimum price. However, cooperatives can pay its members below the order blend price.

Looking at Table 2, we see the areas with the higher mailbox prices compared to the adjusted blend, and those with the lowest in 2014 are similar to their 2013 ranking. However, only seven of the 19 reporting areas showed a mailbox price higher than the adjusted federal order blend price in 2014.

This compares to 2013 with 10 out of 19 reporting higher prices. Plus, out of the seven areas with higher mailbox prices, all were lower relative to the adjusted blend price than last year. Most of the reporting areas with mailbox prices lower than the adjusted federal order blend price showed a greater difference below the adjusted order blend in 2014 compared to 2013.

With record milk prices in 2014, we would expect lower mailbox price relative to the adjusted blend price. Higher regulated prices generally mean lower over-order premiums. In addition, 2014 saw parts of the country struggling to find markets for surplus milk production.

Much of this surplus milk was sold at prices below the federal order minimum in order to find a home. Some cooperatives charged their members additional cost for balancing milk supplies and inventory losses.

All of these factors lower mailbox prices relative to the adjusted order blend. These factors were more prevalent during the first half of 2015, so look for lower mailbox prices relative to the adjusted order blend when the 2015 averages are released.

Even though this article compares mailbox prices to the federal order blend price at the market level, individual dairy farmers should do the same for their own mailbox price. Monthly, dairy farmers should compare their mailbox price to their federal order blend price adjusted for location and components.

It is a good way to watch market conditions and measure how well your milk is being marketed. And if your mailbox price is declining relative to your order blend price, find out why. The more knowledge you can gain about conditions in your milk market, the better opportunity you will have to improve your milk price. PD

Calvin Covington is a retired dairy cooperative CEO and now does some farming, consulting, writing and public speaking.

-

Calvin Covington

- Retired Dairy Cooperative CEO

- Email Calvin Covington