The 5 C’s Explained

When considering a land loan, lenders will look at a farm or ranch’s:

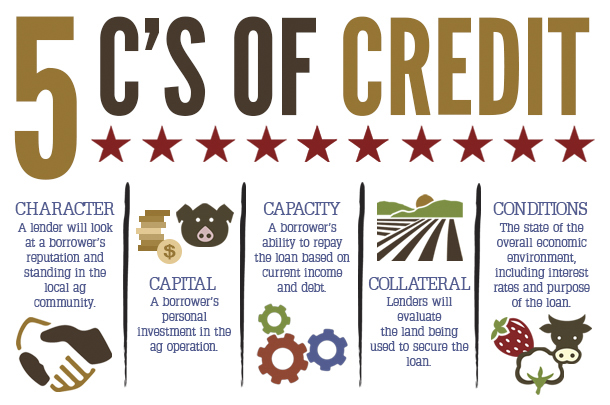

When considering a land loan, lenders will look at a farm or ranch’s:

• Character: the borrower’s reputation and standing in the local ag community.

• Capital: the borrower’s personal investment in the ag operation.

• Capacity: the borrower’s ability to repay the loan based on current income and debt.

• Collateral: property or large assets used to secure the loan.

• Conditions: factors such as the interest rate and purpose of the loan.

These five factors help the land lenders determine a borrower’s risk for defaulting on a land loan. The better or stronger an agribusiness’ 5 C’s, the lower their risk of default, and the more likely they will be approved for a loan.

Q&A with AgAmerica Lending

Q: When considering a loan application, how do the 5 C’s apply in terms of what AgAmerica is looking for in a borrower?

A: Our predominant focus is on collateral, specifically agricultural land (50 acres and up) – farms, ranches, recreational properties, timberland, and even future development land are all considered. Hand in hand with collateral is capital; our ideal borrowers do need to have equity in their land. Character is probably the second most important factor to us. We like to really get to know our borrowers and who they are; how they run their operations during good times and bad. How do they conduct their business affairs in the ups and downs? We do also consider capacity; however, we have a variety of lending products, so if a borrower is a little weaker in this category, AgAmerica typically can still work with the borrower to accomplish their goals.

Q: Which of the 5 C’s does AgAmerica Lending deem the most important?

A: Hands down, collateral. AgAmerica is unique in that we have a variety of lending platforms and products to accommodate borrowers at almost any point along the interest rate spectrum. As long as the collateral is solid, we can generally provide a lending product to help accomplish our borrower’s goals and dreams.

Q: Which of the 5 C’s is open to interpretation by AgAmerica lending teams?

A: Conditions. Once we are comfortable with the collateral, AgAmerica will take a global look at each loan, taking all of the C’s into consideration. Where other lenders look immediately to credit and capacity (often turning borrowers away), AgAmerica specializes in thinking outside the box. We can be creative in structuring tailored lending products for each borrower.

Q: How can agribusinesses improve the 5 C’s of their operations to be more attractive to lenders?

A: Be proactive! Many times borrowers get too far in debt for us to be able to help in any meaningful way. By contacting us sooner, we may be able to help cut financing costs and/or significantly lower payments and ensure the long-term success of the operation.

Q: How does Character factor in?

A: Another important aspect is to maintain good character and good standing in your community. We will look into the background and history of each borrower. If we see someone who has a history of not paying their creditors (regardless of circumstances), we are less inclined to move forward. However, we are very understanding of the ups and downs of farming and when borrowers have fallen on hard times. Good character will come through no matter the situation.

At AgAmerica Lending, we’re committed to finding unique solutions for our clients. As the country’s premier land loan specialists, we help agribusinesses big and small grow and prosper with our low interest rates, long amortizations, and an outstanding 10-year line of credit.