Drought and pasture conditions have improved from the previous month, but the situation is still very poor compared to last year and previous years. On May 12, the USDA National Agricultural Statistics Service (NASS) reported that national hay stocks were down 18% on May 1 from the previous year. However, stock levels of hay by state were mixed across the country. States reporting less hay available were down significantly from a year ago, which has fueled higher hay prices in those states. Fuel and fertilizer prices are also at or approaching record levels. These factors imply that higher operating costs in addition to continued poor pasture conditions are likely weighing heavily on cow-calf producers and are likely causing them to cull deeper into their herds to offset or reduce costs.

This high culling rate is evident from the first four months of the year as the number of beef cows slaughtered is up 15% from the same period in 2021. Based on weekly actual slaughter data reported by the USDA Agricultural Marketing Service (AMS) through May 28, the pace of beef cow slaughter is almost 10,000 head per week on average above last year for the first four weeks of May.

Based on the pace of beef cow slaughter to date, the anticipated slaughter of beef cows is raised in the second and third quarters of 2022. However, that should leave fewer beef cows available for slaughter in the fourth quarter.

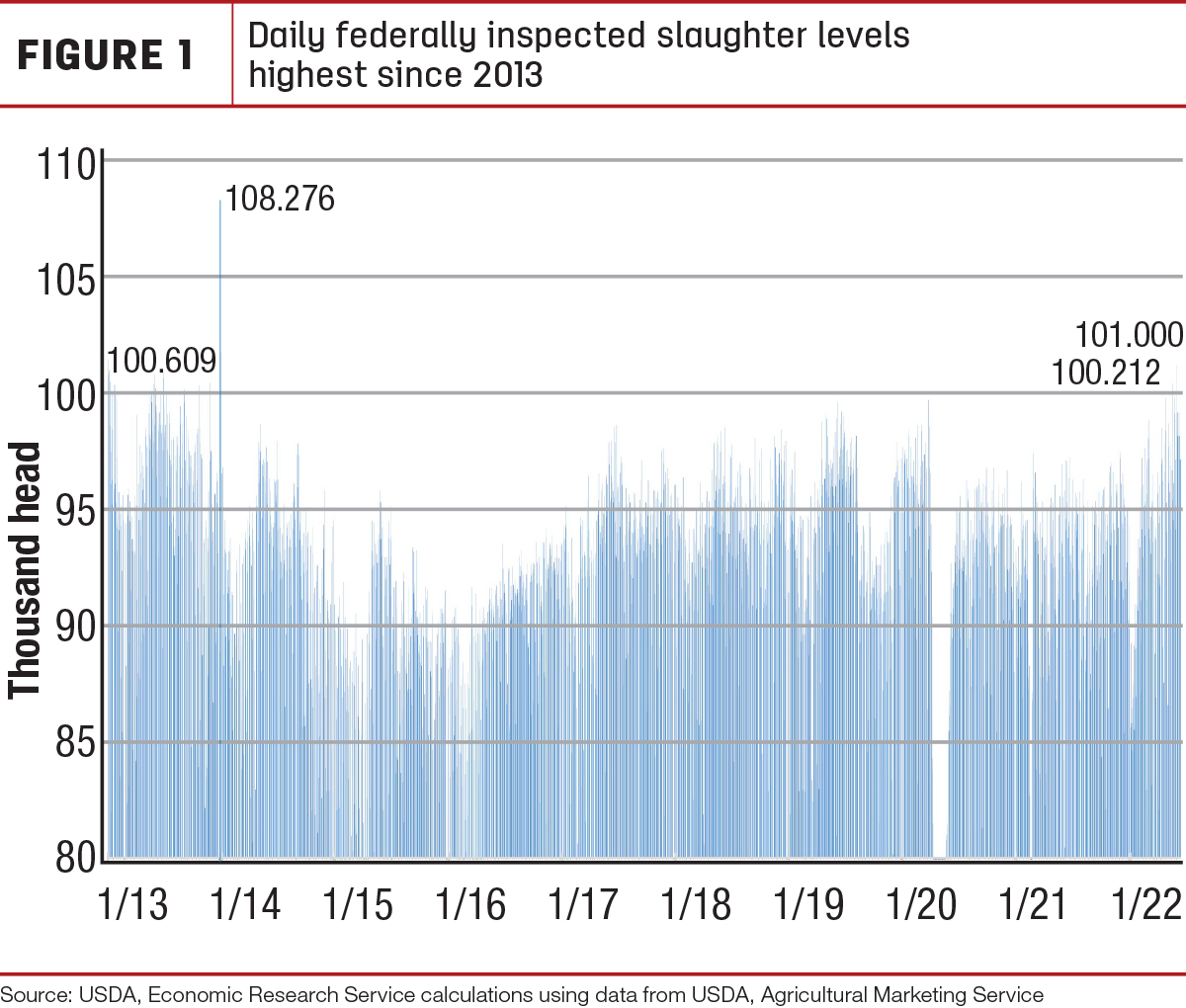

Weekday fed cattle slaughter surpasses pre-covid-19 levels

Based on actual slaughter data through the week ending May 28 reported by the USDA AMS, processing capabilities of packers have improved to pre-Covid-19 levels to the extent that average weekday slaughter has negated the need for large slaughter volumes on Saturdays in order to reach slaughter goals. Further, weekday highs have hit thresholds not seen since 2013 (see Figure 1). Subsequently, it appears that limits to packers’ processing capacity is improving to a point where the fed cattle market is emerging from what may have restricted the market these past two years.

