In November, slaughter was higher year-over-year. While the increase in total cattle slaughter can be attributed to the additional slaughter day in November 2021 relative to a year prior, the average pace of fed cattle slaughter was higher on a per-weekday basis, with Saturday slaughter averaging lower.

Likewise, the pace of non-fed cattle slaughter was higher on a weekday basis but lower on a Saturday basis. The preliminary estimated federally inspected cattle slaughter for November was up 5.4% from a year prior. According to the USDA Agricultural Marketing Service (AMS) Livestock Slaughter report, the actual slaughter for beef cows and dairy cows for the weeks of Nov. 1 through Nov. 27 were up 5.9% and 2.3% compared to a year earlier. More noteworthy was the increase in heifer slaughter, which was also up 3.8% during the weeks of Nov. 1 through Nov. 27 compared to a year earlier. As a result, minor adjustments were made to the fed cattle slaughter estimate based on current slaughter data. However, both steer and heifer carcass weights increased during November and are approaching 2020 levels.

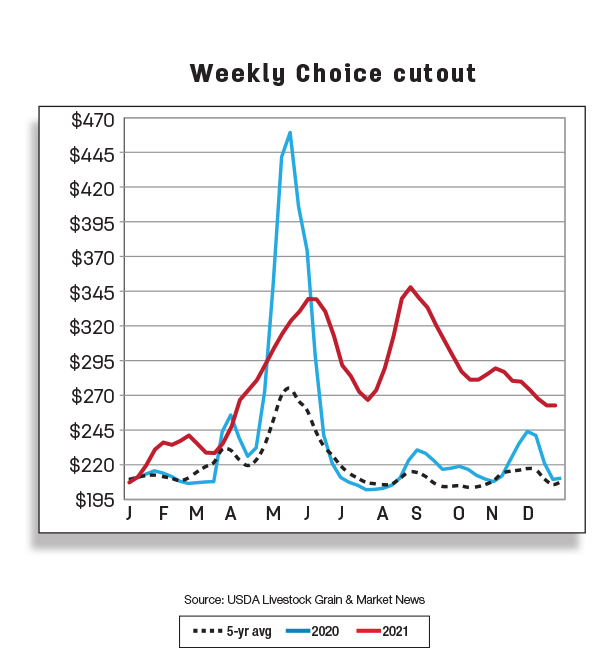

The forecast for 2021 beef production is raised on higher expected slaughter of fed cattle and slightly heavier carcass weights. December’s beef production forecast totaled 27.895 billion pounds, up 10 million pounds from the previous month. The forecast for 2022 beef production is unchanged from a month ago at the time of this writing at 27 billion pounds.

Fed steer and feeder steer prices raised in fourth-quarter of 2021 and 2022

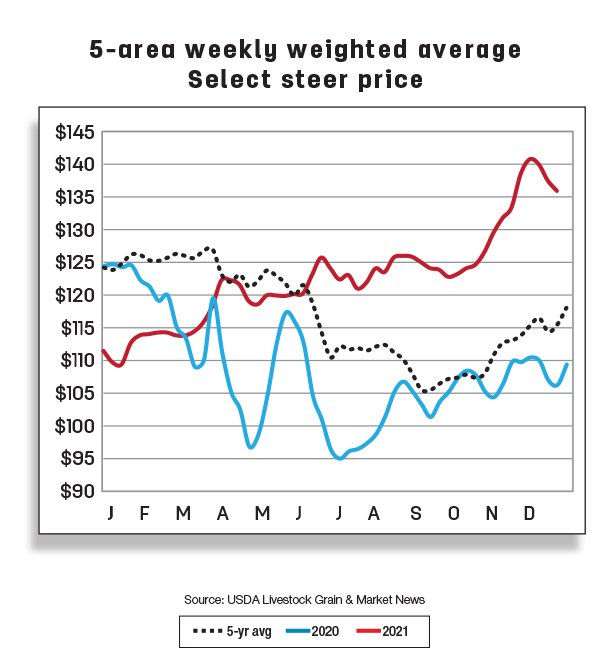

In November 2021, the average price for all grades of live steers sold in the 5-area marketing region was reported at $133.39 per hundredweight (cwt), $9.06 higher than the previous month’s average price and $24.54 above November’s 2020 average price per cwt. For the week ending Dec. 12, the fed steer price averaged $139.69 cwt, down 75 cents from the previous week’s price. The fourth-quarter price forecast for fed steer was raised $5 to $133 per cwt on continuing strength in beef demand and tight cattle supply. These conditions resulted in the 2021 annual forecast for fed steers being raised $1.25 to $122.56 from the previous month and the 2022 annual forecast raised $5 to $135 per cwt.

