Yet with all of their differences, some things do seem to resonate with the majority of cattlemen I speak with: the desire to protect what they inherited or started, reduce estate taxes after their death, reward their children for hard work and dedication, and do all of this while maintaining control of operations.

No easy task, but it can be done. One way is by gifting shares of a business entity.

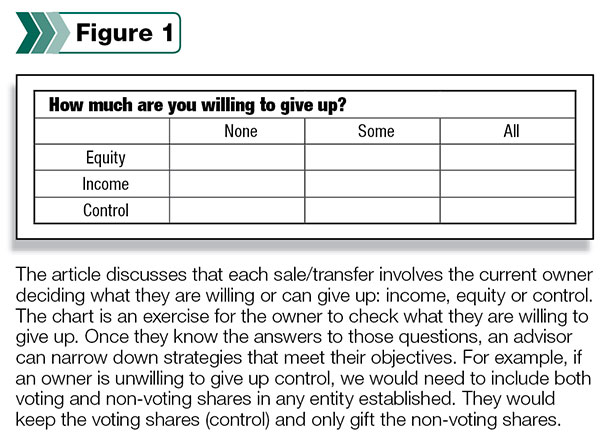

Before considering any gifting strategy, a rancher must first consider three factors present in any transition: control, income and equity.

Control

Many of the ranchers we have assisted in transition planning tell us they want to give the business to the next generation – but they aren’t ready to give up control. Many can’t afford to give up the income derived from operations, as without it they would be unable to sustain their standard of living.

Most, however, feel comfortable giving up the equity in the land and business. Once a gift has been completed, equity is forfeited.

There are many entities that can be used to both “gift” the business as well as provide a protective wrapper around the business itself. Family limited partnerships (FLPs) or limited liability corporations (LLCs) are two of the most common entities we see used for succession planning.

In an FLP, partners are either general or limited partners. General partners carry the liability and responsibility of managing the assets in the FLP. Limited partners have an economic interest but lack control of the assets. In an LLC, shares are divided between voting and non-voting shares. Voting shares maintain the control and income of the assets, while non-voting shares participate in equity ownership only.

Income

Once an entity has been established and assets transferred into the entity, an appraisal must be completed to determine the fair market value of shares. If a gift were being made dollar for dollar, the appraised value of the shares would determine how much of an individual’s lifetime exemption is being used. In 2016, each individual can gift $5.45 million without incurring gift taxes ($10.9 million per married couple).

However, because individuals will often be gifting limited interests or non-voting shares, a discounted value will apply. After the appraisal is complete, a partial-interest valuation will need to be completed to determine the amount of the discount.

Discounts are given for lack of control and lack of marketability. Look at it this way: How likely is it a third party would pay full price to own a non-controlling interest in a family business?

The discounted values are then gifted to children either in the business or non-participating. For high-net worth individuals, this allows them to gift a large asset without using up their entire gift tax exemption as well as reduce potential estate tax liability.

For example, we recently completed a plan for an individual with a net worth above the $10.9 million exemption amount. Of his total estate, his ranch accounted for $6 million of his net worth. To reduce his estate taxes by getting the land out of his estate, we transferred ownership to an LLC with voting and non-voting shares.

The discounted value was $4.2 million, taking into consideration 15 percent discount for lack of control and 15 percent for lack of marketability. By gifting the non-voting shares, he reduced his estate by the full $6 million value but used only $4.2 million of his $5.45 million exemption. He did all of this without giving up control over operations or income generated.

Equity

Another common theme when working with ranching families is: Often only one or two children are in the business. If the principal owner has other assets, he or she can gift all or a larger percentage of the ranching entity to children in the business, leaving a larger percentage of other assets to those not active.

If there are not sufficient non-ranching assets, life insurance is often used to equalize the gift.

Using the same values discussed above, the rancher would gift the discounted value of $4.2 million to the child or children active in the business. He or she would then secure an insurance policy owned by and payable to a trust with a $4.2 million death benefit. The children not active in the business would be the named beneficiaries of the trust.

The IRS has been taking a closer look at discounted gifts. To ensure they do not assess that the transaction was done solely as a tax-reduction strategy, it is important to implement business agreements that illustrate the transaction was made as a business decision.

We recommend executing both an operating agreement and buy/sell agreement. The operating agreement will outline:

- Requirements for adding new members

- Requirements for sale of assets

- Use of company equipment and resources

- Meetings of members

- Allocations and distributions

- Salaries

- Dissolution

In addition, we recommend executing a buy/sell agreement that will outline:

- Determination of value in the case of a transfer or buyout

- Disability, death or divorce buyout

- Transfer of shares during lifetime

The process above requires first and foremost an exploration of goals and objectives. We recommend working with an adviser, your attorney and your CPA to determine which entity is right for you and how gifting will affect your overall financial plan. ![]()

Jacqueline N. Davie is a registered representative and investment adviser representative with Lincoln Financial Advisors Corp., a broker/dealer (member SIPC) and registered investment adviser offering insurance through Lincoln affiliates and other companies.

Jacqueline Davie is an investment adviser with Lincoln Financial Advisers Corp. Email Jacqueline Davie.