The latest NASS Cattle on Feed report showed a May 1 feedlot inventory of 11.973 million head, a series-record for the month and about 2% higher year-over-year from 11.731 million head in 2021. Despite another month of historically high feedlot inventories in 2022, the volume is declining seasonally month-over-month since the high that was set on Feb. 1.

Feedlot net placements in April were down almost 1% year-over-year at 1.755 million head but well above industry analyst expectations. Marketings in April were 1.893 million head, down 2% year-over-year with one less weekday in the month. On a weekday basis, the pace of marketings in April was up over 2.4%. Further, over the previous three months, February through April, the pace of marketings per weekday has averaged almost 2% above the previous year for that period.

In second-quarter 2022, expected slaughter is raised based on cow slaughter data to date, but it is more than offset by lower expected average carcass weights based on the increase of cows in the slaughter mix and lighter-than-expected steer and heifer weights. Third-quarter 2022 production is unchanged as higher expected cow slaughter is counterbalanced by lower expected carcass weights. The projection for fourth-quarter production is raised 80 million pounds because of higher expected feedlot placements in the second quarter, leading to higher anticipated marketings in the fourth quarter, which more than offsets a decline in expected cow slaughter in the fourth quarter.

As a result, the 2022 production forecast is raised 65 million pounds to 27.9 billion pounds, with higher expected steer and heifer and cow slaughter more than offsetting lower expected carcass weights. The 2023 projection is unchanged from the previous month at over 25.9 billion pounds.