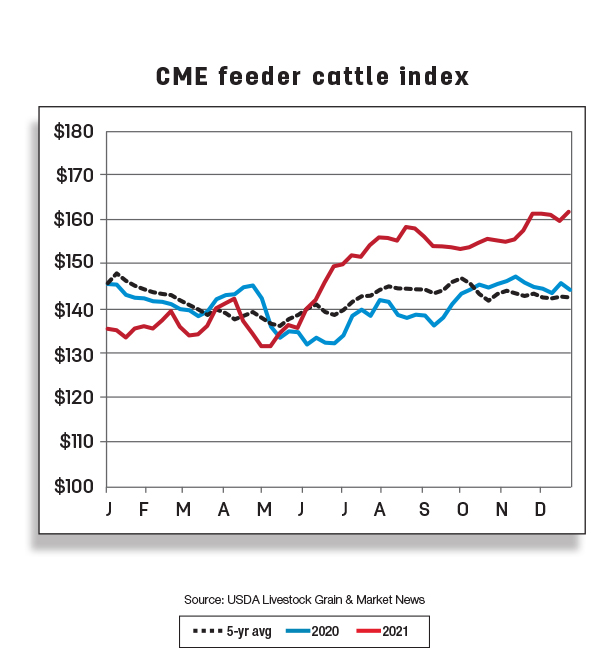

November’s average price for feeder steers weighing 750 to 800 pounds sold in the Oklahoma City National Stockyards was $159.74 per cwt, up $6.22 from the previous month’s average price and $21.52 per cwt from November 2020. For the week of Dec. 6, the average feeder steer price was $168.52 per cwt, up $4.47 from a week earlier. The 2021 fourth-quarter forecast was revised up $5 to $159 per cwt relative to the previous month on current price strength and improved prospects for winter grazing. The 2021 and 2022 annual forecasts were raised from a month earlier to $146.80 and $159 per cwt, respectively.

Beef imports up in October; 2021 and 2022 import forecasts raised

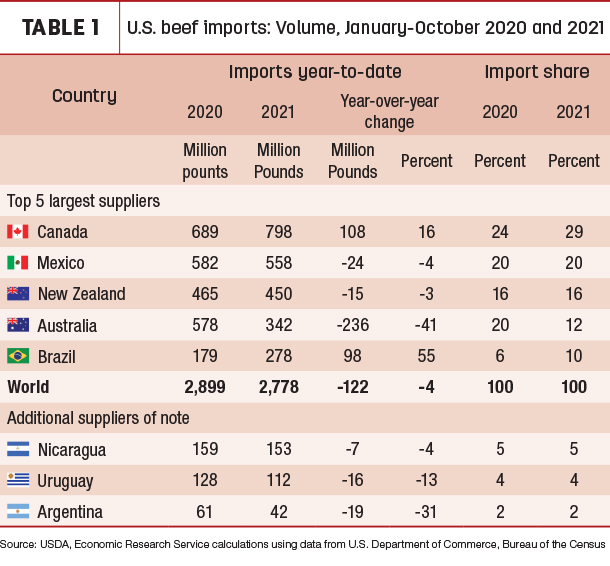

Beef imports totaled 293 million pounds in October, up 17% year-over-year and 22% higher than the five-year average. This was the second-largest import estimate for the month of October, behind 2004. Total year-to-date imports were 4% behind the same period a year earlier but 5% above the five-year average.

There were notable year-over-year increases in monthly imports from Mexico, Brazil, Canada and New Zealand. Imports from Mexico were nearly 42% higher year-over-year at 60 million pounds, the largest shipment for the month and eighth-largest overall. Imports from Brazil had a year-over-year increase of over 21%, setting a record high of nearly 38 million pounds.

As Table 1 shows, year-to-date imports from Canada and Brazil have increased by 16% and 55%, respectively.

So far this year at the time of this writing, Canada has supplied nearly 29% of beef imports compared to 24% the previous year. Brazil has increased its beef import share by 4 percentage points, accounting for 10% of U.S. beef imports in 2021. Year-to-date imports from Australia are nearly 41% behind the previous year, a share of only 12% of total year-to-date imports compared to 20% in 2020.

The fourth-quarter beef import forecast was increased by 55 million pounds to 830 million pounds due to stronger-than-expected October imports and continued strong domestic beef demand. Annual imports for 2021 were increased to 3.315 billion pounds. The beef import forecast for 2022 was increased to 3.265 billion pounds, reflecting stronger supply availability from Oceania that can enable a move closer to historic import levels from that region.

