Overall, the 2025 beef production forecast is raised fractionally from last month’s projection by 15 million pounds to 26.7 billion pounds. Compared to last month’s forecast, fewer steers and heifers are expected to be processed this year, but that decline is more than offset by an adjusted outlook for cow and bull slaughter and for heavier carcass weights in each quarter. Specifically, fewer fed cattle in the slaughter mix are anticipated in the second and third quarters, reflecting a slower projected pace of slaughter based on fewer placements in the first quarter than previously thought.

The latest Cattle on Feed report, published by the USDA National Agricultural Statistics Service (NASS), showed a March 1 feedlot inventory of 11.577 million head, 2% below the 11.838 million head in the same month last year. Feedlot net placements in February were 19% lower year over year at 1.494 million head and lower than most analysts projected. However, when factoring in the year-over-year increase in January, the total volume of net placements for January and February combined was 8% lower than the same period last year. Of note, February had one less weekday than last year. Marketings in February were 1.633 million head, down 9% year over year, though on a weekday basis the pace was 4% behind last year. The slower pace of marketings likely occurred due to weather impacting packer operations and movement of cattle.

Carcass weights in the first quarter are raised on slaughter data through March as reported by the USDA Agricultural Marketing Service (AMS). The first quarter saw the largest proportion of steers and heifers in the slaughter mix since 2006 and the heaviest fed cattle carcass weights for this time of year. Subsequently, it elevated average carcass weights for total cattle slaughtered to all-time highs for any quarter. For the remainder of the year, weights are raised on a slightly slower pace of slaughter, suggesting the percent of fed cattle on feed over 150 days will likely remain relatively high.

Tight supplies and beef demand are fundamental to price support

In March, the weighted-average price for feeder steers weighing 750 to 800 pounds at the Oklahoma National Stockyards was $283.18 per hundredweight (cwt), more than $31 above March 2024. According to the April 7 auction report for the Oklahoma National Stockyards, feeder steer prices dropped roughly $20 from the previous week to $270.90 per cwt. For that sale, receipts were down sharply relative to recent weeks due in part to inclement weather. As a result, not much weight was given to this price drop in early April.

Despite market volatility and the futures market indicating lower prices in the deferred contracts during the week of April 7, economic fundamentals with tight cattle supplies still play a role in supporting prices in the outlying quarters. Based on weekly data from the USDA AMS National Feeder and Stocker Cattle Summary report, sales of feeder and stocker cattle in the first two months are down 15% from the same period in 2024. This is likely due to a 75% year-over-year decline in feeder cattle imports due to restrictions on cattle from Mexico over the first two months of the year. This has led to feedlots in Kansas and Texas placing 5% and 21% fewer cattle, respectively, in January and February compared to the same period last year. Although the weekly volume of feeder cattle imports from Mexico is expected to improve moving forward, annual volume is projected below year-ago levels.

Based on price data through early April and weaker expected first-quarter placements, the second-quarter forecast is raised by $7 to $280 per cwt. Prices in the third and fourth quarters are raised $8 and $7 from last month to $282 and $286 per cwt, respectively. These changes raise the annual feeder steer price to $281.03 per cwt, a 12% increase from last year.

Slaughter steers in the 5-area marketing region averaged $207.96 per cwt in March, more than $20 above 2024. At publishing, weekly prices appear to have put in an early spring peak during the week ending with March 23 at $212.76 per cwt, which has been supported by record wholesale prices for this time of year. With first-quarter production at 99.8% of last year, wholesale prices suggest that demand remains robust through early 2025.

However, for the rest of the year, the 2025 forecasts for U.S. beef exports are lowered from last month by more than the reduction in beef imports, which is increasing per capita availability of beef in the U.S. Although this could soften support for slaughter steer prices in the outlying quarters, supply fundamentals and current price strength bolster the outlook for slaughter steer prices, which is raised from last month. Further, weekly comprehensive wholesale beef prices are showing quite a bit of strength ahead of what is typical in the run-up to the spring grilling season in April and early May. In the outlying quarters, the forecasts are raised $6, $8 and $7 from last month’s forecast for an annual price of $205.51, nearly 10% above 2024.

Uncertainty in global trade conditions lowers both import and export forecasts for 2025

U.S. beef exports in February were 227 million pounds, 7% lower year over year. Monthly exports to China, Mexico, Taiwan and Japan were all lower year over year. Exports to Canada were 3 million pounds higher year over year, nearly 17%, while exports to South Korea were also slightly higher, up 2%. Table 1 shows year-to-date exports compared to the same period a year ago. Total exports are down 4% so far this year, but year-over-year changes in exports to the top markets are mixed.

