For many Americans, work and social activities are returning to some form of pre-COVID-19 normal. So is milk marketing through the Federal Milk Marketing Order (FMMO) system. Here’s Progressive Dairy’s monthly attempt to navigate through the numbers to see how “normal” might appear on your milk check.

Uniform prices and PPDs

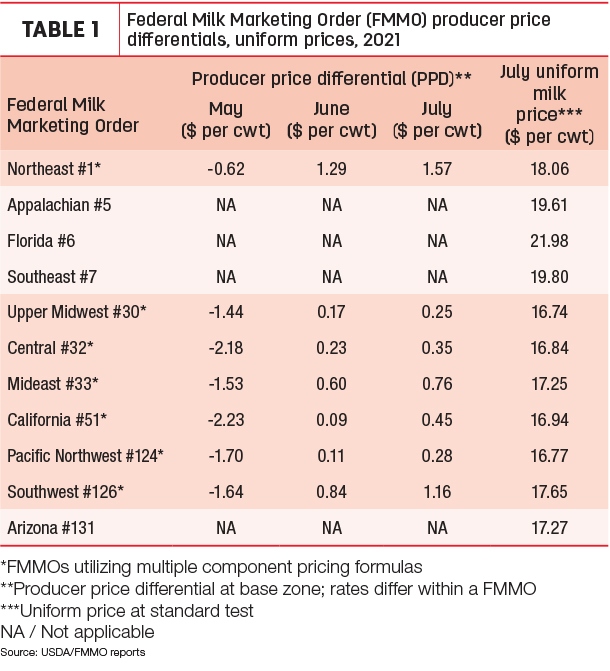

FMMO administrators reported July 2021 uniform milk prices, producer price differentials (PPDs) and milk pooling data during the week of Aug. 13. As they were in June, July baseline PPDs in all applicable FMMOs were again positive. One the other hand, uniform or “blend” prices at standardized test moved lower in all 11 FMMOs.

With Class I, Class III and Class IV milk prices down from June, July uniform or “blend” prices were down 36-64 cents per hundredweight (cwt) across all 11 FMMOs. The high was $21.98 per cwt in Florida FMMO #6; lows of under $17 per cwt were in four FMMOs (Table 1).

July 2021 marked the second consecutive month that baseline PPDs were positive in all FMMOs utilizing multiple component pricing, moving 8-36 cents higher from June. As we note every month, however, PPDs have zone differentials and vary slightly within each FMMO, in some cases -10 cents to -50 cents per cwt from the base PPD in each order. Also, whether positive or negative, PPDs’ impacts on producer milk checks are based on deductions by their individual milk handlers.

As described by dairy economists Marin Bozic and Christopher Wolf, negative PPDs have a half-dozen contributing factors, including declining Class I fluid milk sales and differences in how the value of milk protein is collected and distributed to the spread in Class III-Class IV milk prices and depooling.

Protein, butterfat values dip

Some of the same factors that produced positive PPDs in July also played a role in lowering uniform milk prices.

Declines in cheese and butter prices drove down the value of both protein and butterfat used in monthly Class III and Class IV milk price calculations. At just under $2.50 per pound, the value of milk protein in July fell nearly 9 cents from June and is the lowest since May 2020. The value of butterfat posted a similar but smaller decline in July, down 6.5 cents to about $1.90 per pound.

When factored into milk class prices, the July 2021 Class III price fell to $16.49 per cwt, down 72 cents from June 2021 and $8.05 less than July 2020. At $16 per cwt, the July 2021 Class IV price came off its 17-month high and was down 35 cents from June but was still $2.24 above a year ago.

With Class III falling more than Class IV, the July Class III-Class IV price spread shrunk to 49 cents per cwt, the narrowest gap since January 2020. A year ago, during the height of milk pricing gyrations caused by cheese-heavy purchases for USDA food boxes, the Class III-IV price spread was $10.78 per cwt.

