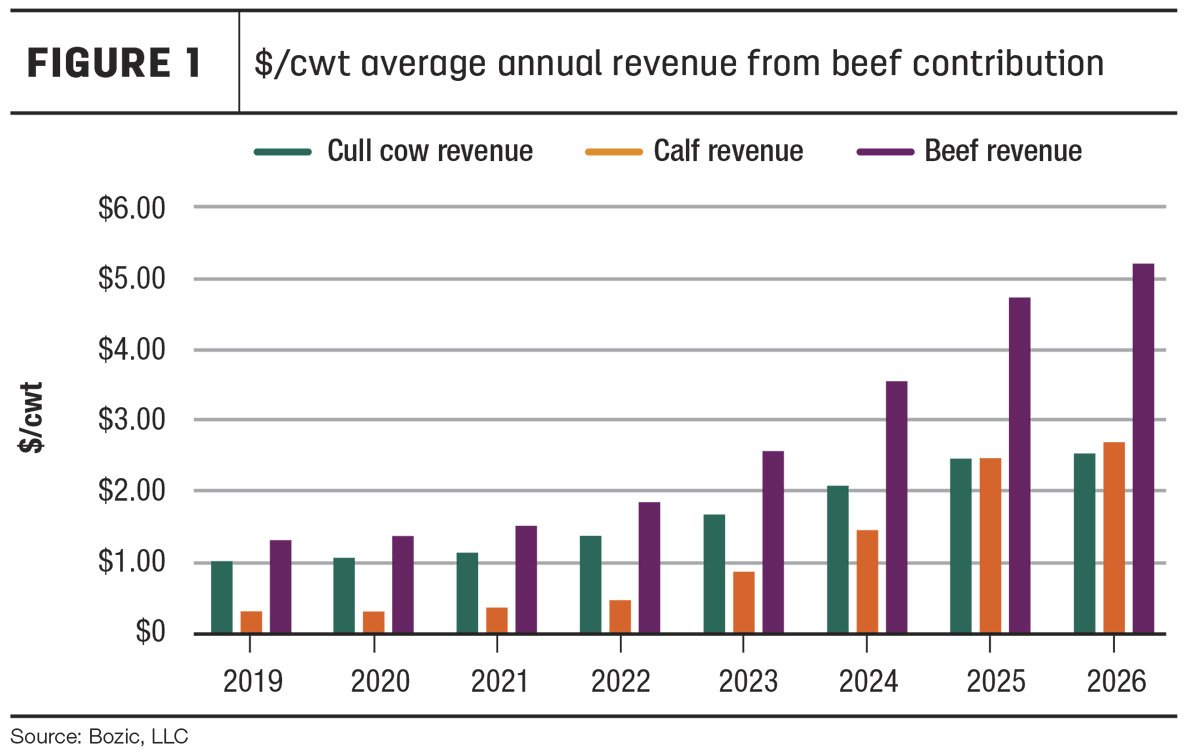

While milk drove nearly all revenue decisions on dairy operations for decades, that dynamic is shifting. Dairy-beef cross calves produced through beef genetics and the steady contribution of cull cows have elevated beef revenue into a meaningful financial consideration. With beef from dairies contributing an estimated $5 per hundredweight of milk-equivalent revenue (Figure 1), exposure to beef price volatility now carries real weight in culling and calf marketing decisions. Managing the downside without limiting upside is now part of disciplined dairy risk management – precisely where Livestock Risk Protection (LRP) fits.

What LRP does – and what it doesn’t

At its core, LRP allows a producer to establish a price floor using national market prices derived from CME feeder cattle futures. If the ending value is below the selected coverage price, an indemnity is triggered. If prices move higher, the producer keeps the upside.

LRP strictly protects against price risk. It does not cover death loss, disease, performance or local basis differences. Think of it as protecting the value of calves or cows you plan to market for beef – not insuring the animals themselves.

LRP basics

- Daily offers are available when CME markets are open (except USDA Cattle on Feed report days).

- Coverage levels range from 75% to 100% (Table 1).

- Premiums are subsidized and billed after coverage ends (about two months after the end date), which helps keep cash flow predictable (Table 1).

- You can cover as few as one head under an endorsement.

- Program head limits are large enough for most dairies: up to 25,000 head per crop year per type (e.g., 25,000 feeder-type and 25,000 fed-type).

