Since the last time we explored forward dairy production margins in the February 9 edition, much has changed in the market both for milk prices and feed costs. On a positive note, feed costs have held steady and are under fundamental pressure from larger crop estimates out of South America, as well as indications that acreage will be higher in the U.S. this spring. Moreover, domestic demand over the past quarter has not been as strong as previously expected. Unfortunately, milk prices have dropped sharply since mid-January, more than offsetting all of the benefit gained from steady to cheaper feed prices.

There were many reasons cited for the milk price decline. Cow numbers increased 3,000 head in January and February after steadily declining month-to-month through all of 2009. Since the beginning of the year, dairy cow slaughter has trended below a year ago, possibly due to early-year indications that forward profit margins were positive and discouraged further herd contraction. Meanwhile, American cheese stocks were higher at the end of February, up 2 percent from January and up 10 percent from a year ago. Moreover, milk-per-cow figures have increased as the herd has become more productive.

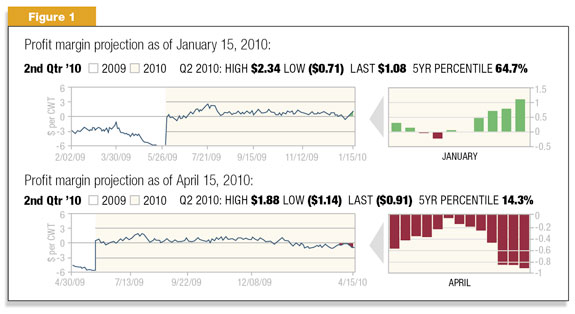

From a profit margin standpoint, projected dairy returns through the remainder of 2010 are actually lower now than they were when we last calculated them. As we begin Q2 2010, spot dairy margins are now projected at a negative $0.91 per hundredweight, meaning that you are currently losing money if you are simply selling milk and purchasing feed ingredients in the open market on a spot basis. As recently as mid-January, however, when we last calculated forward dairy returns for the February 9 edition, Q2 margins were projected at a positive $1.08 per hundredweight, meaning it was possible to secure a profitable margin for the now-current period as we begin the second quarter (see Figure 1 ).

While this may come as little solace reflecting on lost opportunities in hindsight, it is important to realize a fact mentioned in the last edition: Just because the market is projecting a profitable situation in a forward time period, there is no guarantee that you will earn a profit on your milk when that period rolls around. The futures market is dynamic and constantly changing in response to new information being discovered about the value of these component pieces of our profit margin. Just as margins can improve with changing futures prices, it is also important to remember that they can deteriorate quickly as well. Because of this, it is important to be proactive in protecting potential profits when the opportunity presents itself as it did back in mid-January.

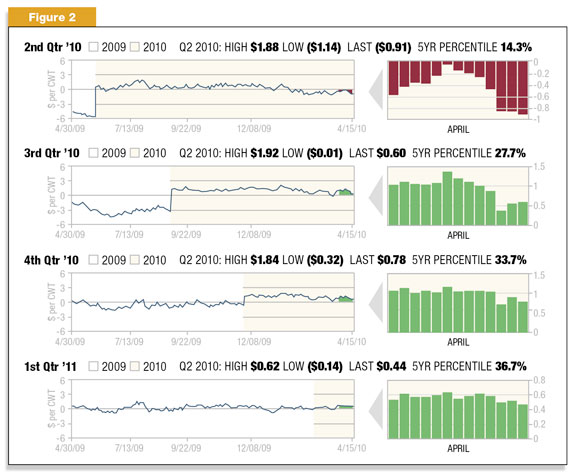

On a more positive note, deferred margins are still profitable although lower than they were back in mid-January. Looking at Q3 through Q1 2011, dairy margins range from a positive $0.78 per hundredweight down to a positive $0.44 per hundredweight. Again, these margins are now lower than where they were back in January and below average from a longer-term basis, but they are still positive and worth protecting

(see Figure 2 ).

Many dairy producers are obviously apprehensive about locking in a margin that is below average at best, albeit still positive. In general, one of the main concerns about forward contracting is the potential opportunity cost surrendered if milk prices were to increase, and/or feed prices decline after pricing. This very question came up recently at one of our educational programs in Chicago where a dairyman asked, “What if I don’t want to commit to a milk sale at current price levels but still want to protect the possibility of the price declining?” Fortunately, option contracts allow for the flexibility to protect a price level without the obligation or commitment involved with a forward or futures contract sale.

