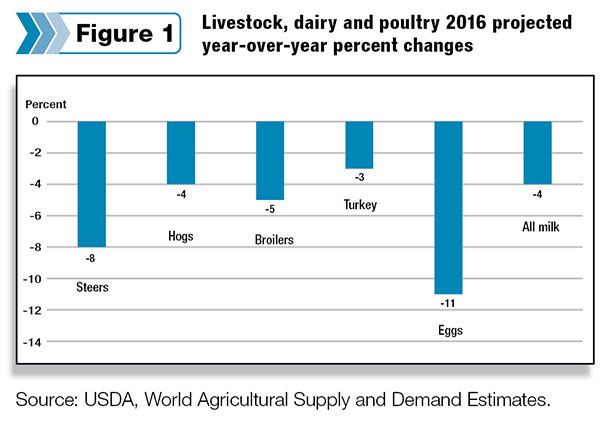

Hog prices are expected to be 4 percent lower next year, a consequence of larger hog supplies from recent industry expansion.

Poultry and egg prices are also forecast lower – broilers (-5 percent), turkeys (-3 percent) and eggs (-11 percent) – as bird numbers and exports recover from Highly Pathogenic Avian Influenza outbreaks in 2015. Stock levels of some broiler parts are expected to be larger in 2016, which should also continue to pressure broiler prices.

The 2016 all-milk price forecast is about 5 percent below prices in 2015, a result of increased milk supplies from industry productivity gains, high beginning stocks of dairy products and weak global demand for certain products.

Southern Plains expects more rain, cooler temperatures

The National Oceanic and Atmospheric Administration (NOAA) anticipates higher-than-average precipitation levels and cooler-than-average temperatures according to their U.S. Winter Outlook. With one of the strongest El Niños on record underway, favorable precipitation will likely continue to impact the Southern Plains.

As of Nov. 29, 2015, Crop Progress reported that 79 percent of winter wheat had emerged in Texas – down 3 percent compared with the 2010-2014 average.

Cooler conditions were forecast for much of cattle country, for the week ending Nov. 29, 2015, as 55 percent of selected states reported winter wheat in good or better condition – slightly lower than conditions at the same time last year (USDA Crop Progress 11/30/15).

The Dec. 8 U.S. Drought Monitor reported D0 Abnormally Dry and D1 Moderate Drought in much of Kansas, Oklahoma and Texas – a major improvement compared with last year’s severe drought conditions.

Even with the recent precipitation and beginning of El Niño, much of the West still reported D3 Extreme Drought and D4 Exceptional Drought conditions (Dec. 8 U.S. Drought Monitor).

Cow slaughter reflects low milk prices and beef cow herd expansion

Total commercial cow slaughter for January through October 2015 was 5 percent below 2014 slaughter for the same period. Dairy cow slaughter through October averaged almost 4 percent higher year-over-year and accounted for 57 percent of the total cow slaughter, largely reflecting lower milk prices, which are not expected to improve into 2016.

Beef cow slaughter through October 2015 was down 18 percent from same-period 2014, reflecting low but expanding beef cow inventories.

While the monthly more-than-800-pound category of placements in 1,000-plus-head feedlots in October was again higher year-over-year, that heaviest category accounted for only 30 percent of total placements, down from the 40-plus percent of recent months.

As the proportion of more-than-800-pound cattle placements declines over the next few months, so should the proportion of marketings of extremely heavy fed cattle, beginning next spring.

However, inexpensive corn and depressed fed cattle prices could still motivate cattle feeders to hold cattle on feed well beyond optimal finish in hope of higher prices further down the road.

Volatile prices

Fed cattle prices tumbled in October 2015. The fed-cattle market volatility is expected to continue into the winter months. The recent downward pressure on fed cattle prices can be attributed to the current high volume of very heavy fed cattle leaving feedlots.

In October 2015, the cattle placed on feed in 1,000-plus-capacity feedlots weighing more than 800 pounds were up 5 percent year-over-year; all other weight categories were down for that period (Nov. 20 Cattle on Feed).

In addition to marketings of heavy cattle, Livestock Slaughter (released on Nov. 19) reported a year-over-year increase in dairy cow slaughter, continuing the trend in monthly year-over-year increases (except in August) thus far in 2015. The resulting domestic beef supplies, coupled with very high Australian imports of beef products, may be contributing to the pressure on cattle (and beef) prices.