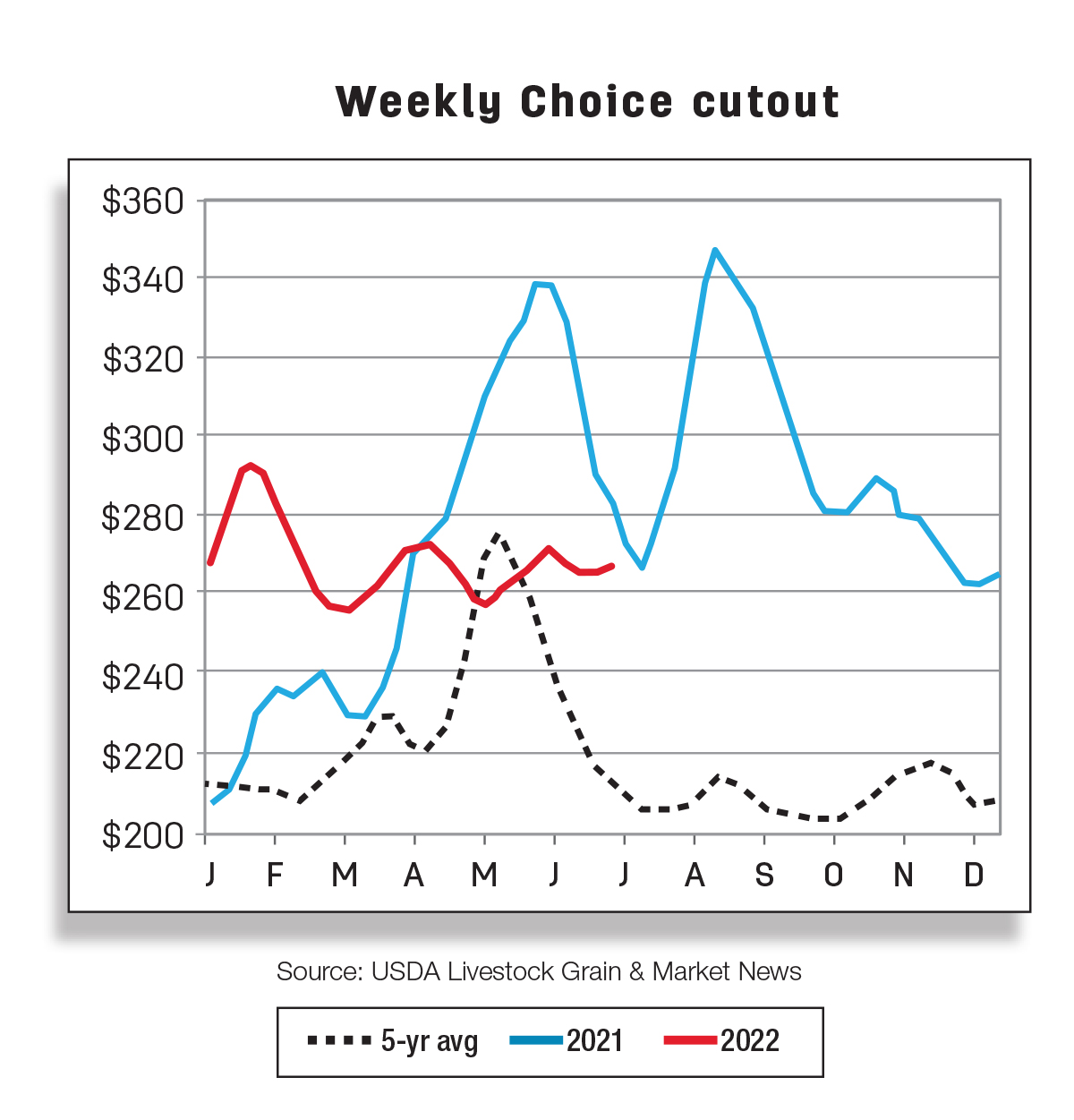

Cattle prices mostly unchanged

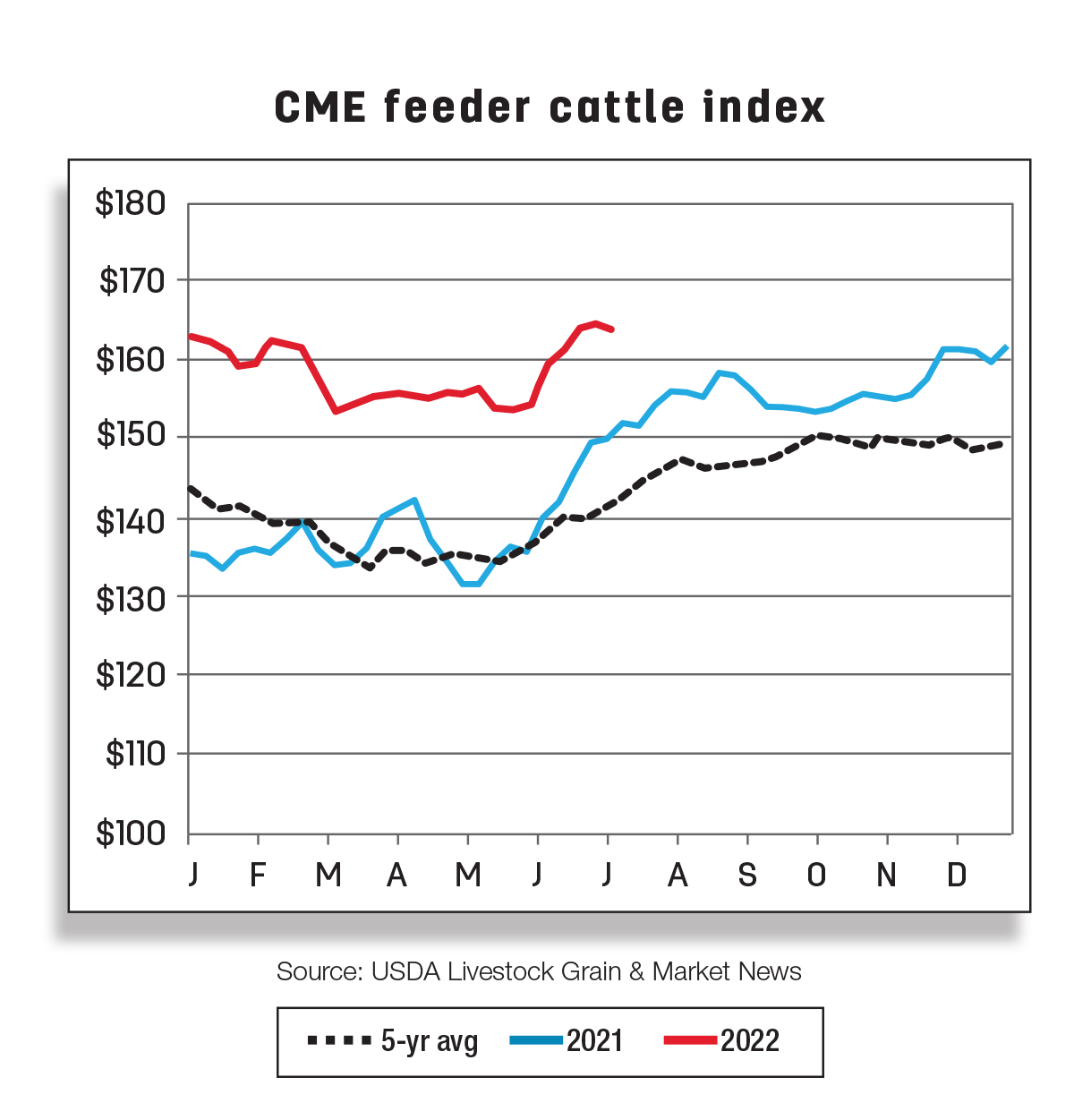

In the first week of June, the price for feeder steers 750 to 800 pounds at the Oklahoma City National Stockyards was reported at $158.08 per hundredweight (cwt). The second-quarter 2022 price forecast is lowered $2 to $157 per cwt on recent data. However, second-half 2022 is unchanged, for an annual forecast of $162.30 per cwt. Feeder steer prices in 2023 are unchanged at $198 per cwt.

