Last week, Elliott Dennis discussed the relationship between corn price and feeder cattle placement weights and the likelihood that the industry will continue to place lighter weight cattle while corn prices remain high.

When cattle are placed on feed at lighter weights, they tend to finish at lighter weights, which typically reduces the percentage of cattle grading Choice. As the industry adjusts to high corn prices, what will happen to the Choice-Select spread?

Over a 12-month time period, the Choice-Select spread is typically narrowest in the January to March time frame as the demand for Choice-graded middle meats is at its lowest, and the supply of Choice-graded cattle is typically at its highest. In contrast, as we go into summer, the demand for Choice-graded middle meats is higher as retailers fill shelves in anticipation of the grilling season, but the supply of Choice-graded cattle is lower as we see more calf-fed cattle being harvested. The percentage of lightweight animals (less than 700 pounds) placed on feed is highest in November and this percentage typically decreases until May.

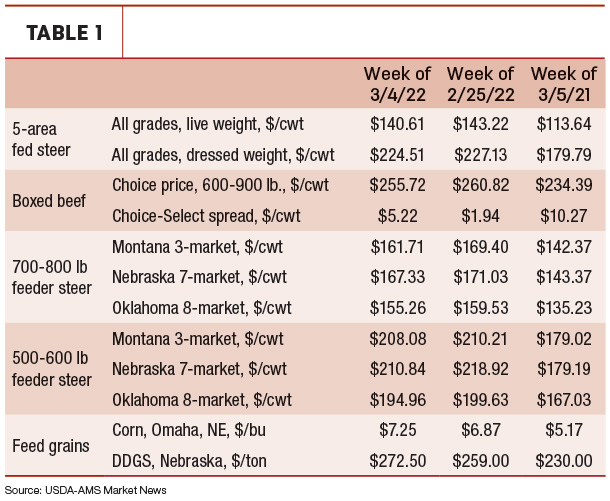

The last few weeks have seen the Choice-Select spread narrow to $3.97 compared to a 2019-2021 average of $5.78 for the same week. Considering we began 2022 with a spread that was almost $4.50 wider than the 2019-2021 average, the narrow spread illustrates the backup in cattle processing in January. Currently, the average weekly year-to-date dressed steer weight is up 9 pounds over 2021 and 24.8 pounds over the 2019-21 average for this time of year. The increase in dressed weights is partially due to the backed-up cattle supply due to COVID-19-related labor issues in the packing sector. As cattle finish at higher weights, the percentage of Choice-graded cattle tends to increase. Year to date, the percentage of cattle grading Choice is up 1.25% over the 2019-21 average.

Seasonally, the Choice-Select spread will widen until late June/early July due to the supply/demand considerations for Choice and for Select beef. However, given the higher percentage of lightweight cattle placed on feed since November as compared to the 2019-21 average lightweight percentage placed on feed, the Choice-Select spread will likely widen more than average. How wide the spread becomes is dependent on corn prices when cattle are placed, the percentage of cattle grading Choice, total amount of beef production, as well as beef demand. If we hold all those factors affecting Choice-Select spread at a constant level and allow only the percentage of beef grading Choice to change, the impact of a 1% change in cattle grading Choice can have almost a 9% change in the spread. This means that since the average 2016-20 spread was as wide as $22.45 in June, a decrease of 1% in Choice-graded beef could widen that spread by another $2, providing some incentives to feed cattle longer and to heavier weights.

The markets

All cattle and calves in the U.S. and Canada combined totaled 103 million head on Jan. 1, 2022, down 2% from the 105 million head on Jan. 1, 2021. All cows and heifers that have calved inventory at 44 million head, down 2% from a year ago.

For the week, May corn prices were up 98.5 cents, while December corn prices were up 49.75 cents. Cattle markets continued the downward slide, with April live cattle prices down $6.15 last week and June live cattle down $5.78. Cash prices were down around $2 depending on the market. Feeder cattle prices also show large declines, with March feeder cattle prices down $6.90 and April feeder cattle prices down $7.50 last week. Declines in prices are due to the Russia-Ukraine conflict and the impact on feed prices. Average Texas cash feeder cattle prices for cattle weighing less than 600 pounds were up $3.82 week over week, while those over 600 pounds were down $6.55 week over week.

—This originally appeared in the Livestock Marketing Information Center’s March 7, 2022, In the Cattle Markets newsletter.