Although year-to-date exports to China are higher year over year through February, U.S. export sales to China have dropped off severely in March as the General Administration of Customs of China (GACC) allowed the registration of most U.S. beef export facilities to lapse in mid-March. Without updates to the registration list, a significant portion of U.S. beef production is ineligible to be exported to China. Additionally, any remaining product that would be eligible for export to China would now be subject to retaliatory tariffs, in addition to the previously effective tariff rate of 12%. These factors, which are assumed to remain in place, are expected to severely restrict U.S. beef exports to China.

In 2024, exports to China represented 16% of total U.S. beef exports, the third-largest export market for U.S. beef. With exports projected to substantially decline to that market this year, some exports that would have otherwise gone to China may be redirected to other markets such as Japan and South Korea. However, with economic headwinds already facing U.S. beef exports in these markets, there may not be sufficient demand to absorb all of the product, given the high prices. Therefore, the beef export forecast for 2025 is decreased by a total of 135 million pounds. The second-quarter forecast is lowered 55 million pounds to 675 million, and the third and fourth quarters are lowered 45 and 35 million pounds, respectively. The new annual forecast for 2025 is 2.685 billion pounds, which if realized would be an 11% decrease year over year.

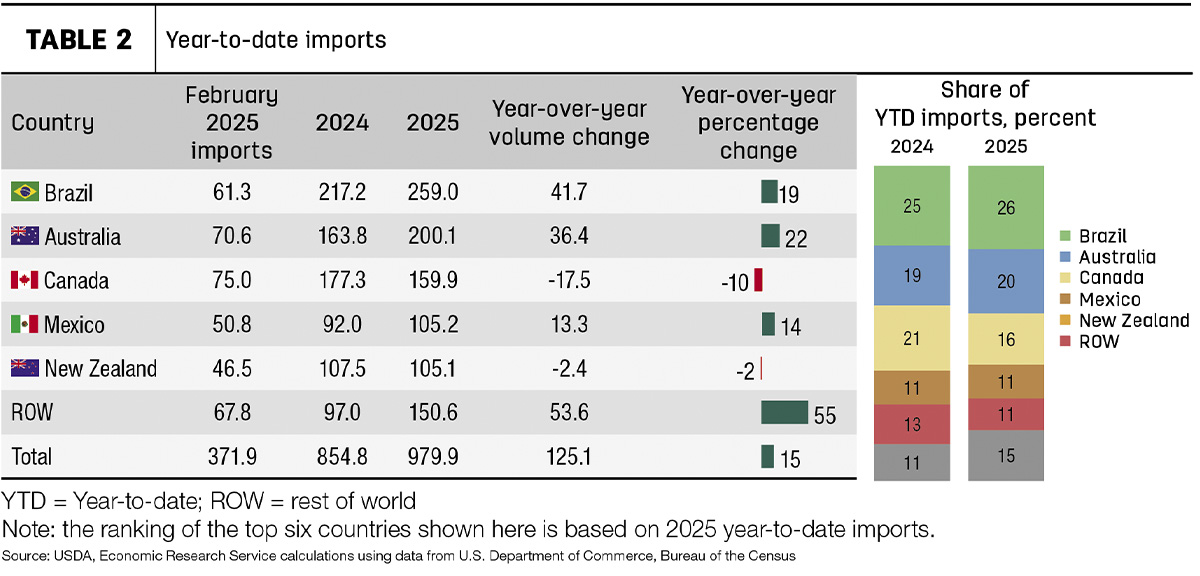

On the import side, total U.S. beef imports are running higher year over year, mostly due to the record imports in January, though imports in February were also higher year over year (up 6%). The main contributors to this increase are shown in Table 2; imports from Brazil, Australia and countries outside of the top five suppliers are significantly higher year over year through February. Due to the strong pace of imports so far, the forecast for first-quarter imports is raised 30 million pounds to 1.36 billion.

Prices for imported frozen 90% lean trimmings were more than $52 per cwt (20%) higher year over year in February, exhibiting strong demand for imported beef. However, starting in April, there will be an additional 10% tariff on all beef imports from most major suppliers. Beef imports were already subject to a tariff-rate quota, so imports from countries that have already filled their quota face a 36.4% tariff (overquota tariff of 26.4% plus 10% reciprocal tariff). Such is the case for countries that import beef under the other countries quota (i.e., Brazil and Paraguay), which was filled in January. The additional tariffs will likely make imported trim more expensive. However, with cow slaughter (which results in product comparable to imported lean trimmings) forecast to decline 8% year over year, the demand for imported trimmings will likely remain strong.

Due to the expected increased price of imported beef, the U.S. beef import forecasts for the second, third and fourth quarter are lowered 10, 15 and 20 million pounds, respectively. The net change to the annual forecast is a decrease of 15 million pounds to 4.86 billion. This would still be a year-over-year increase of nearly 5%.