For years, we have talked about markets and their behavior. We study supply and demand features. We discuss exports and trade policy. We analyze chart patterns and talk about technical influences. But there remains one element of the market seldom mentioned. There is a particular group of people often left out of the conversation – speculators.

At the very mention of speculators, immediate mental images and conditional responses come to the mind of each individual who dares to consider them. They are often given a bad rap. Comments such as, “They manipulate the market,” or “They don’t care about farmers,” or “They have destroyed our prices,” or “How can they be trusted?” are commonplace to many a discussion throughout rural America.

Given that many people have had little exposure to speculators or have a general lack of understanding of their actions or function in the market, it is easy to appreciate why such comments exist. So if you will grant me the opportunity, I will make an attempt to shed some light on this very important crowd of participants in today’s marketplace.

For decades, the broad offering of agricultural markets traded at the many different exchanges in our history stayed inside of a very narrow trade, almost a flat price range. Exceptions existed for special extreme weather events or significant geopolitical occurrences. Aside from such events, prices would be described by many as boring.

Trade began at the Chicago Board of Trade in 1848. The market was developed to provide buyers and sellers the wherewithal to create a forward contract in an effort to build a degree of predictability and certainty into their business. Leading up to the exchange’s existence, credit risk was a major concern for those who attempted to do this on their own.

By eliminating the counter-party risk and developing standardized contracts, the exchange was able to offer a mechanism which met the needs of those seeking to offset their perceived risk and establish pricing certainty.

But what if farmers sought a market to sell into at a time when buyers were uninterested in assuming the other side? In the past, this was a problem. Actual buyers of physical product were not always prepared to accept the prices sellers of product were demanding.

The inverse was also true: Sellers were not always willing to sell at prices where buyers stood ready with open arms. So who assumes this risk? Enter the speculator.

While their entry into the market was slow, the introduction of options in the 1980s, together with an ongoing growth in the world’s economy, brought more and increasingly sophisticated traders to our marketplace. Speculators were among them.

Decades later, this is still the trend. Instead of having to always have a buyer or seller of physical commodity on hand to take the other side of a trade, speculators stood ready to consider the opportunity.

The presence of a speculator brought pricing to a much more competitive place. Physical buyers would have to compete with speculators on the bid for product. Sellers would have to compete with the same speculators on the offer of product.

Their fight for a place in the price discovery process actually brought greater competitiveness and fairness to everyone’s efforts. Instead of manipulating a market, they have actually worked to make it more fair – not to mention more robust.

Consider Figure 1. Since the beginning of the new millennium, prices (blue bars) have been generally increasing, while the amount of trading volume (green and red bars) has also been increasing.

While milk prices are certainly a long way from the highs of 2014, they have also stayed well away from what used to be the pre-2K standard cycle lows at or below $10 per hundredweight.

Moreover, the manic trade of the early 2000s has become much tighter from day to day, week to week and month to month. In other words, there is less volatile trade in the short run, a sign of a market well balanced among buyers, sellers and the speculators willing to stand in between them.

That is not to say the market has lost its ability to move. Case in point: 2014. However, it is to say, regardless of what side of the market you stand on, there is a growing ability for you to find someone to take the other side of your deal without causing a disruption to the market.

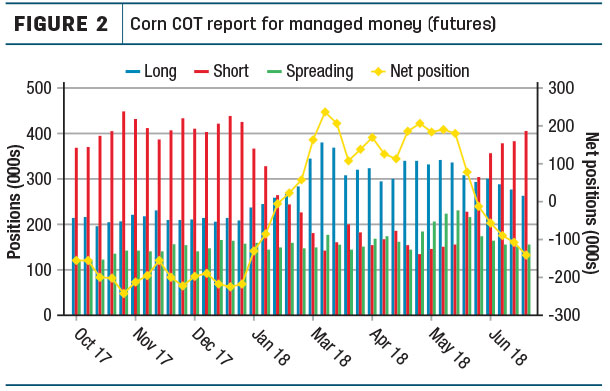

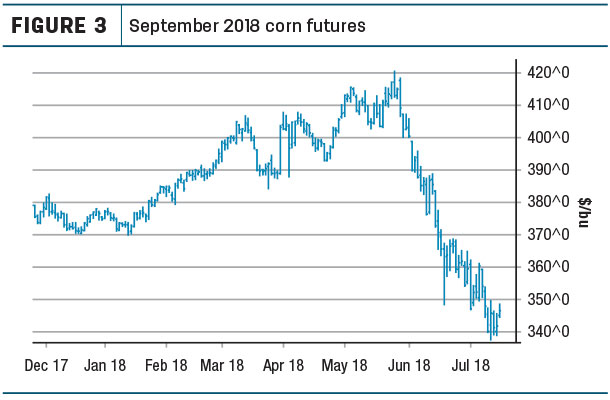

Next, let’s speak to this idea of price manipulation. To help illustrate this, let’s examine reports from the U.S. Commodity Futures Trading Commission for the positions held by managed money (funds) in the most mature agricultural market we have – corn – and compare that to price movement. (Figures 2 and 3).

You will notice an uncanny consistency between the net position (the yellow line in Figure 2 which represents all long positions minus all short positions) and the price of corn. A negative number represents a net short position.

You will also notice “Managed Money” became net long for the first time in late February. At that time, corn was trading at $3.90 to $3.95 in the September contract. They continued to buy corn.

Prices escalated to $4.20 before markets began to descend in late May. Prices plummeted. They sold aggressively as that took place. Even after prices breached $3.90, they continued to hold a long position.

In other words, while they took profits on some positions, they also experienced losses on several other positions.

So while some would look at these two charts and suggest speculators were the cause of the price move, it becomes difficult to suggest that when, along the way, their losses can sometimes be greater than their profits, as I just illustrated. Anyone who has the ability to manipulate a market would not accept a loss.

Instead, speculators bear the risk in a market others are seeking to shed.

This means dairymen can come into a market that has provided opportunity and eliminate their own risk of falling prices by handing it off to a speculator willing to accept it. This trade-off is what we refer to as hedging.

At the heart of the very existence of hedging is the ability for us, as producers, to identify that other individual who is willing to take what we do not want. And while some of these folks may not be able to tell the front of the cow from the back of the cow, they serve a vital role for today’s dairy industry.

Remember, as we analyze the risk that exists in future prices, this crowd of individuals we call speculators is essential in removing risk from our operation. ![]()

For nearly 20 years, Mike North has educated and guided dairymen and farmers in their efforts to manage commodity price risk.

DISCLAIMER: The information contained herein is the opinion of the writer or was obtained from sources cited herein. It should be noted that the impact on market prices due to seasonal or market cycles and current news events may be reflected in market prices.

Trading in futures products entails risks of loss which must be understood prior to trading and may not be appropriate for all investors.

-

Mike North

- President

- Commodity Risk Management Group

- Email Mike North