On July 22, the USDA National Agricultural Statistics Service (NASS) released the midyear Cattle report. It provided a snapshot of the U.S. cattle herd, which includes both beef and dairy cattle as well as a glimpse into producers’ outlook for retaining heifers and the availability of cattle for placement in the coming year. The report estimated the U.S. cattle herd on July 1 at 98.8 million head, which is 2% – or 2 million head – below a year ago. Currently, the U.S. beef industry is in a contracting phase of the cattle cycle that began during 2014 and peaked in 2019.

As the number of cattle has declined since 2019, several indicators in the report were evaluated to assess the stage of herd reduction. While the report does not distinguish beef cattle from dairy cattle in all its statistics, it does specify separate statistics for heifers and cows. That is significant, as beef females make up two-thirds of all females and about a third of all cattle types. To gauge the direction and magnitude of the cattle cycle, it is important to examine the estimated number of beef cows and the number of beef heifers producers expect to retain to either replace older cows or increase their herds.

According to the Cattle report, the number of beef cows on July 1 was estimated at 30.4 million head, 2.4% below July 1, 2021. The number of dairy cows is estimated at 9.5 million head, 0.5% less than the previous year. Further, producers intend to keep about 4.2 million beef heifers as beef cow replacements, almost 3.5% fewer than producers intended to keep at this time last year. This is one of the lowest retention estimates of replacement heifers as a percent of beef cows since 2011, and the lowest total heifers estimated for retention since the series began in 1973. During this time, the number of heifers retained has ranged from 4.2 to 7.9 million head. In addition, dairy producers are retaining 3.8 million heifers, the fewest replacement heifers since 2005. For context, since 1973, the number of dairy heifers retained midyear has kept a range between 3.6 and 5 million head.

“Other heifers,” which are females typically relegated to feedlots and not retained for breeding purposes, are also reported in the Cattle report. When fewer heifers are retained for beef cow replacements, more females might enter feedlots. Although the number of other heifers declined from last year, as did all types of cattle, the heifers on feed increased. According to the July NASS Cattle on Feed report, the number of cattle on feed totaled 11.3 million head on July 1, 2022, up slightly from last year. The report estimated 4.4 million heifers on feed, which is an increase of 3% and represented a larger share of the cattle on feed than last year.

The initial estimate of the 2022 calf crop reported in the Cattle report is 34.6 million head, 1.4% below a year ago. The ratio of calf crop to number of cows and heifers expected to calve on Jan. 1 was higher than in the last three years, and the ratio was larger than expected.

From the time the herd size peaked in 2019, it appears the contraction of the beef cattle herd has been accelerating. Further contraction is supported by the lowest number of heifers expected to be retained at this time of year and the estimates of heifers on feed, as well as by the lively pace of producers culling beef cows from their herd.

Observing non-breeding types of cattle, the number of cattle outside feedlots available for placement in feedlots in the second half of 2022 can be assessed by adding the number of steers, other heifers and calves under 600 pounds and then subtracting the total number of cattle on feed. The number of cattle not in feedlots is 37.5 million head, which is smaller by 3%, or 1 million head, than at this time last year.

Robust slaughter raises outlook for late 2022 and 2023

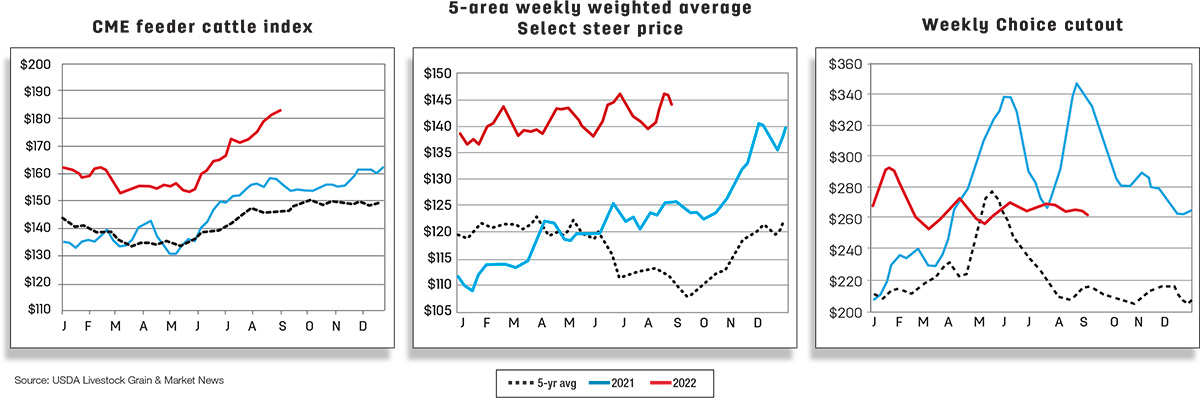

There are a couple of takeaways regarding cattle slaughter in the first half of 2022. The first is the aggressive culling of beef cows. This is likely based on producers’ reaction to pasture conditions and increased operating costs, and then by the packers’ ability to achieve weekday slaughter levels of fed cattle, the highest observed since 2013. Strong domestic wholesale beef cutout and lean trimming prices supported by strong domestic beef demand and record export sales helped support this level of slaughter.

At the beginning of second-half 2022, drought conditions have intensified through July into August, particularly in the Southern and Central Plains and the Southeast. As a result, pastureland conditions have declined since the previous month and are at levels typically occurring in the fall. This continues to manifest itself in beef cow slaughter, as 60% of cattle are experiencing drought and producers continue to cull deep into their herds. Regions 6 and 7 are the areas reporting the highest beef cow slaughter volumes. These areas represent where slaughter takes place, and some of these cows may not have originated in these areas.

As a result, the pace of beef cow slaughter in July is the fastest recorded since the USDA Agricultural Marketing Service (AMS) began reporting the series in 1986. Looking at the rest of the year, it is expected that beef cow slaughter will likely decline, but not below year-ago levels until early next year.

In addition to rapid pace of cow slaughter, the weekday pace of federally inspected fed cattle slaughter in July is the fastest in over a decade. However, despite robust cattle slaughter reported in July, the outlook for 2022 beef production is forecast only slightly higher, by 68 million pounds from the previous month to nearly 28 billion pounds. This is mainly on higher expected cow and fed cattle slaughter in the second half that is partly offset by lower anticipated average carcass weights. With the anticipated addition of more cows in the slaughter mix than expected the previous month and recent carcass weight data from the AMS July weekly reports of Actual Slaughter Under Federal Inspection, prospective weights in the second half of 2022 were lowered to levels below the previous year.

For 2023, greater expected fed cattle marketings and heavier expected carcass weights more than offset a reduction in anticipated cow slaughter to raise projected beef production by 325 million to 26.3 billion pounds. The larger increase in marketings next year is grounded on the prospect of more cattle placed in feedlots in second-half 2022 and first-half 2023. Higher calf placements in late 2022 are bolstered by the likelihood that poor pasture conditions will move cattle into feedlots at a quicker pace and in early 2023 by placements from the 2022 calf crop. Also, more cows were removed from the forecast in 2023 based on the expected increase in cow slaughter in second-half 2022. Coupled with relatively steady feed costs, this tipped the scale slightly toward heavier expected carcasses next year.