It is commonly believed that the disastrous dairy farm income situation in 2009 was caused by a “collapse in demand,” especially in the export markets for U.S. dairy products. This is not correct. Total dairy product consumption, both domestic and international, actually grew strongly in 2009. What collapsed was the U.S. dairy industry’s ability to compete in the growing world market in 2009. The resulting collapse in U.S. milk prices was deeper and lasted longer for U.S. dairy farmers than it would have if proper export marketing tools had been available. The immediate cause of the problem in 2009 was a 1.7 percent drop in total commercial disappearance of U.S. dairy products resulting from a 22 percent drop in commercial exports.

Since the U.S. dairy industry shares the U.S. domestic market with dairy imports, a closer look at U.S. domestic commercial disappearance shows that imports dropped in 2009, allowing the U.S. dairy industry’s domestic sales to grow by 1.5 percent.

A 1.5 percent increase in the U.S. dairy industry’s sales in the domestic market may be more modest than desired, but the U.S. domestic market is a mature market, and total sales in that market have generally not grown much faster than population in recent years, about 1 percent annually.

These numbers show that sales volume in the domestic market cannot reasonably be considered to be the cause of the 2009 U.S. dairy crisis. Nor can dairy imports be the cause, since they dropped by over 12 percent that year.

In terms of growth in import volumes from 2008 to 2009, excluding U.S. imports, growth in all major product categories were:

• Butter: up 7 percent

• Cheese: up 2 percent

• Skim milk powder: up 9 percent

• Whey and lactose: up 18 percent

• Whole milk powder: up 9 percent

These numbers show that a drop in worldwide dairy import sales volume cannot reasonably be considered to be the cause of the 2009 crisis either.

So, if declining sales in the domestic and international dairy markets was not the problem in 2009, what was? In particular, what caused the big loss of U.S. dairy exports that year?

Basically, a drop in world dairy product prices, which resulted in a major loss of international market share for U.S. dairy product exports.

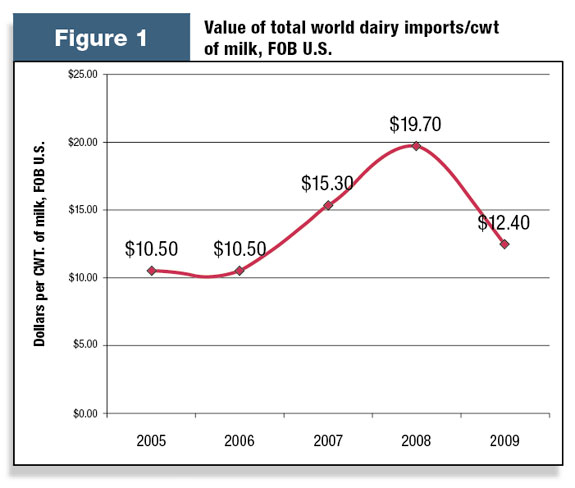

Figure 1 shows the total value, per hundredweight (cwt) of milk equivalent, of all world dairy product imports during 2005-2009, less product manufacturing, transportation and all other costs required to supply those imports from the U.S.

The figure represents the price U.S. dairy farmers would have received for milk used to manufacture and export dairy products if they were paid for that milk based only on the average value of those products in world trade.

Figure 1 illustrates clearly the events in world markets during the past several years.

• Strong demand growth outpaced available supplies.

• This boosted prices dramatically in 2007 and 2008.

• This resulted in buyer resistance.

• Competing exporters aggressively cut prices to maintain export sales and avoid building inventories.

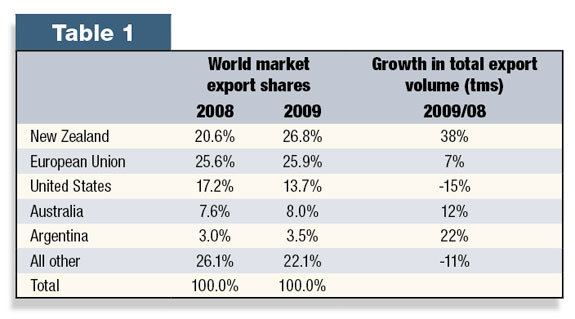

Table 1 shows the results of this pricing strategy followed by the major dairy export suppliers during 2008 and 2009.

It shows that four of the five major dairy exporters managed to increase both their export volumes as well as their total export shares of the world market in 2009, while the U.S. suffered major losses in both.

The 3.5 percentage-point loss of world market share the U.S. suffered in 2009 represented the loss of about 4 billion pounds, milk equivalent, of commercial export sales that year.

The other major world dairy suppliers – the European Union, New Zealand and Australia – managed to increase their exports in the face of sharply lower prices in 2009 and thus reduce or avoid burdensome product inventory buildups.

The U.S. was forced into an opposite course, reducing cow numbers and dealing with inventories through government action.

The resulting adjustment lasted much longer and destroyed U.S. dairy farmer equity far more than if the industry had been able to maintain export volumes in 2009. Almost two years after the world price collapse in late 2008, U.S. milk prices are still impacted by high cheese inventories.

This analysis strongly suggests that CWT might have been more effective in 2009 by maintaining product exports at least equivalent in volume to the number of cows removed.

Now that CWT herd retirements will not be continued, CWT could focus exclusively on the critical business of ensuring against the financially destructive erosion of U.S. export market share in the future.

U.S. dairy farmers can take an effective step to avoid a repeat of 2009 in the future by continuing an effective CWT export assistance program in 2011 and beyond. PD

Editor’s note: CWT is in the middle of a membership drive to increase participation in its export assistance program above 75 percent at a commitment level of two cents per hundredweight in 2011 and 2012.

Peter Vitaliano

Vice President of Economic & Market Research

National Milk Producers Federation

PVitaliano@nmpf.org