The three LRP use-cases most dairies care about

LRP can be used in several ways, but most dairies fall into three practical categories:

- Day-old dairy-cross calves (unborn calves type): Coverage is intended for calves sold shortly after birth (within two weeks).

- Raising dairy-beef cross calves to feeder weights: If you retain ownership and market calves later (for example, 700 to 800 pounds), LRP feeder cattle types can establish a floor on that feeder value.

- Cull cows: Cull cows represent a steady, year-round revenue stream for dairies, and LRP can protect that revenue from broad national price declines.

Expected prices vs. settlement: The key distinction

This is the single most important concept to understand: LRP’s expected prices are set using CME feeder cattle futures, but settlement is based on a published index at the end of the endorsement.

For feeder cattle types (including unborn calves), the ending value is derived from the CME feeder cattle index. For cull cows under the fed cattle endorsement, the ending value is also tied to the CME feeder cattle index, adjusted by a published factor. (Fed cattle with the type of steers and heifers are a separate category that settle to a USDA AMS cash price report.)

In short: You are buying protection tied to national market price levels, not your local basis.

Why price adjustment factors exist

LRP pricing starts from a CME reference, but real cattle values differ by sex, weight and type. The marketplace typically assigns a higher value per hundredweight to steers than heifers and, on a per-hundredweight basis, values lighter cattle more than heavier feeders. To align with these marketplace differences, LRP uses price adjustment factors (PAFs) that adjust the CME-based reference up or down depending on the insured type and target weight.

The practical takeaway is simple: The daily offer price already reflects the correct PAF for the type you select, and the ending value used for settlement is adjusted in the same way. For feeder cattle types (such as calves being raised to feeder weights), these factors remain consistent. For unborn calves and cull cows, PAFs update monthly to reflect prevailing market relationships.

Coverage length: Why it matters for risk management

Endorsement length is where strategy really shows up:

- Cull cows: Currently limited to a 13‑week endorsement

- Unborn calves/day-old calves: Can be covered further out (from 13 weeks up to 39 weeks)

- Raising dairy-beef crosses: Feeder cattle types range from 13 weeks out to 52 weeks

The ability to purchase coverage further into the future can be powerful: It allows producers to hold favorable price levels in place longer, and the further out coverage extends, the greater the chance that adverse market forces could push prices lower while protection is in effect.

Cull cow coverage is a newer addition to the LRP program and is currently limited to 13-week endorsements. As illustrated in Figure 2, adoption has trailed unborn calves – likely because producers cannot extend coverage further out. While short-term protection can still provide value, longer endorsement options would improve effectiveness and support broader adoption over time.