Asian markets extend record pace of U.S. beef exports

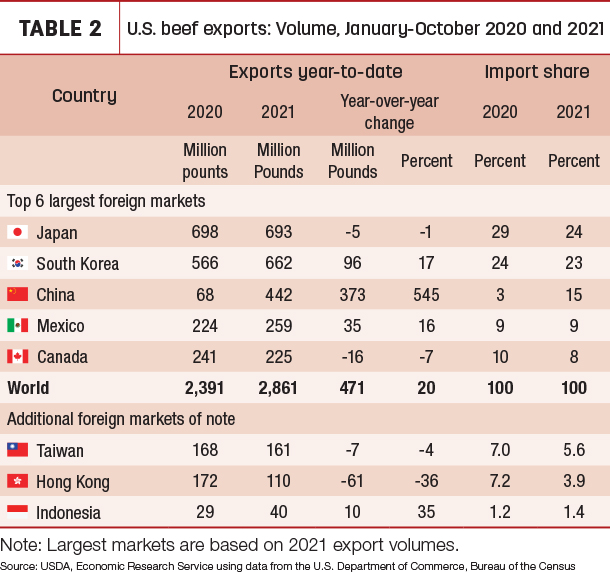

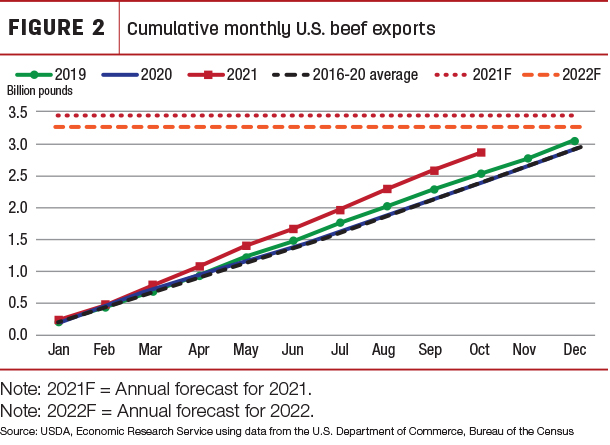

In October, U.S. beef exports were 281 million pounds, 9% above a year earlier and 11% above the five-year average. Among major destinations, larger year-over-year shipments to China, South Korea and Japan more than offset reduced exports to Hong Kong, Mexico, Canada and Taiwan. As Table 2 shows, cumulative exports for January to October reached 2.861 billion pounds, up almost 20% from a year prior and the five-year average.

Exports to China reached over 47 million pounds in October and 442 million pounds year-to-date, exhibiting the largest year-over-year and year-to-date volume increase. Compared to the previous year, shipments to China soared, moving it from the seventh- to the third-largest export destination and nearly surpassing combined shipments to Mexico and Canada. This is largely a function of several ongoing factors, including changes to U.S. market access that were implemented in March 2020.

China’s demand for animal protein is expected to continue to support beef imports. U.S. beef shipments to South Korea set a record for October, and South Korea’s aggregate beef imports from the world through October remain at their highest recorded levels. During the same period, U.S. beef sales to Japan were 5% higher in October from the previous year, bringing year-to-date shipments almost to 2020 levels.

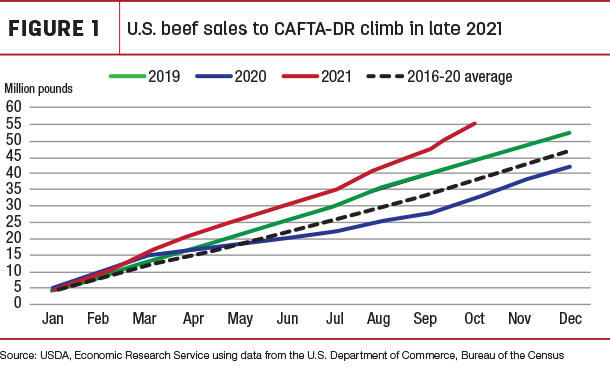

U.S. beef exports to member countries of the Dominican Republic-Central America Free Trade Agreement (CAFTA-DR) are at a record pace. The members consist of Costa Rica, Guatemala, Honduras, Nicaragua, El Salvador and the Dominican Republic (DR). Total beef exports year-to-date to these countries are up 69%, or 23 million pounds, from the previous year. Separately, exports achieved historic levels to Guatemala, Costa Rica, Honduras and El Salvador. The DR is typically the largest destination for U.S. beef in the region, but in 2021 Guatemala surpassed the DR by 22%, or almost 4 million pounds, despite the DR’s return to beef import levels pre-COVID-19.

Although U.S. exports to Mexico in October were down 13% from a year ago, year-to-date shipments are up 16%.

Based primarily on continued strong shipments to Asia, the forecast for beef exports in 2021 was unchanged from the previous month for a total of 3.455 billion pounds, 17% over the previous year and 18% above the five-year average. The 2022 beef export forecast was also unchanged at 3.27 billion pounds, a decline of about 5% into 2022.