USDA’s June World Ag Supply & Demand Estimates (WASDE) report raised 2016 and 2017 U.S. milk production and marketing estimates, but also saw reason to brighten the 2016 price outlook.

• 2016 milk production and marketings were raised about 200 million pounds from last month’s forecast, to 212.6 billion pounds and 211.6 billion pounds, respectively. If realized, both would be up about 1.9 percent from 2015.

• 2017 milk production and marketings were raised about 100 million pounds from last month’s forecast, to 215.3 billion pounds and 214.3 billion pounds, respectively. If realized, both would be up about 1.3 percent from 2016’s estimates.

The increased milk production forecasts were based on the growth of cow numbers.

Read: April milk production up as milk cow numbers hit 8-year high.

Fat- and skim solids-basis export forecasts for 2016 and 2017 were lowered, as international supplies of dairy products remain abundant and U.S. prices remain high relative to those of competitors. Butter and cheese stocks were forecast to remain relatively high. Fat-basis imports were reduced for both 2016 and 2017 on expectations of slower imports of butterfat products, and to a lesser extent, cheese.

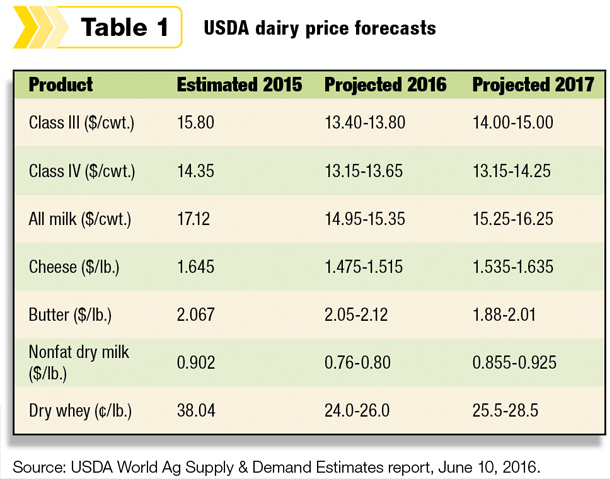

Cheese and butter prices for 2016 were forecast higher, despite relatively large stocks. The nonfat dry milk (NDM) price was raised based on recent price strength. The whey price forecast was unchanged at the midpoint.

Cheese prices are forecast lower for 2017 as relatively high stocks pressure the market, but prices of butter, NDM and whey are unchanged from last month.

As a result, Class III and Class IV price forecasts were raised for 2016 (Table 1). For 2017, the Class III price is lowered on lower cheese prices, but the Class IV price is unchanged.

Compared to last month, the 2016 all-milk price was forecast $.25 to $.35 higher at $14.95 to $15.35 per hundredweight, but unchanged at $15.25 to $16.25 per hundredweight for 2017.

Beef outlook

Impacting cull cow prices, the forecast for 2016 and 2017 total red meat production was lowered from last month, based largely on higher feed prices dampening the rate of production growth. Beef production for 2016 was reduced mostly on lower carcass weights, but the pace of second-quarter slaughter was slightly slower than previously expected.

Production in 2017 was reduced on slightly lower carcass weights, as higher feed prices are expected to encourage cattle feeders to minimize the amount of time cattle are on feed.

Annual average steer prices for 2016 were raised from last month to $125 to $129 per hundredweight, with 2017 prices forecast in a range of $118 to $128 per hundredweight.

Feed situation

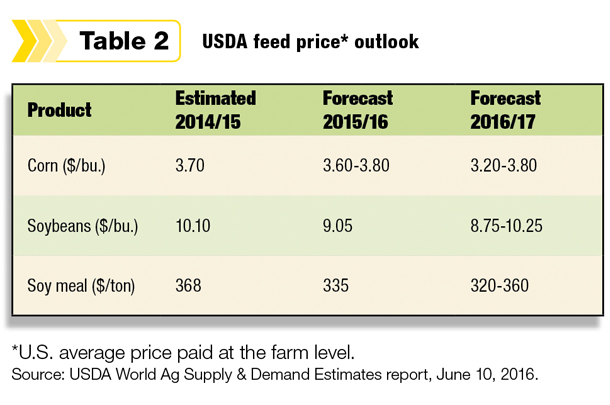

On the feed side of the equation, the 2016-2017 outlook for U.S. feed grain supplies was lowered. Projected corn production for 2016 was unchanged at a record 14.430 billion bushels. Corn ending stocks for 2015-2016 were reduced 95 million bushels due to heavier exports. Reduced corn production in Brazil and harvest delays in Argentina have improved the relative competitiveness of U.S. corn in recent weeks.

The season-average farm price for corn was raised for both 2015-2016 and 2016-2017 (Table 2). The 2015-2016 price was forecast up $.10 per bushel at the midpoint, within a range of $3.60 to $3.80 per bushel. The 2016-2017 price was projected $.15 per bushel higher at the midpoint, within a range of $3.20 to $3.80 per bushel. Price outlooks for other feed grains were also raised.

This month’s U.S. soybean supply and use projections for 2016-2017 include lower beginning stocks, higher exports and lower ending stocks. Soybean meal exports were raised.

The 2016-2017 season-average price for soybeans was forecast at $8.75 to $10.25 per bushel, up $.40 at the midpoint. Soybean meal prices were forecast at $320 to $360 per ton, up $20 at the midpoint.

See the full World Ag Supply & Demand Estimates report (PDF, 257KB). PD

-

Dave Natzke

- Editor

- Progressive Dairyman

- Email Dave Natzke