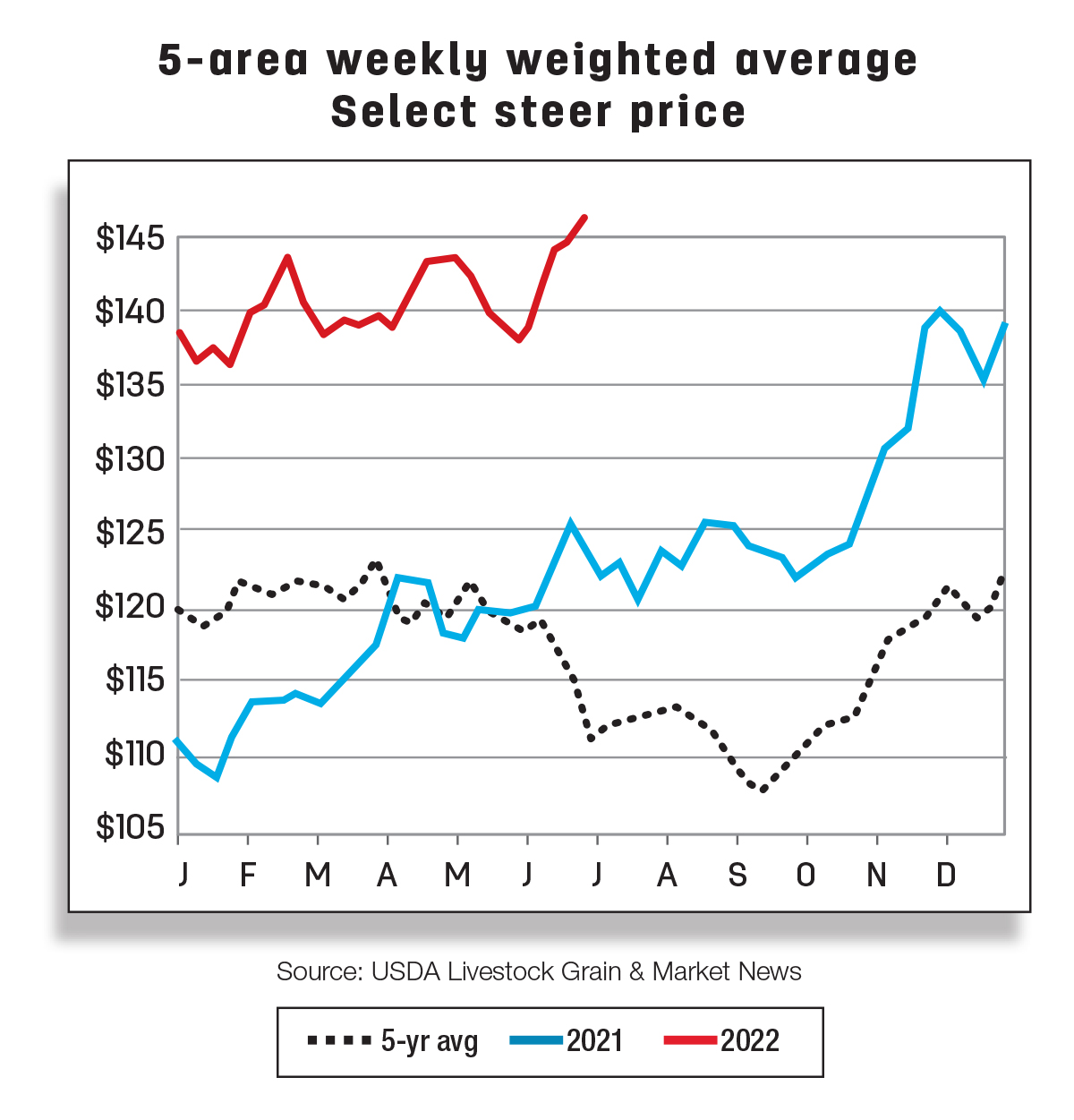

Weekly fed steer prices peaked this year during the week ending May 8 at $143.42 per cwt and have since declined at a slower-than-typical seasonal pace. Fed steer prices for the 5-area marketing region for the week ending June 5 were more than $18 above a year ago at $138.07 per cwt. A generally faster pace of slaughter from packers may keep fed steer prices relatively stable for the remainder of the second quarter. Based on the May 2022 average monthly price of $141.34 per cwt and current daily price data, the 2022 fed steer price is forecast unchanged at $140.10 per cwt. The 2023 fed steer price is also unchanged from the previous month at $153 per cwt.

