These dramatic effects have ranged from massive sell-offs in the futures market, record packer profit margins, coupled with increases in Saturday harvest numbers, and volatile feeder and fed cattle prices. But to date, most of the cattle market commentary has focused on packing plant and feedlot responses. Little has focused on how cow-calf producers have responded due to this event and resulting feeder futures market volatility. Responses between these groups will be fundamentally different since packers and feedlots operate off margins, whereas cow-calf operations rely on market price levels where profitability is largely driven by controlling costs.

To illustrate the market uncertainty cow-calf producers were making decisions in this past year, let’s take a representative Northern Plains cow-calf producer who calves in March or April and then sells weaned calves in October. At calving, October 2019 feeder cattle futures prices were $157 per hundredweight (cwt). Poor planting conditions caused a run-up on corn prices, dropping demand for feeder cattle prices to $147 per cwt. Markets bounced between $145 and $132 per cwt in June, July and August before the Holcomb fire dropped prices to $127 per cwt. Prices did recover, and the October 2019 futures contract finished near $145 per cwt. Depending upon how risk-averse producers were likely determined price risk management used and, ultimately, gross revenue received for sold calves.

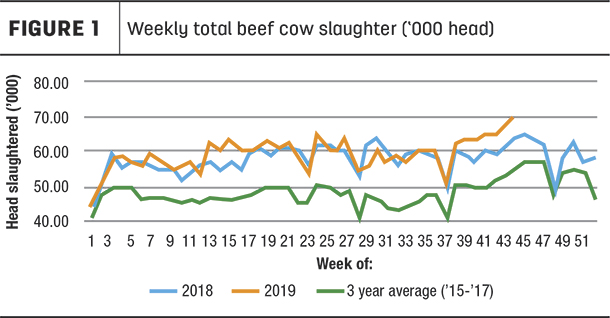

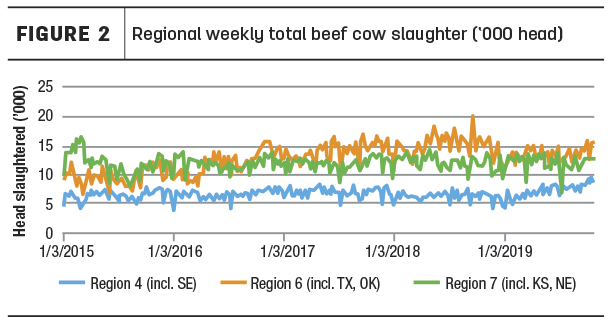

Given this market volatility, cow-calf producers could respond by either selling cows and exiting the market, or retaining beef cows for breeding. Their response to these events ultimately determines the availability of feeder cattle in the coming years. The Cattle Inventory report in January 2020 will officially detail the number of bred beef cows and heifers held for breeding herd replacement this fall. Before this release, the weekly USDA Agricultural Marketing Service (AMS) Cow Slaughter Under Federal Inspection report can provide the direction of cow-calf producer response. This report suggests there is a large beef cow sell-off occurring since the week of Sept. 14 (see Figure 1), with significant regional differences (see Figure 2). There is a clear uptick between beef cow slaughter in 2018 and 2019 beginning in week 37, and it is well above the three-year average. Approximately 28% of the increase in beef cow slaughter came from regions which include Nebraska, Texas and Kansas, 32% from Idaho, Oregon and Washington, and 16% from the Southeast.

The Holcomb fire occurred on Aug. 9, 2019 (the 32nd week of the year). The October 2019 feeder futures contract initially dropped from $140 to $130 per cwt and settled at $135 over the next few weeks before sliding back down to $130 the week of Sept. 14 (the 37th week of the year). Beef cow slaughter numbers closely tracked 2018 numbers for most of 2019, even during the fire incident (week 32 to week 37). Since the week of Sept. 14, 2019, beef cow slaughter numbers are on an upward trend and do not show any signs of slowing down. The Holcomb fire has surely impacted some producers’ decisions to remain in the business.

However, this rise in beef cow slaughter was partially driven by factors other than the Holcomb fire. Several reasons include: Imported 90% lean beef prices are skyrocketing largely driven by Chinese demand but has pulled the domestic market along with it; wet spring and summer seasons have damaged hay, tightening available hay supplies going into winter; and while futures markets have rebounded from the fire, local cash markets have been slower to respond. These factors combined, not related to the Holcomb fire, has some cow-calf producers exiting the industry. In the short term, this reduction in beef cows affects the number of calves born next year and feeder cattle available to enter feedlots. In the long term, it could ultimately signal the industry is beginning to enter a contractionary phase of the cattle cycle. Monitoring these trends the remainder of the year will reveal producer preferences. ![]()

Reference omitted but are available upon request. Click here to email an editor.

Dr. Elliott Dennis is an assistant professor in the livestock marketing economist department of agricultural economics at the University of Nebraska – Lincoln.

—Excerpts from the Livestock Marketing Information Center In The Cattle Markets newsletter, Nov. 11, 2019