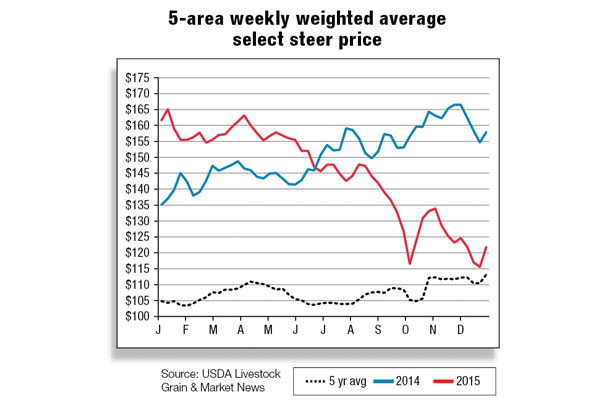

The five-area all-grade fed steer prices recently dropped below the five-year (2010-2015) average. For the week ending Dec. 6, 2015, five-area all-grade fed steers were $123.39 per hundredweight (cwt), roughly $45 lower than year-earlier fed steer prices.

The USDA projected fourth-quarter five-area direct total all grades steer prices to be $126 to $129 per cwt, down more than $38 compared with fourth-quarter 2014. The depressed prices are expected to carry into 2016; the USDA projected first-quarter 2016 fed steer prices to be $128 to $134 per cwt, down more than $30 year-over-year.

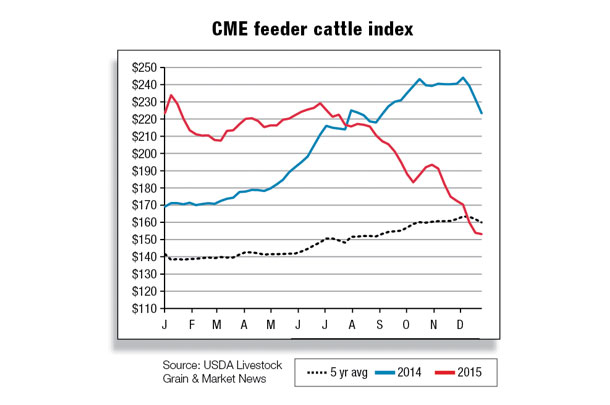

Like fed cattle prices, feeder cattle prices are also feeling downward pressure. The Oklahoma National Stockyards prices on Dec. 8, 2015, for medium No. 1 feeder steers weighing 750 to 800 pounds ranged between $153 and $160 per cwt, down around $70 compared with this time last year.

Packers cut kills, cold storage stocks surge

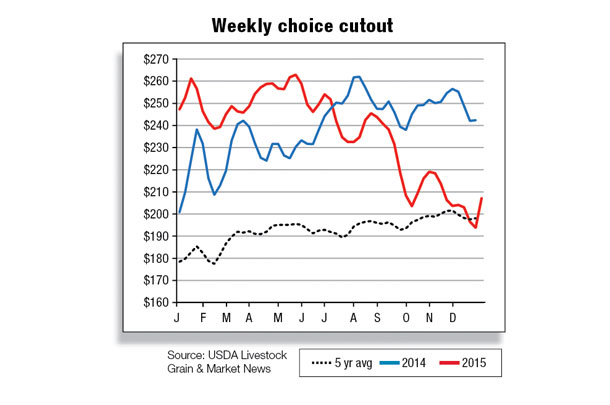

Margin pressure continues for beef processors due to the relative weakness of wholesale beef prices through much of the fourth quarter. Beef processors are limiting weekly kills in an effort to support the cutout, but how packers compensate for the year-end holiday disruptions will also play a role in reduced kill levels in the weeks ahead.

On the supply side, the strategy of reducing kills will lead to backed-up front-end supplies (once again), causing additional downward pressure on cattle prices heading into 2016.

Consumer resistance to high-priced retail beef and plentiful supplies of competitively priced competing meats (pork and poultry) have resulted in weaker-than-expected demand for beef in the latter half of 2015. In addition, large volumes of beef in cold storage could prove to be problematic for the beef complex going forward.