In the case of a forward or futures contract, you are essentially locking in a price level – either a milk sale or feed purchase. While you have the right to that price, you also carry the obligation associated with that price. For example, I have the right to sell milk at $14.50 per hundredweight for a deferred delivery based upon CME Class III milk futures. However, if the price were to eventually rise to $16 per hundredweight once it comes time to deliver my milk to the co-op or processor, I am committed to the sale previously established at the lower price and therefore do not participate in the benefit of being “open to the market.” Option contracts allow you to “unlock” the obligation associated with the right to a given price level – either a purchase or a sale.

Let’s say you still want to protect the $14.50 per hundredweight level as a sale price for your milk, but you want to retain the opportunity to participate in higher prices should the market eventually be trading at $16 per hundredweight once it is time to deliver your milk to the co-op or processor. As an alternative to simply “locking in” the price by forward contracting or selling futures, you could purchase a $14.50 put option, which would give you the right but not the obligation to sell milk for future delivery at that price level. In this case, because you are not obligated to the sale at higher prices, you benefit from any increase in price between the time you purchase the put option and the time you deliver your milk. In exchange for this added flexibility, you pay a premium for the benefit of only holding the right but not the associated obligation to your sale price.

The cost of this option will vary based upon the price level you are protecting, how much time you have to exercise your right and how volatile the underlying market is. If after factoring in the cost of the option’s premium relative to your projected forward profit margin, you can still sell milk profitably, this type of strategy can prove very effective in protecting your operation’s profitability without surrendering opportunity in the open market.

As an example, let’s assume you have just finished pricing your feed ingredients through the remainder of the summer until the fall harvest period, and based upon an average of the July/August/September Class III milk futures contracts, you are projecting a positive profit margin of $1 per hundredweight for Q3. Let’s further assume that you like this profit margin, but are concerned that it may continue to improve with rising milk prices into the third quarter. You know that you can purchase a milk put option that will protect the current price level of Class III futures for a cost of $0.70 per hundredweight. If you purchase this put option, you have basically locked in a “minimum margin” for your Q3 milk sales of $0.30 per hundredweight, which is equivalent to the projected profit margin of $1.00 minus the premium cost of the put option. There will remain a basis risk between the Class III milk futures price upon delivery and the mailbox price received for your milk, although you have effectively protected a majority of the forward revenue risk associated with an adverse price change.

In the above example you have already priced your feed ingredients, but what if you are open on those as well? A similar type of option strategy can be used to secure a “maximum price” on your energy and protein equivalents. Call options can be purchased against the corresponding corn and soybean meal contracts to secure the right, but not the obligation, to buy those contracts at a pre-determined price for future delivery. Here, you retain the opportunity to benefit from a lower feed cost should the market for those contracts decline between the time you purchase the call options and the time you eventually price your feed ingredients in the cash market. As in the milk example, you would want to determine how much premium expense for these options would mean in terms of your overall profit margin so that the opportunity you retain is acceptable for the cost you project to incur.

When you purchase options, either puts to secure a minimum sale price or calls to secure a maximum purchase price, the limit of your exposure is the cost of the premium. Because your profit margin is a combination of the difference between your milk revenues against your feed expenses, you need to calculate what this premium cost represents in terms of your maximum feed cost and your minimum milk sale. While a milk put will secure a minimum sale price at a pre-determined level (referred to as the “strike” price), you have to subtract the cost of the put option from this level to arrive at your true minimum milk price. Similarly, where a corn or soybean meal call option will secure a maximum purchase price at given level, you have to add the cost of the call options from this level to calculate your true maximum price for the corn or meal. Once you have calculated these costs, you can arrive at what a “minimum margin” strategy will secure for your overall profitability in a given period – for example, Q3 2010.

In some cases, the minimum margin strategy will still secure a profitable margin while allowing for improvement over time through a combination of higher milk prices, and/or lower feed costs. At other times, the net costs of these options will be greater than the projected forward profit margin such that it may be desirable to try reducing these costs through other strategy combinations. More complex combinations involve minimum/maximum price structures, ranges of protection, or potentially a combination of both. Regardless of the strategy specifics, it is important to think about your forward profitability in margin terms. Focusing on either costs or revenue in isolation can actually expose your dairy to greater risk than simply staying open to the market. Fortunately, there are many tools available to dairymen to effectively manage their profit margin over time in these volatile markets. PD

-

Chip Whalen

- Senior Risk Manager for Commodity & Ingredient Hedging

- Email Chip Whalen