Exports expected to remain strong despite headwinds

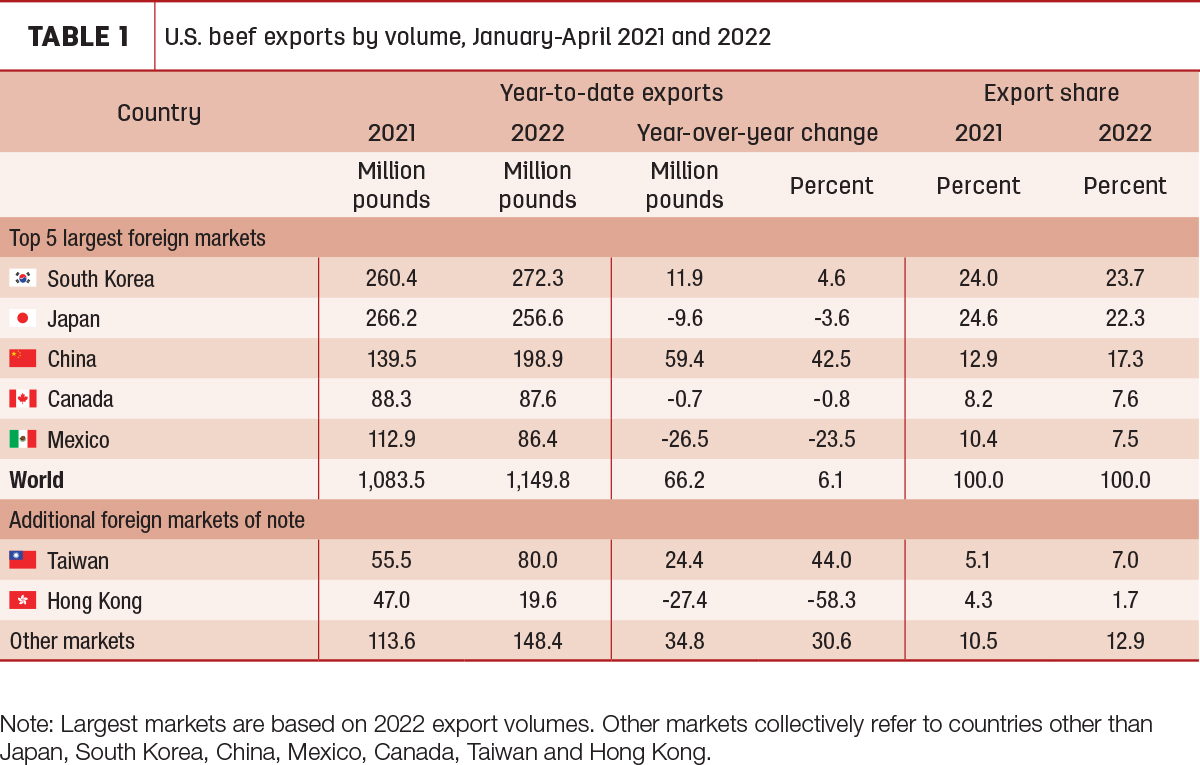

Monthly beef exports remain strong despite obstacles such as inflation, logistical challenges and lockdowns in some markets. Beef exports in April were a record for the month at 304 million pounds and the third-largest of any month overall. Exports to Taiwan were 23 million pounds in April, 40% higher year-over-year and a record monthly shipment to that country. Exports to China were a record for April at 54 million pounds. Shipments to smaller markets continue to make gains. Exports to the Philippines set a new high at nearly 7 million pounds, 86% higher year-over-year. Further, exports to member countries of the Central America Free Trade Agreement –Dominican Republic are setting a record pace in the first four months of the year, up 22% from the same period last year.

As Table 1 shows, cumulative exports from January through April this year are 6% above last year. The largest increases were to Taiwan, China, South Korea and other markets not in the top seven.

Through April, exports to Taiwan are up 44%, and exports to China are up nearly 43%, and those to South Korea are up 5%. Exports to smaller markets combined, those not in the top seven, are up over 30% from 2021. These increases more than offset decreases to Mexico, Hong Kong, Japan and Canada.

Based on strong demand in Asia and the recovery of food service sectors in other key markets, the export forecast for second-quarter 2022 is increased 40 million pounds to 880 million. While exports started the year ahead of 2021, there may be major obstacles throughout the remainder of the year. The U.S. dollar is strengthening in relation to the currencies of certain export markets, making U.S. beef more expensive on top of already high prices. Based on trade data to date, the export forecasts for third and fourth quarters of 2022 are raised 15 and 10 million pounds, respectively. However, second-half 2022 is still expected to show a year-over-year decline of almost 5%.

Despite the overall increase to the 2022 annual forecast, it remains slightly below 2021 at 3.421 billion pounds. The increase in 2022 exports is carried over into the forecast for first-quarter 2023, which is raised 10 million pounds to 660 million, and the annual forecast for 2023 is 2.94 billion pounds, a year-over-year decrease of 14%.