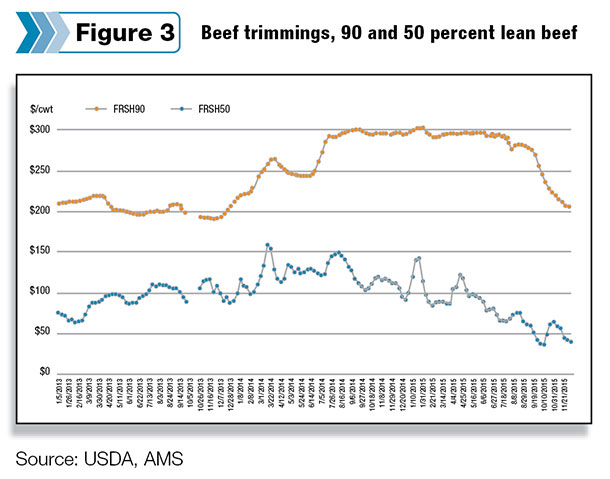

At the end of October, the USDA reported total beef in cold storage at 512 million pounds, about 34 percent higher year-over-year. Strikingly higher volumes of boneless beef have contributed to the large year-over-year increases in the total volume of beef in cold storage.

The USDA reported frozen boneless beef stocks as of Oct. 31 at a new record high of 472 million pounds. Although the USDA does not indicate whether the large stocks of boneless beef are imported or domestic, it is likely that some imported 90 percent lean beef from Australia is being included in total frozen boneless beef stocks.

Large freezer inventories can sometimes be indicative of slowing demand and packers’ inability to move product. The combination of burdensome stocks and slowing demand for processing beef is expected to continue to pressure domestic lean beef prices lower.

Beef exports lackluster, Australian beef imports decline year-over-year

A strong U.S. dollar, soft global demand for U.S. beef and lower year-over-year beef production have resulted in a very uninspiring year for U.S. beef exports. In October, beef exports to top U.S. markets were well below year-prior levels, with the exception of Mexico (up by 13 percent).

Japan, the top U.S. export destination for fed beef, continues to import more beef from Australia than from the U.S., and this adversely affected total exports. Australian cattle slaughter has slowed and is expected to fall dramatically in 2016, subsequently constraining beef exports. This should help boost demand for U.S. beef exports to Japan next year.

Overall, the U.S. is expected to produce more beef in 2016 at lower prices, increasing beef available for export, and lower beef prices should partially offset the net impact of a strong dollar and prompt renewed interest in U.S. beef on a global level.

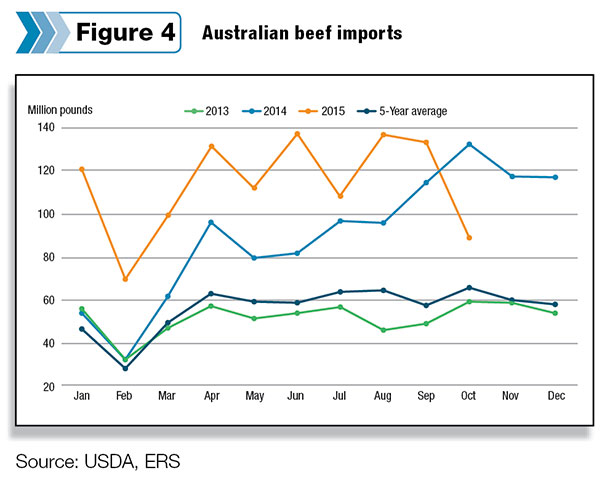

U.S. beef imports were reported lower year-over-year in October for the first time since February 2014. The USDA reported total beef imports at 237 million pounds, down about 13 percent relative to a year earlier.

The volume of beef from Australia declined dramatically (-33 percent year-over-year) for the month of October, but year-to-date totals are about 34 percent higher than a year earlier. Beef imports from other major suppliers, namely New Zealand, Canada, Mexico, Uruguay and Brazil, were all reported higher for the year in October and the January-through- October period.

According to U.S. Customs data, Australia has already filled 100 percent of its World Trade Organization tariff-rate quota of 378,214 tons. However, it is significant that Australia has filled its WTO quota for the first time in more than 10 years and thus is accessing the FTA quota for the first time. It is expected that the flow of processing beef from Australia will be significantly lower through the remainder of the year.

The Australian cattle industry is at a pivotal point. Cattle inventories are low, producers have begun to reduce slaughter rates, and herd rebuilding is expected to begin next year, assuming favorable weather.

These factors will limit the volume of Australian processing beef available for export in 2016. In addition, reduced demand for processing beef from the U.S. will also adversely affect Australian exports next year. ![]()

Kenneth Mathews is coordinating analyst for the USDA Economic Research Service. Analyst Mildred M. Haley assisted with this report.