There have been large amounts of price movement for feeder cattle this spring and summer due to a variety of factors, including strong domestic retail and export beef demand, meat processing issues, a run-up in feed prices, worsening drought conditions and the loosening and retightening of local COVID-19 restrictions. All of these have combined to change buyers’ expectations of future beef demand and, subsequently, what they are willing to pay for feeder cattle this fall.

Forward contracting feeder cattle is one way buyers can control costs and thus manage overall operation profitability. Video auctions provide a market for both buyers and sellers to transact cattle to be delivered at a future date at a given price and weight subject to a price-weight slide adjustment at delivery based on actual pounds of production delivered. These video auction prices are publicly reported by the USDA Agricultural Marketing Service (USDA-AMS) and provide one source of market information for what feeder cattle buyers’ expectations are in fall 2021 and hint toward what local sale barn auction prices will be.

Video auction prices

So what are video auctions telling us about potential expected feeder cattle cash prices in fall 2021, and how does this vary by type of feeder cattle, region and delivery month? I answer this using publicly available data taken from USDA-AMS from Superior, Northern, Western and Torrington Video Auctions between January 2021 and August 2021. I restrict my focus to steers or heifers, muscle grade 1 or 2, either a large or medium frame that is set to be delivered in either September, October, or November and is not associated with price discounts or premiums.

Cattle type differences

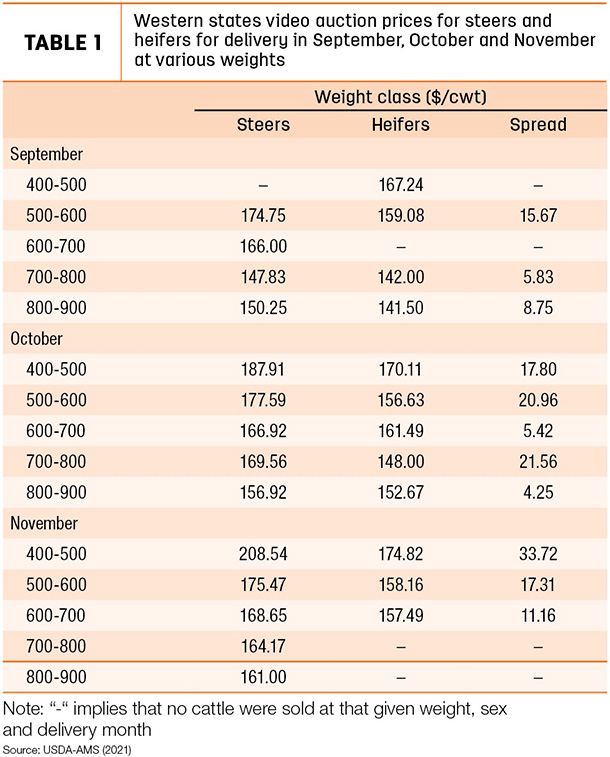

Video auction prices for steers and heifers by various weights and delivery months for the West region are displayed in Table 1.

Blank cells indicate that either steers, heifers or both were not transacted at that given weight and delivery month.

The steer-heifer spread varies considerably both across delivery months and weights. For example, for steers delivered in October between 400-500 pounds, the spread is approximately $18 per hundredweight (cwt), whereas the spread is approximately $34 per cwt in November. Overall, steer-heifer spreads are larger for months farther in the future relative to closer months. This is likely because of a larger-than-average heifer cattle supply this fall as herd liquidation continues due to low prices and drought conditions, reducing incentives for heifer retention.

Regional differences

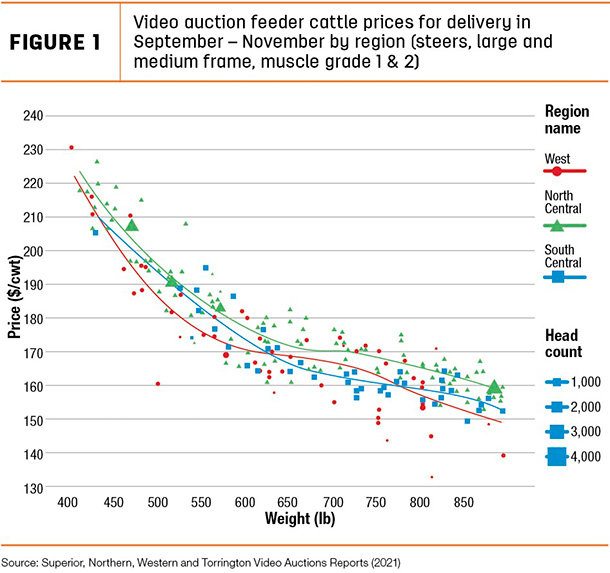

Figure 1 plots individually observed transactions segmented by region.

Prices are only reported for steers for ease of presentation, but heifers have similar findings. Points represent individual lots sold at a given weight-price combination. The size of the dot represents the number of head within the sold lot. Larger dots indicate more cattle in the lot for a given weight-price point. The solid line represents the estimated price-weight slide, showing that the heavier feeder cattle are, the less per pound is paid.

To find out what the video market could pay, on average in each region, find a specific weight on the horizontal line, go up until you reach the region’s sold color line and then trace it to the left until the vertical line to find the price. This can provide some signal for what the price will be in a specific region by the weight of steer sold.

Notice that there is significant variation in the prices received by region and weight. So while the solid line represents an average price, some feeder cattle received prices that were higher or lower than this. On average, cattle are priced relatively higher in the North Central region relative to the West and South Central region. In the West and North Central region, premiums are being given for 625- to 725-pound cattle, on average, across all delivery months relative to what the price-weight line theoretically should be. This is likely due to feedlots in the Northern Plains wanting to place heavier cattle to limit the number of days cattle are on feed, thus lowering their overall cost of gain.

Delivery month differences

Averaging prices across regions within sex, weight and delivery month can provide a broad signal for when buyers of feeder cattle want cattle delivered. Currently, across most weight classes by sex, there are higher premiums for cattle delivered in later months than closer months.

For example, prices for feeder steers 500-600 pounds are greater in November relative to September by about $8 per cwt, or 5% higher. This suggests that buyers of feeder cattle are wanting cattle to be delivered in later months and are willing to pay a premium to feeder cattle producers to do so. These premiums are much smaller for heifers relative to steers, suggesting a lower desire to have heifers delivered in later months.

Implications

This fall, numerous factors are impacting the price received for feeder cattle by weight, sex, region and delivery month. Producers choosing to retain feeder cattle post-weaning should calculate the value of gain (VOG) and compare it with their operations’ cost of gain (COG), recognizing that the added value of gain only comes when the VOG is greater than the COG.

For producers selling at weaning, currently there are larger discounts for weaning later relative to earlier. Matching labor requirements, weather and cattle conditions to this can potentially yield higher dollars per pound weaned.

Prices reported are video auction prices for cattle that are set to be delivered in the future. Local markets can change quickly to news and market information, so paying particular attention to the short-term dynamics in your local area before bringing cattle to auction is always recommended.