Beef imports remain strong, with some signs of slowing

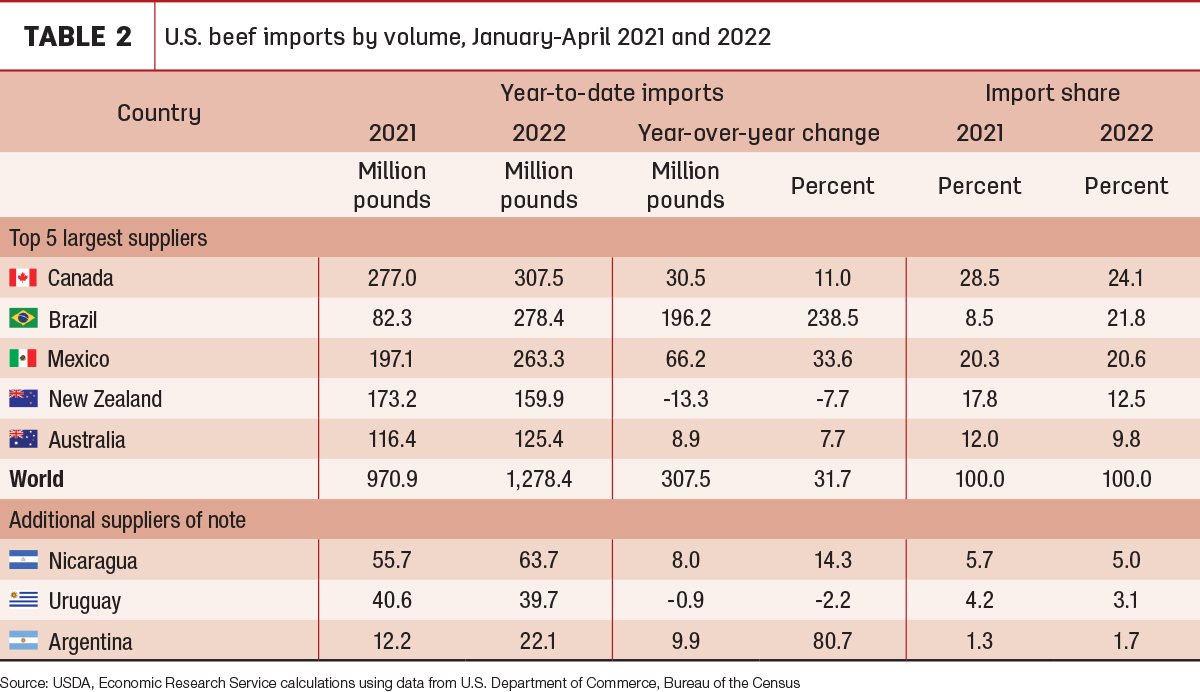

Beef imports in April were 294 million pounds, a year-over-year increase of 7%. Among the top five suppliers, the only year-over-year decreases in imports were from Australia and New Zealand, down 8% and 27%, respectively. Monthly imports from Brazil were up about 52%, and imports from Mexico were up nearly 19%. Other notable year-over-year increases in imports came from Argentina (131%), Nicaragua (16%) and Canada (4%).

Table 2 shows that year-to-date imports have increased nearly 32%. The largest increase has been from Brazil, which has sent nearly 200 million pounds so far this year, an increase of nearly 239%.

Imports from Brazil in April were 48 million pounds, 52% higher than last year but 35% lower than in March. The quota under which the U.S. imports fresh beef from Brazil was filled as of April 4, 2022. Therefore, for the remainder of the year, Brazil will be subject to a 26.4% tariff on the value of these imports.