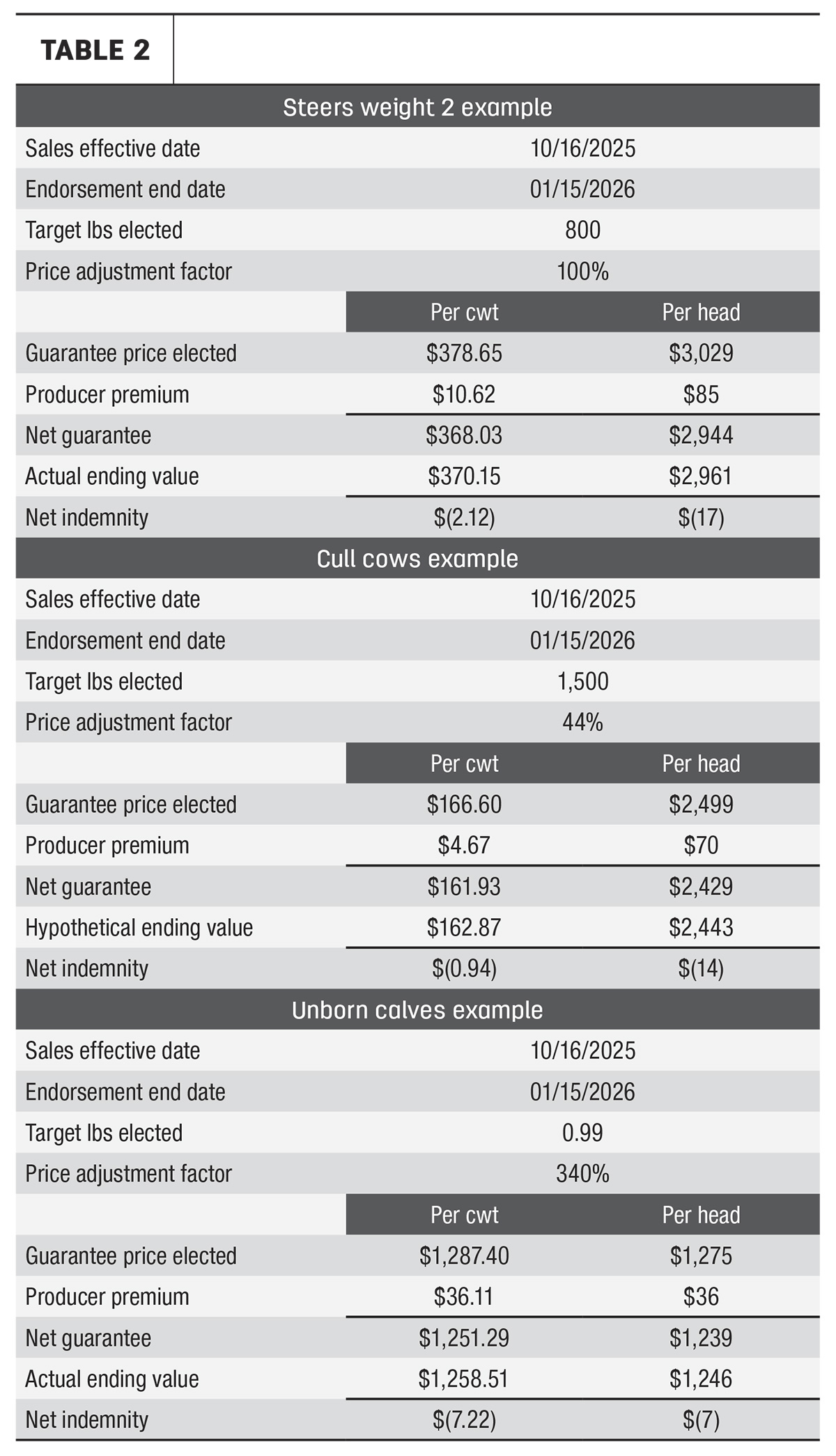

A practical dairy example: How quickly markets can move

To mirror how dairies manage multiple beef revenue streams – and to illustrate how quickly market sentiment can change – consider the following example. In mid-October 2025, cattle markets were supported by strong fundamentals and historically high prices. However, public statements from President Trump signaling a desire to sharply reduce beef prices introduced policy uncertainty and quickly unsettled the market. Prices declined sharply before rebounding almost as fast (Figure 3), underscoring how rapidly outside forces can reprice risk – even when underlying supply-and-demand conditions remain intact.

Against that backdrop, consider a hypothetical producer who, on Oct. 16, 2025, purchased three LRP endorsements on the same sales date, each with an end date of Jan. 15, 2026 (13 weeks). The producer was protecting three distinct beef revenue streams commonly found on dairy operations:

- Steers weight 2: Dairy-beef cross calves being raised to approximately 800 pounds

- Unborn calves: Day-old dairy-beef cross calves sold shortly after birth

- Cull cows: Dairy cows leaving the herd after extended milk production

Each endorsement reflects how the marketplace values different cattle types, which is why different PAFs apply across the examples. Unborn calves carry a substantially higher adjustment relative to the CME feeder cattle reference, feeder steers align more closely with the benchmark, and cull cows reflect a lower relative value. While the pricing mechanics differ, the risk protection logic is identical across all three: If the ending value falls below the selected coverage price, LRP pays an indemnity based on the difference multiplied by the insured weight and head count.

Prices declined meaningfully following the initial market reaction but mostly recovered before the end of the coverage period. In these examples (Table 2), indemnities were ultimately minimal or unnecessary because the market rebounded. However, the value of the coverage was not the payout – it was the protection. Having LRP in place allowed the producer to avoid potentially costly, reactionary decisions during a period of heightened volatility, such as forward contracting cattle at depressed prices or altering marketing plans in response to short-term fear.

Final thoughts

LRP is not about predicting the next market move. It is about recognizing that modern dairies now carry meaningful revenue risk in beef – through both dairy-beef cross calves and cull cows – and that risk can show up quickly.

For dairies that have made beef genetics and cull cow management part of the revenue plan, LRP offers a straightforward way to protect what has already been earned while staying fully open to stronger markets. That balance – protection without limitation – is why LRP deserves a place in today’s dairy risk management conversation.

This article is provided for information purposes only. Readers should consult their own professional advisers for specific advice tailored to their needs. Information contained in this article may be subject to change without notice.