Class III returns to the pool

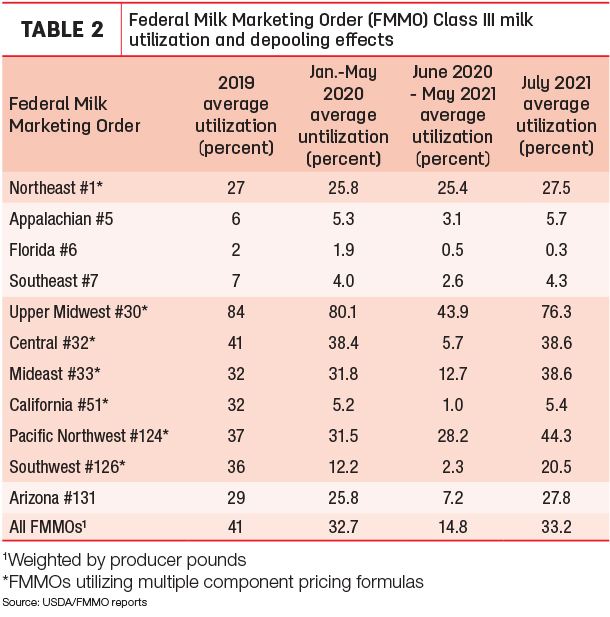

The narrower Class III-IV spread in July 2021, combined with a Class I base price that was higher than the Class III price for only the second month in 2021, reduced incentives for Class III handlers to depool. That brought volumes of Class III milk back to the pool at levels not seen in the past year.

Overall FMMO July 2021 Class III milk utilization and pooling moved higher on both a volume and percentage basis. Only the fluid-heavy FMMOs in the southeast U.S. (Appalachian, Florida and Southeast) posted small declines in Class III pooling.

By volume, total Class III milk pooled across all FMMOs in July 2021 was about 4.09 billion pounds, the most since May 2020 and moving closer to the 4.33-billion-pound average for January-May 2020, prior to the pandemic-related milk marketing disruptions and cheese-heavy food box purchases. By comparison, Class III pooling across all FMMOs still lags the average of 6.6 billion pounds per month during January-August 2019.

July's jump in Class III pooling was especially notable in the Upper Midwest FMMO #30, which saw an increase of more than 750 million pounds of Class III milk compared to June. That's more than the total pooling of all classes of milk in July in each of five other FMMOs (Appalachian, Florida, Southeast, Pacific Northwest and Arizona).

On a percentage basis (Table 2), Class III utilization was about 33.2% of all FMMO milk marketings in July 2021, up from 22.2% in June and the 14.8% average during June 2020-May 2021. Class III utilization was on par with the 32.7% pre-pandemic utilization rate in January-May 2020 but below the average of 41% for all of 2019.

Looking ahead

Are FMMO pooling behaviors and positive PPDs a long-term relationship or just a summer romance? Tracking announced milk class prices and Chicago Mercantile Exchange (CME) Class III and Class IV milk futures prices provides some guidance.

Near term, the August 2021 Class I base price, already announced at $16.90 per cwt, will almost certainly be higher than Class III-IV prices. Actual August Class III and Class IV milk prices won’t be announced until Sept. 1, but as of the close of CME trading on Aug. 13, Class III and Class IV milk futures prices closed at $16.12 and $15.75 per cwt, respectively.

Markets change, but that would result in a Class III-Class IV spread of just 37 cents, the narrowest gap since June 2019, when the Class IV price was higher than Class III price.

While those prices and price relationships might be good for depooling and PPDs, it also means August uniform milk prices will be lower than July prices.

Beyond August, the Class III-IV price spread grows to more than $1 per cwt in September through early 2022, peaking at about $1.65 per cwt in November and December, resurrecting depooling possibilities. At the same time, futures prices indicate at least some improvement in overall milk prices to end the year.

One other item of note: After a year of dairy producer Class I milk income “losses” attributed to the change from the “higher of” to the “average of plus 74 cents” FMMO Class I mover price formula, the closer Class III-IV price relationship means producers likely saw a net Class I price benefit in July and August.