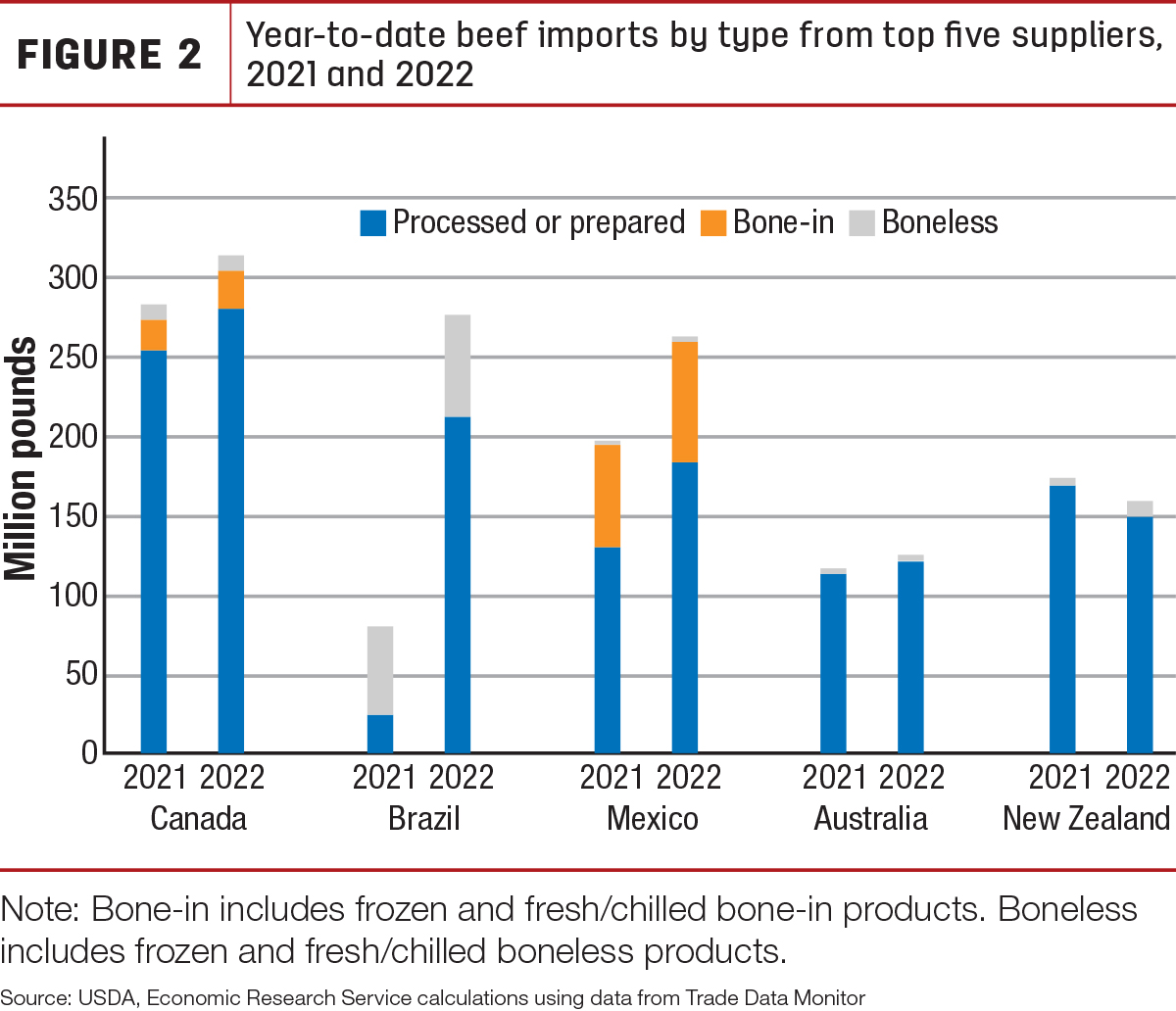

Most of the increase in 2022 year-to-date imports is boneless beef from Brazil. As shown in Figure 2, these imports are more than eight times higher so far in 2022 than the same period last year.

Historically, Brazil has been a major supplier of heat-treated or prepared beef products, but imports of fresh beef from Brazil have rapidly increased since the U.S. ban on fresh beef from the country was lifted in February 2020.

Imports of boneless beef from Mexico and Canada have increased as well. Mexico and Canada are also the major suppliers of imported bone-in beef products, but boneless beef remains the vast majority of what the U.S. imports. This beef is often destined to be blended with higher-fat-content trimmings to produce ground beef with the desired lean-to-fat ratios.

Year-to-date imports from Australia are higher than a year ago but still below the five-year average. Imports from New Zealand are down 8% year-over-year. Labor challenges, logistical issues and the low underlying cattle supply are hindering processing capacity and limiting exportable supplies.

The second-quarter import forecast remains unchanged from the previous month at 890 million pounds. Based on fewer expected exportable supplies from Oceania, the third- and fourth-quarter import forecasts are lowered 20 and 10 million pounds, respectively. The annual 2022 forecast is 3.515 billion pounds, a year-over-year increase of 5%. The annual forecast for 2023 remains unchanged from the previous month at 3.2 billion pounds.